A strong five-week rally by gold stocks and related ETFs like the SPDR Gold Trust (NYSEARCA:GLD) hit a wall two weeks ago, but it was completely reversed this past week.

As it turns out, the Federal Reserve is more or less happy with where interest rates are right now, and the strong June jobs report has quashed inflation worries for now, buying the FOMC some more time.

GLD has fallen 3% from its late-June peak, while leading gold stocks like Barrick Gold (NYSE:GOLD) and Newmont Goldcorp (NYSE:NEM) have suffered similar setbacks. In short, the buying that sent gold prices up 30% beginning in early May appears to have been mistimed.

Before jumping to conclusions that this is just another false start for gold stocks though — extending a multi-year streak of false starts — it would be wise to take a step back and digest another stark reality about the use of gold as a hedge against any sort of financial difficulties. The reality is that, for better or worse, gold never actually behaves as it’s “supposed to.”

Meanwhile, charts tend to lead views on gold rather than the other way around.

Reality Check

Gold is allegedly a hedge against inflation. It’s also a safe haven against currency turbulence. It’s also a preferred holding during economic lulls. And gold prices as well as gold stocks are often viewed as a beneficiary of falling interest rates.

Finally, gold prices are expected to rise when the U.S. dollar loses value.

All of these moving parts result in one overarching reality: Speculating on gold is mostly a coin toss.

That’s not a truth a wide swath of gold pundits agree with, though that doesn’t change the facts of the matter. Specifically, the presumed relationship between interest rates and gold prices doesn’t hold up. Neither does the relationship between gold and inflation. As a result, since interest rates and inflation also impact the actual value of currency, the correlation between gold and the U.S. dollar is wobbly at best.

The idea of using gold as a currency hedge may hold some water, though the volatility of exchange rates can be difficult if not impossible to successfully handicap.

None of this means that the basic underpinnings of all the aforementioned relationships don’t hold any water. They do. I’m simply pointing out that many of the underpinnings are also impacted in unpredictable ways — often in opposing ways — by one or more of the other drivers of gold prices.

But gold prices are still impacted primarily by speculation.

Speculation controlled gold prices between 2010 and 2012, when inflation remained tame and interest rates were steady. The value of the dollar was relatively weak at the time, too, but it was also holding steady, even as gold and gold stocks soared on the presumption that the greenback would lose more value.

It didn’t.

The failure of those factors to ever fully justify the large jump in gold prices ultimately set the stage for a big price pullback by GLD and gold stocks in 2013 and 2014. The U.S. dollar was on the mend at that point, but not to the degree suggested by the gold selloff.

The Outlook of GLD and Gold Stocks

Don’t misread my message. While the recent gold rally was thwarted by new perceptions that a rate cut isn’t a foregone conclusion and the increasingly clear message that inflation isn’t an issue just yet, the rebound efforts could be rekindled.

The key is the shape of the chart.

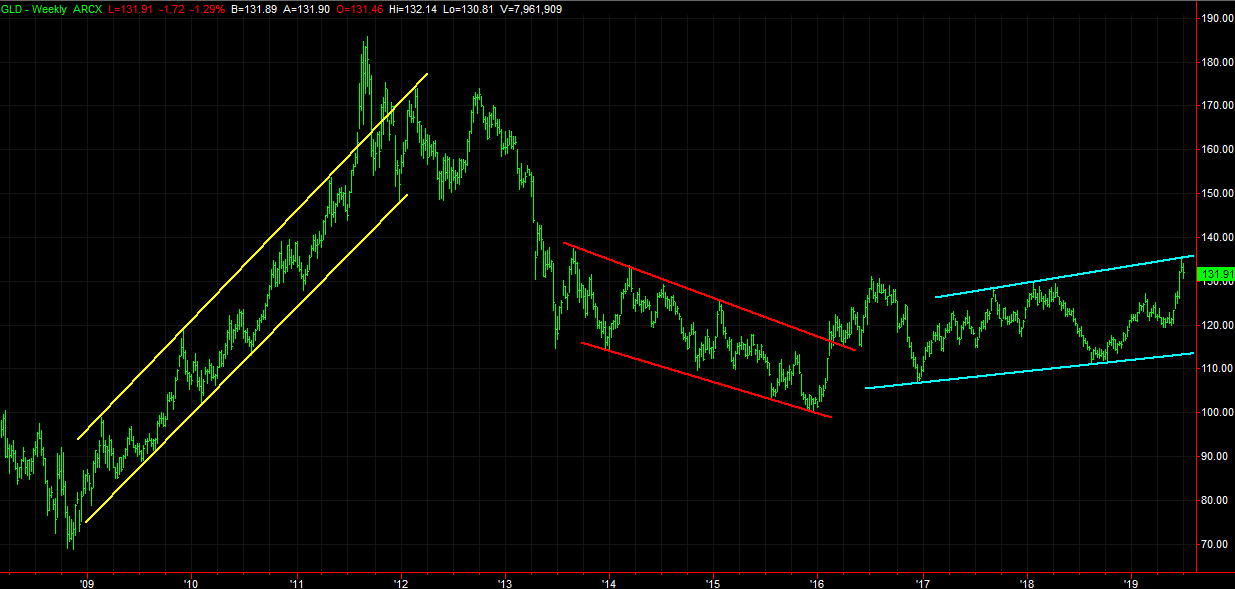

Based on the chart of GLD, one can see that the peak from two weeks back may have been destiny anyway. GLD’s recent high near $135.50 more or less lines up with peaks from mid-2017 and early 2018.

Click to Enlarge

Also note that since the late-2015 low, gold prices have managed to log a string of higher lows. Big swings between the technical floor and ceiling have been the norm, though.

And those big swings haven’t necessarily been in conjunction with the appropriate changes in interest rates, the dollar’s value, or inflation. Assumption and speculation have continued to be responsible for most of the movement of the prices of gold stocks and of GLD.

That’s not necessarily a bad thing, though. Right or wrong, speculators tend to move in rather predictable patterns that become visibly evident on a chart.

In this case, a slide back to the floor near the $114 area wouldn’t be out of character for GLD, while a break above the recently-conformed ceiling near $136 would likely spark a melt up. Even if such a bullish thrust is in the cards though, it’s unlikely to take shape without a small setback first, which will give the bulls the opportunity for another running start to punch through that resistance.

Little to none of that action, of course, will actually have anything to do with the things traders like to pretend control GLD and gold stocks.

In other words, if your gut is at odds with the rhetoric, don’t be afraid to trust your gut.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about him at his website jamesbrumley.com, or follow him on Twitter, at @jbrumley.