Cloud-computing and enterprise software stocks have been on fire. They were the leaders going into the fourth-quarter correction and they were one of the first groups to bottom. Workday (NASDAQ:WDAY), Salesforce (NYSE:CRM) and others bottomed in November and have been climbing ever since. However, Workday stock has been under pressure since reporting earnings, causing investors to ask if now’s the time to buy.

To determine that, we need to comb through the company’s earnings results.

Workday Earnings

Last week, Workday delivered a top- and bottom-line earnings beat on its fourth-quarter results.

Non-GAAP earnings of 41 cents per share beat consensus expectations by 9 cents. On a GAAP basis, WDAY turned in a 47 cent per share loss, although that was 8 cents better than expected. On the revenue front, sales of $788.6 million beat analysts’ expectations by almost $12 million and grew 35.4% year-over-year (YoY).

Both subscription and services revenue came in ahead of expectations, as did billings and operating margins. All while management raised its subscription revenue for this year. The company now expects $3.03 billion to $3.045 billion in subscription sales vs. a prior outlook of $2.375 billion to $2.377 billion.

At this point, you’re probably wondering why Workday stock isn’t rally

after a report like this. Further, why is the stock action down 10% after the fact?

We need to keep a few things in mind. First, the stock clearly ran too much ahead of the print. Up more than 66% from its November lows, and anything short of a mega-blowout quarter was a sell-the-news event. Second, WDAY stock is already quite expensive and even with better-than-expected results, it needs some time to let the fundamentals catch up to its price.

Valuing Workday Stock

I love Workday’s products and it’s clear that its customers do too. That’s said, the valuation is rich — and that’s putting it mildly. Investors who are going to get involved in cloud and enterprise software stocks need to swallow their traditional valuation metrics. These names typically trade at insane multiples, but it’s hard to deny their long-term performance. That’s why it’s best to buy on big dips — like we saw in Q4 — rather than at or near all-time highs.

With Workday, we can see why. While current expectations call for great growth — 26% and 23% revenue growth this year and next, and 21% and 33% earnings growth this year and next — 110 times this year’s non-GAAP earnings is very high. Operating cash flow increased about 30% in the last fiscal year and management expects similar growth this year. Free cash flow also continues to increase, eclipsing $600 million over the trailing 12 months.

When we dig a little further past the headline results, we see that the booking growth outlook for this year lags management’s revenue growth outlook. That suggests slowing organic growth. Currently trading at 11 times this year’s sales, WDAY stock isn’t cheap. But given its growth and solid business, I think that’s why we’re only ~10% off the highs. All things considered, Workday’s pullback seems justified and doesn’t mean the bull run is over.

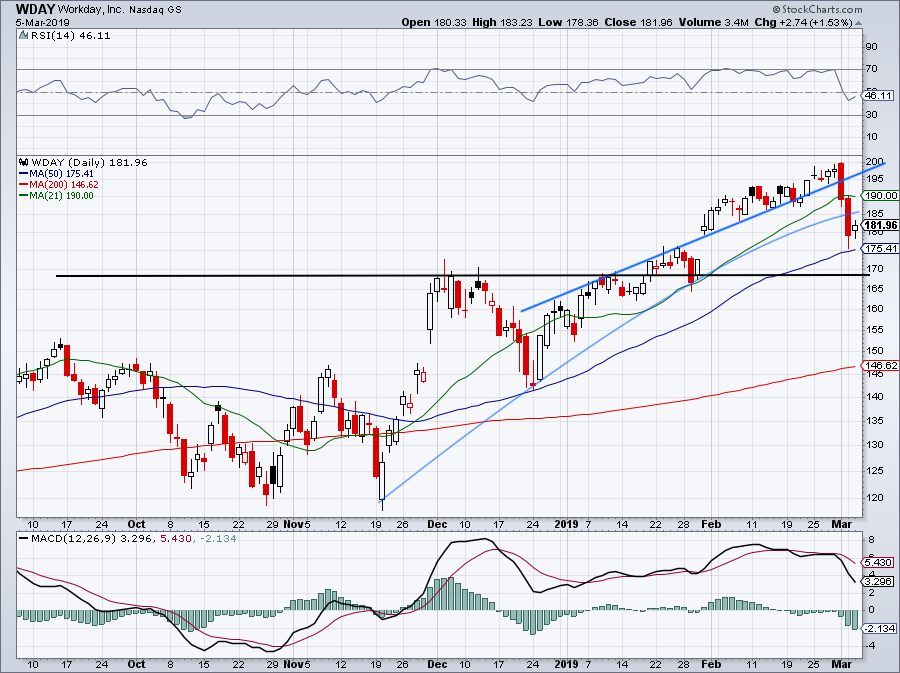

Trading WDAY Stock

Click to Enlarge

In short, I think we have a valuation issue with Workday stock. These forms of consolidation can either happen through time or through price (or both). So far, WDAY stock is correcting through price, down 10% in just a few days. We’ll see if further consolidation happens through time or in the form of more declines.

If it’s the latter, here are the levels to keep in mind. Knifing through the 21-day moving average, WDAY stock is currently using the 50-day moving average as support. I like the work it is putting in above the 50-day, consolidating that decline. But I wouldn’t hate a move down to $170-ish.

Why? Because this was an important level on the way up and I would like to see it now act as resistance. Further, it would flush out the stop-loss orders that are no doubt piling up near the 50-day as we speak. Finally, the 38.2% Fibonacci retracement for the 52-week range comes into play just over $169, while the 61.8% retracement for the year-to-date range is up near $170.48.

At this point, let’s see if the 50-day acts as support. Above and we’ll need to see how Workday stock does with the 21-day. Below and $170 becomes key.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.