If last quarter’s numbers from Delta Air Lines (NYSE:DAL) and United Airlines Holdings (NASDAQ:UAL) are an early indication, then then Thursday’s Q2 report from Southwest Airlines (NYSE:LUV) should prove bullish for an otherwise lethargic LUV stock. Shares of the rival carrier have underperformed DAL and UAL stock in a big way since early last year.

On the other hand, even with the decidedly disparate performance, the current LUV stock price near $53 leaves shares oddly overvalued compared to most of its peers.

The upcoming event may well put Southwest stock on course for a higher altitude, but the airline will have to bring a big-time ‘wow’ factor to the table to shake the stock out of its funk.

Southwest Earnings Outlook

Delta’s second-quarter top and bottom lines were both better than expected. Ditto for United Airlines. Indeed, most of the airlines that have posted second-quarter numbers have managed to impress investors.

The backdrop serves as a double-edged sword for Southwest, which is slated to share its Q2 results on Thursday morning, July 25.

The industry’s wave of success suggests Southwest also top expectations, but should it fall short, the shortfall will look relatively worse considering other airlines didn’t bump into a headwind.

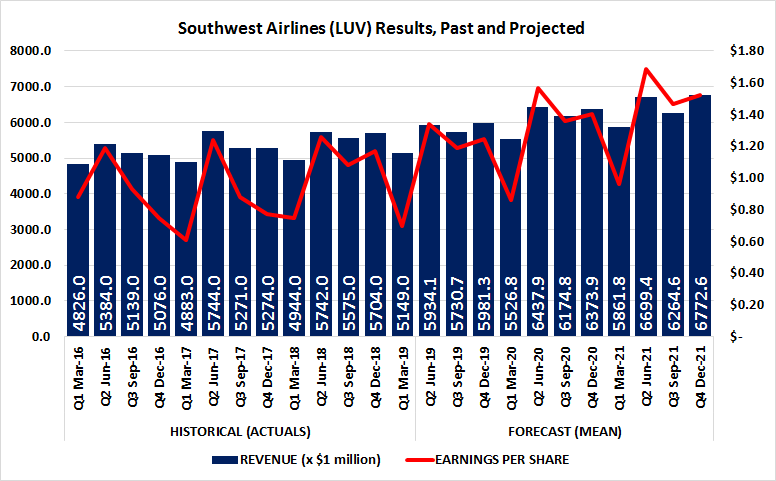

To that end, the bar is set more or less on par with how those other airlines fared. Analysts are calling for earnings of $1.34 per share for the quarter ending in June, versus the $1.26 per share of LUV stock reported in the same quarter a year earlier. Analysts are looking for a top line of $5.93 billion, on average, up 3.3% from the year-earlier figure of $5.74 billion.

Beyond the raw numbers, investors may largely end up making buy/sell decisions based on a trio of more obscure criteria.

Things to Watch in LUV Stock’s Earnings

1.Impact of Boeing 737 Debacle

The 737 MAX from commercial jet maker Boeing (NYSE:BA) has been grounded in the United States, and in other select areas all over the world. It’s arguably been the biggest disruption any airline has been forced to tangle with this year.

Southwest has adapted, though not elegantly. The company has stopped hiring and promoting pilots, and has also been forced to cancel flights that can’t be cost-effectively handled by other aircraft. With the 34 of the 737 MAX 8 jets in its fleet now grounded until early November, Southwest — the biggest single user of the jet — must continue to handle the logistical nightmare.

2.PRASM

PRASM, short for passenger revenue per available seat mile, will paint a more accurate picture of Southwest’s quarter without penalizing it for its dependency on the 737 MAX 8.

A quarter earlier, Southwest’s PRASM grew 2% to 12.52 cents, while total revenue per available seat mile improved 2.7% to $13.59 cents. During the second quarter of this year, United Airline’s PRASM grew 2.5%. Delta’s figure improved along those same lines.

3.Operating expenses

At the other end of the spectrum, LUV stock holders will want to measure the airline’s costs incurred in ferrying the passengers sitting in its planes’ seats.

That’s best measured with a metric called CASM, or cost per available seat-mile. Southwest’s CASM during the first quarter of the year was up 5.1%, and as such wasn’t fully offset by rising per-unit revenue.

This is a front where Southwest is particularly vulnerable. Though now proven problematic, the 737 MAX was a very fuel efficient airplane. Southwest was counting on relatively lower fuel costs in 2019 and beyond, but the grounding of its 737 MAX jets wipes away that cost advantage.

To that end, Delta — which didn’t fly the 737 MAX plane that’s grounded in many major markets — reported an unadjusted GAAP decline of 1.5% in CASM, though on an adjusted basis, Delta’s second quarter CASM was still up 1.4%. United’s CASM for Q2 was practically flat.

Looking Ahead for LUV Stock

For the record, Delta raised its full-year profit outlook when it reported its second quarter numbers earlier in July. United Airlines upped the lower end of its 2019 profit forecast, from a range of between $10.00 and $12.00 to a range of between $10.50 and $12.00. It’s likely Southwest will share a similarly-improved outlook, even if it doesn’t offer specifics.

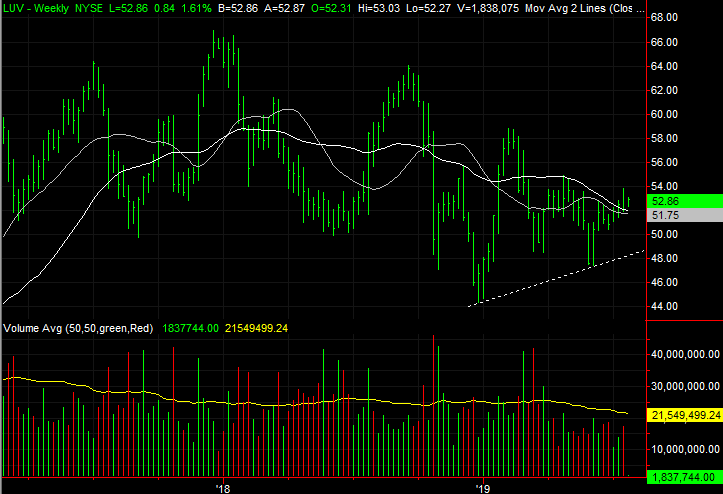

Even so though, the airline’s results are leaving investors struggling to rectify the stock’s valuation with a chart that’s seemingly testing the waters of a recovery effort.

Click to Enlarge

LUV stock has been trending lower, albeit erratically, since peaking in early 2018. The weakness has been problematic despite continued top line growth and at least a steady, reliable bottom line that’s only been subject to sweeping changes in oil prices.

The net-bearish outcome, therefore, is largely attributed to an above-industry-average trailing P/E of 12.5. Analysts, however, are modeling a massive improvement in next year’s profits that other airlines aren’t apt to keep pace with.

Click to Enlarge

This shift may be a key reason the late-May/early-June low from Southwest stock was the first major higher low shares have logged since 2016.

The turnaround effort is still wobbly to be sure. LUV stock has only just crossed back above its 200-day moving average line, but even then it’s far from securely in a new uptrend.

If the company can convince investors that it’s truly positioned to do something it’s struggled to do over the course of the past year, though, LUV stock may actually offer more potential upside than most other major airline stocks do at their current prices.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.