PepsiCo (NASDAQ:PEP) shareholders clearly expect to hear more good news when the beverage and snack giant reports its fiscal second-quarter numbers on Tuesday morning. Pepsi stock is up 9% since its most recent quarterly report. It has also rallied nearly 18% since the Q4 2018 Pepsico earnings. By consumer-staples standards, that’s a monumental run up.

It’s also not a terrible bet. Although the big move does present some valuation-based challenges for Pepsi stock, it’s been years since Pepsico earnings have missed. Indeed, it’s only failed to beat quarterly bottom-line estimates once in the past three years alone.

Still, the sheer scope of the multi-month gain sets the stage for potential profit-taking. Should the Pepsico earnings report present anything less than ideal, a beat may prove irrelevant.

Pepsico Earnings Preview

For the most recent look, analysts collectively expect the company to report earnings of $1.50 per share of Pepsi stock. Additionally, forecasts call for sales of $16.42 billion. That bottom line would be up versus the operating profit of $1.49 per share that Pepsico booked in the comparable quarter from a year earlier. Furthermore, revenue at that level would mark a 2.1% improvement on the year-ago top line of $16.1 billion.

Adverse currency-exchange rates have been and continue to weigh results down. However, please note that rivals like Coca-Cola (NYSE:KO) and Procter & Gamble (NYSE:PG) have lamented the same headwind. During the first fiscal quarter of 2019, disadvantageous foreign exchange rates reduced Pepsico’s per-share profit by 2%.

3 Things to Watch

While a multi-faceted company, investors will only be able to respond to the most noteworthy changes in the company’s business. Three items presently matter more than any other. As such, they need to be weighed carefully during and following the Q2 Pepsico earnings report.

1.Organic Sales

Organic revenue is a figure that strips away the misleading impact of changes in currency-exchange rates. It also removes changes associated with business acquisitions or divestments. In other words, it is a more accurate picture of a corporation’s true health and Pepsico stock specifically.

For Q1, Pepsico saw organic sales growth of 5.2%. Assuming the company maintains this stride, it’s a repeatable target.

2.Full-Year Guidance

With its Q1 Pepsico earnings report, PEP modeled full-year organic revenue growth of 4%. And though it also cautioned per-share profits could decline by 1% in 2019, that would be entirely due to investment being made in its growth. Perhaps more importantly, Pepsico guided for $9 billion in operating cash flow and $5 billion in free cash flow. Management is planning on giving $8 billion of that back in the form of dividends and stock repurchases.

Changes to that initial outlook have the potential to move Pepsi stock, for better or worse.

3.Revenue Mix Vs. Profit Mix

North America’s beverage arm is the company’s biggest by revenue, producing 32.2% of Q2 2018’s top line. It’s not Pepsico’s breadwinner in terms of income though. That honor belongs to North America’s Frito-Lay snack-food unit. This arm accounted for 23.8% of the year-ago revenue but contributed 39.6% of the company’s total operating earnings.

While it’s unlikely to change much, you should look out for any variances of each unit’s sales and earnings contributions. Even small fluctuations could signal trouble and potential disruption of Pepsi’s low-margin business.

Looking Ahead for Pepsi Stock

Regardless, investors mostly have to embrace that judging Pepsico stock right now isn’t a simple exercise.

Just a few days ago, analysts with Bank of America Merrill Lynch noted that FY2019 is an “investment year.” Specifically, management hopes to bolster growth through capability enhancement, manufacturing, and go-to market capacity additions. Further, advertising and marketing investments should increase consumer awareness.

It’s a work in progress and will be difficult to ferret out any specific impacts just yet. However, the market may respond to a qualitative feel on how this spending is setting up future growth.

On the other hand, that qualitative feel for Pepsico stock may not matter at all right now.

While it would be unlikely Pepsico fails to continue moving fiscally forward, that might not be enough for Pepsi stock.

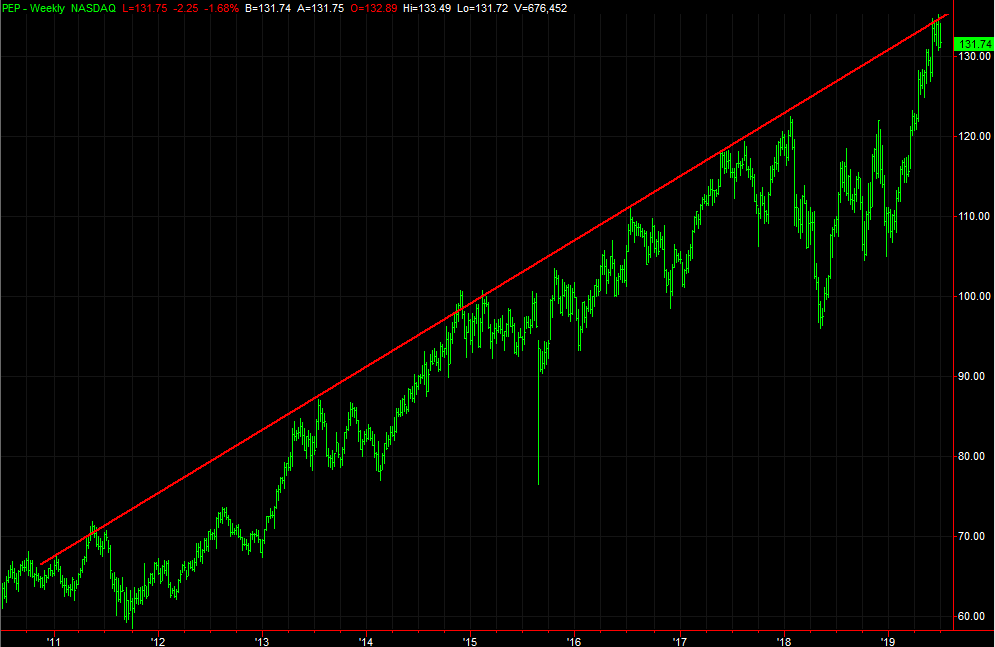

Click to Enlarge

One has to zoom out to a multi-year chart of Pepsi stock to fully appreciate it. However, the rebound since May of last year has been more than dramatic. In fact, the 37% jump over this timeframe is unprecedented.

It’s also carried Pepsico stock back to a familiar resistance line that tags all the major price peaks going back to 2011.

Now valued at a trailing price-earnings ratio near 23 and a forward-looking of 24, we’ve got to get real: there’s little plausible room for more upside even if the beverage and snack company does everything it’s expected to do. Prior to 2015, a trailing PE anywhere but the mid-teens was unusual. Therefore, you should approach Pepsico stock with caution.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about him at his website jamesbrumley.com, or follow him on Twitter, at @jbrumley.