From a personal, anecdotal perspective, the most honest way I can describe Square (NYSE:SQ) is that it’s the best company that I don’t own. Even with its leader head splitting his loyalties — CEO Jack Dorsey also shot-calls Twitter (NYSE:TWTR) — SQ stock has impressed.

Back in November 2015, the payment-processing specialist introduced Square stock to the markets. In hindsight, that represented one of the greatest long plays of all time. Starting with a lowly initial public offering price of $9, SQ experienced turbulence early on.

In January 2016, SQ stock dipped below its IPO price. While the business concept appealed to some early bird investors, critics pointed out some flaws; specifically, slowing growth and widening losses.

That thought process has all but disappeared. Today, the only people who have bad feelings about Square stock are those who abandoned ship too soon. With share prices hovering above $70, SQ has nearly increased eight-fold since its IPO.

However, the narrative now is whether SQ stock can still deliver the goods. After all, the markets are agnostic about past accomplishments. Investing is a game of “what have you done for me lately?”

Using a more recent framework, Square stock doesn’t seem so impressive. Since August 2018, the company equity hasn’t moved much. So unless something dramatic happens between now and the end of July, Square’s 52-week trailing performance risks running close to 0%.

I don’t need to spell it out for you. That would be quite a shift from earlier optimism. Thus, prospective buyers are right to ask the question: Is SQ stock a good investment now?

If you’ll stay with me on this extended analysis, I’ll show you that it is.

Square Stock Is Fundamentally Undervalued

It might seem strange, perhaps ludicrous, to suggest that Square stock is fundamentally undervalued. For one thing, the underlying company runs negative earnings. Therefore, buying shares hinges on the speculation that the growth narrative will one day decisively outpace expenses.

It’s not an easy risk. As I mentioned at the top, CEO Dorsey splits his time with social-media outlet Twitter. Considering that Twitter is becoming an arm of the executive branch, Dorsey has his hands full. Multiply that sentiment by five knowing that we’re entering a critical presidential election cycle.

But I would propose to you that SQ stock is indeed undervalued. A few pictures here would be extremely helpful in illustrating my point.

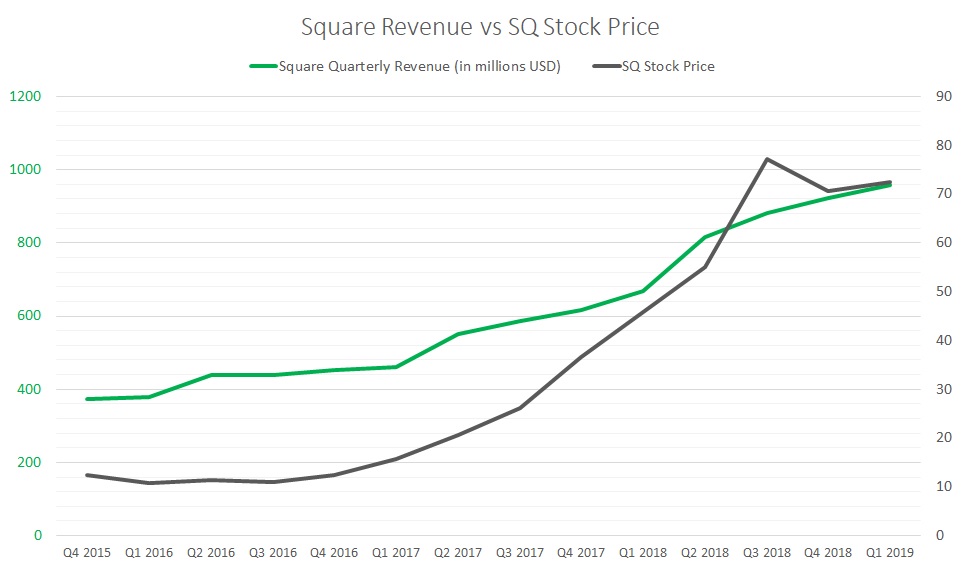

Click to Enlarge

As you can see, the markets have treated Square stock as a “show me” investment from the get-go. Revenue ramped up significantly between the fourth quarter of 2015 ($374.4 million) and Q2 2016 ($438.5 million).

Yet during that sequence, the average Square stock price dropped from $12.32 to $11.31. When sales growth failed to impress investors throughout the rest of 2016, shares went sideways.

However, that story changed in 2017, and later in 2018. Market observers saw that SQ consistently strung together strong revenue tallies. Worries about some of the granular weaknesses in the financials faded as Square’s business narrative stole the stage.

Click to Enlarge

When that happened, speculation ran wild. Quickly, the upside trajectory of SQ stock outpaced sales growth. You can see the sharp lift in the equity (compared to the steady rise in revenues) when viewing it on a logarithmic scale.

At some point, the party had to unwind. And that’s exactly what happened.

A Return to a Compelling Entry Point

But like clockwork, SQ stock is now looking like a compelling buy at this price point.

I say this because the markets rarely, if ever bring a stock down to a fair valuation immediately following a massive bull run. In virtually all cases, Wall Street excessively corrects a publicly traded company before the next leg up.

It’s no different here. When Square stock was challenging the $100 level in the back half of 2018, you could make the case that trading sentiment got ahead of itself. Sure, broader market fears and geopolitical tensions with China certainly didn’t help matters. But the primary issue remains that SQ simply needed a breather to work out the excess speculation.

I believe that the equity has received this breather. Consider that between Q3 2018 and Q1 2019, revenue jumped from $882 million to over $959 million. That’s roughly a 9% lift. On the other hand, the SQ stock price declined from $77.13 to $72.47, or a loss of 6%.

At the time of writing, the Square stock price is $71.28.

But here’s a more critical point: revenue growth has picked up intensely over the last five quarters, averaging year-over-year growth of 47.4%. In contrast, in the five quarters between Q4 2016 and Q4 2017, YOY revenue growth averaged 27.6%.

Clearly, SQ is a big mover. As I’ll explain later, the company has so many potential sales-growth channels it’s not even funny. At the minimum, we should expect out sized growth to continue.

Taking the average growth of the last five quarters and extrapolating it out to Q2 2019, I anticipate sales over $1.1 billion. At an SQ stock price of only $71, this is historically undervalued.

International Tailwinds Will Buoy SQ Stock

Of course, the caveat here is that Square stock is undervalued against my forward expectations. Anything can happen to disrupt that assumption. For example, with geopolitical tensions the way they are, the global economy could unravel. Such a circumstance would translate to SQ being overvalued, even after the sharp drop from last year.

I’m not taking the above scenario lightly, and neither should you. At the same time, even if a wide-reaching recession impacted the global economy, it won’t mean a complete standstill. People will still go to work, albeit perhaps fewer in number. And those same people will need to buy stuff, although again in fewer quantities or frequency.

As such, Square’s aggressive international expansion plans should turn out to be a net positive, even under extreme pressure. It’s also the countries that Square is expanding into that should pique investor curiosity.

For instance, the company has pushed into the U.K. and Australia. Just on the surface level, this move makes sense because of the shared language and generally similar cultures. But what really makes this move genius — and Jack Dorsey is exactly that — is the British small-business environment.

Our friends across the Atlantic have more than one million micro-businesses. This category is defined as an organization that has fewer than 10 employees. Better yet, this micro and small-business environment is robust and vibrant. Naturally, this benefits Square stock due to the underlying company’s payment-processing products and services.

Best of all, this dynamic will likely only see upside. The British working culture is changing so that society considers entrepreneurship as normal as getting a job. That means SQ is making an excellent choice entering (and hopefully dominating) early.

But Dorsey and company have an even better catalyst: Japan.

Land of the Rising Cash Flow

In terms of economic and business news, Japan has turned into an odd stepchild over the past three decades. Once a feared Asian juggernaut on the cusp of superpower status — sound familiar? — Japan Inc could do no wrong.

Then it did wrong, and the once vaunted economy collapsed. Despite best efforts from the current administration of Prime Minister Shinzo Abe, Japan has still not recovered.

It’s not that Japan is an utter disappointment. It still holds the No. 3 slot in terms of GDP. Also, the country is a critical U.S. ally located in a geographic hotspot among China, Russia and North Korea.

However, negative press hovers over Japan like a dark cloud. There’s the declining birth rate, the decades of deflation and a working culture that borders on psychotic.

And yet, Jack Dorsey, the genius, is making some very clear overtures to Japan. As you will see, this spirit of contrarianism is a recurring theme that drives SQ stock.

Unlike almost every other developed nation, Japan loves its cash. I’m not talking about money, which we all love. No, I’m referencing the format. For multiple, deep-seated reasons, the Japanese will not let go of their physical fiat currency.

Part of the problem is that the cash love affair starts at a very young age. Wired ran a story explaining the cultural undertones regarding money in Japan. Over there, families have a tradition called otoshidama, where children receive cash in highly decorated envelopes on New Year’s Day.

Actually, the overall practice is not just limited to a particular holiday, and the age limit can be much higher. But the takeaway is that tradition, culture and history are intricately linked to cash usage.

So, can Japan change? Absolutely it can!

Japanese Businesses Primed to Push SQ Stock Higher

Before I get into my argument, let me be clear: I don’t think traditions like

otoshidama will ever go out of style. Indeed, it’s such an awesome concept that the entire world should adopt it. But my point is that tradition and technology can co-exist.

Japan of all countries have proven this point. Thus, I don’t think it’s any coincidence that Dorsey is pushing so hard here.

For one thing, if this dam breaks, the Square stock price will launch into another galaxy. As I mentioned recently, Square is sitting on a veritable goldmine. Despite being one of the most technologically advanced societies ever, Japanese consumers overwhelmingly prefer cash transactions. The company that finally breaks this long-established practice will receive untold riches.

But changing Japanese habits is an endeavor wrought with failure. Where SQ can succeed, however, is through relevant strategies.

According to a study conducted by Chuo University’s Hiroshi Fujiki, Japanese consumers have many reasons for using cash. Some of the biggest factors involve speed, such as cash’s immediate closing of a transaction, or the payment processes’ quickness. Others include security concerns or the desire for anonymity.

Most of these issues are areas that Square can address immediately. Moreover, the second-biggest reason why Japanese consumers use cash is acceptance: in the places that they shop, cash is king.

What if that specific narrative changed? Installing Square’s payment-processing equipment isn’t difficult. It also gives small Japanese businesses a more equal playing field against their larger counterparts. If more proprietors bought into this concept, it can create a ripple effect that ultimately skyrockets SQ stock.

Again, it’s not a pipe dream. The Japanese love affair with cash is mostly tied to rational factors, according to Fujiki. Therefore, management just needs to find the right tweaks.

Square Stock to Get High on Cannabis

Go look at any mainstream investment-related resource and you’ll quickly come across marijuana stocks. Names like Canopy Growth (NYSE:CGC), Aurora Cannabis (NYSE:ACB) and Cronos Group (NASDAQ:CRON) have entered the collective consciousness. In short order, these and other names have become this century’s version of the Dow 30.

I’m not being facetious. Our own Will Ashworth discussed the rapid rise in popularity for marijuana stocks — and ACB in particular — among the youth. Within the youth-centric Robinhood trading platform, cannabis companies dominate the discourse.

No one is surprised at this development. As I’ve argued many times, cannabis is a transformational economic reality for the U.S. Just a few years ago, this was a strictly black-market affair. Now, several states have fully legalized weed. More will surely follow.

But what has kept cannabis-related businesses from truly prospering here is the Schedule I classification. Under this archaic policy, marijuana receives the most stringent and draconian federal oversight. Long story short, individual states can legalize weed, but Uncle Sam ultimately calls the shots.

Under a shaky arrangement, the feds reserve the right to crack down on “green” companies. However, they won’t, presumably because they have bigger fish to fry (hopefully).

But that leaves cannabis businesses and their financial backers in a precarious situation. It’s also the reason why most cannabis firms in the U.S. don’t enjoy traditional financing. But this is where Square is stepping up, and it could dramatically impact SQ stock down the line.

SQ Quietly Securing Some Green

To fill the void in marijuana entrepreneurship, Square is quietly moving into the cannabidiol, or CBD space. Just to quickly summarize, CBD is the non-psychoactive compound of the cannabis sativa plant. In other words, it has the possible benefits of cannabis but without getting you high.

Either way, the feds still classify CBD as a Schedule I drug; hence, traditional financial institutions don’t make a distinction between CBD and “regular” cannabis businesses. To them, it’s all the same: trouble.

But I appreciate the risk that Square’s management team is taking by offering a pathway for CBD financing. Sure, it’s a sizable risk because of the federal overhang. Also, marijuana companies have not garnered a reputation for stability, or even transparency.

Nevertheless, I think this is another genius contrarian move that should benefit SQ stock longer-term.

As I’ve also argued many times before, the Trump administration’s aggressive foreign policy has absorbed economic penalties. During last year’s trade war with China, the U.S. agricultural industry suffered tremendously. While we may soon see a trade deal emerge, how long will this peace last? Knowing President Trump, most likely not long at all.

Opening the door to marijuana provides an economic engine that simply didn’t exist before. As I recently stated, an extended trade war with China risks one million American jobs. Cannabis, though, represents the fastest-growing job market.

With or without trade war pressure, the White House can’t afford to ignore this economic phenomenon.

Considering that we’re nearing an election year, I anticipate a more favorable posture to weed. Plus, a more favorable administration for cannabis can launch Square stock. Because while others are running away from weed, Dorsey and his executive team are running toward it.

Don’t Forget the Fundamentals!

One of the immediate criticisms that come to mind regarding my thesis for SQ stock is the timeframe. While the factors I cite are extraordinarily bullish, they require time to build out. Moreover, these are deep-rooted issues (i.e., Japanese cash usage and Schedule I classification).

They might not even pan out the way I’m hoping.

Of course, I think they will pan out exactly like I’m hoping. But even if they don’t, you don’t have to swing for the fences with Square stock. Playing small-ball and going for infield singles is just as effective.

For those that don’t watch baseball, here’s what I mean: The bread and butter for SQ stock — small businesses — has always been the same. Square dominates this segment, and more importantly, it will continue to dominate.

While our British friends may now have a small-business culture, we’re not slouches in this department. After all, small businesses represent the engine of domestic job growth. And with the era of giant, unwieldy conglomerates slowly fading, going small will become an increasingly relevant component of our professional lives.

However, one of the factors that keep small firms stuck in neutral is that they lack a growth plan. That’s an understandable problem: proprietors are more worried about keeping afloat than writing out a long-term strategy.

Also, some common fears for people interested in starting a business but not making the jump are administrative in nature. For instance, having to deal with accounting functions drive otherwise talented entrepreneurs screaming for the exits.

But the good news: these are challenges that SQ easily addresses.

A Holistic Approach to Small Businesses

Contrary to popular assumptions, Square is more than just a payment processor. They’ve developed a comprehensive suite of products and services that can assist almost any organization at any stage. Best of all, this suite is under one umbrella.

Yes, that’s an obvious statement, but it’s also one that shouldn’t be overlooked. Speaking from personal experience, starting a business is an exciting venture. It’s a journey that I believe everyone who has the desire to do so should undertake.

But it also comes with its obstacles and challenges. For me, the additional administrative tax-preparation work was daunting. Keeping track of sales and expenses and keeping up on tax forms was always an unpleasant part of the job.

You can get used to it, and grind through the responsibilities, like I did. Or, you can take advantage of Square’s brilliant platform, which provides the tools you need to handle current tasks as well as help scale up your business. Believe me, one method is decisively quicker and easier than the other.

Furthermore, Square’s position in the small-business marketplace facilitates far-reaching synergies. For instance, big data and artificial intelligence platforms will only improve in the coming years. Plus, these technologies will become cheaper and more accessible. That means SQ clients can leverage these platforms to perform tasks that in prior generations would require a human expert.

In fact, Square has already been moving in that direction for a while. The difference today is that we’re finally seeing how all these disparate parts are coming together. Once the market realizes this narrative again, SQ stock will be off to the races.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.