Micron Technology (NASDAQ:MU) enjoyed a strong rally between June and July. The stock traded in a range below $35 and then rocked to around $47 by late July. Markets liked the third quarter 2019 report on June 25. In August, the party ended for MU stock and its chip peers as the U.S. announced it would impose another 10% tariff against China.

This undermines Micron’s recently posted strong quarterly report and outlook for the rest of the year. Micron stock is off 12.6% so far this month while the iShares PHLX Semiconductor ETF (NASDAQGM:SOXX) is down 8.2%. Micron Technology stock is sixth-largest holding among the the exchange-traded fund’s 31 semiconductor stock portfolio.

Micron Stock Rose after Q3 Report

Micron reported DRAM revenue falling 45% year-on-year as shipment volumes were relatively flat. NAND revenue fell 25% year-on-year. And even though revenue fell on all segments — Compute and Networking, Mobile, Storage, and Embedded — results were better than expected. More importantly, Micron did not take an impairment charge on inventory. In the last few months, customer inventory improvements fell in-line with expectations in most of the end markets.

Given that positive development, management reinforced its view that DRAM demand will return to healthy comparative growth in the second half of this year. Similarly, NAND bit demand is rebounding as markets respond to the price declines incurred in the last year.

To align expected revenue levels with costs, Micron announced a cut in capital expenditures. The capex cut will lower industry supply for the second half of the year. And as the industry reaches supply-demand equilibrium, inventory levels will return to normal. The capex reduction is bad news for Applied Materials (NASDAQ:AMAT) and Lam Research (NYSE:LRCX). Both companies rely on memory capex spend for their revenue growth.

Looking ahead into 2020, chances are good that Micron will cut its capital spending further, hurting Lam and Applied. Despite the weakness ahead, Lam Research stock rose by over 9% in the month, while Applied stock rose 7%. Micron’s pullback led to a 0.6% drop in the stock markets last month.

Investment Opportunity

Micron has a healthy balance sheet and is in a winning team position to pounce on markets when the industry environment eventually recovers. Long-term demand for memory and storage is still strong. Secular trends such as AI, autonomous vehicles, IoT and 5G will lead to a higher demand equilibrium for Micron DRAM and NAND products. Although the stock is up 50% from 52-week lows, the recent pullback is quickly creating another entry point for semiconductor investors.

The outcome of the U.S./China trade war is the only major headwind that all investors face. How it plays out is impossible to predict. And though it is in China’s best interest to resolve the trade dispute, the U.S. is willing to negotiate aggressively. The prolonged dispute may send Micron stock lower but that does not matter. The company already cut costs and production to bring the industry supply-demand into balance.

In the DRAM space, an increased mix will increase Micron’s revenue diversification. In the NAND space, it continues to ramp up 96 layers, while delivering on cost declines for the fiscal year. It is also making good progress on 128-layer 3D NAND, which uses a replacement gate.

Market Growth Beyond Computing

Micron’s SSD portfolio depends on sales of its latest 9300 Datacenter NVMe SSD. For its cloud customers, inventory is dropping back to normal levels. Beyond this space, the company is leading market share in the automotive space. The sector will become a bigger source of revenue for Micron. This is led by content growth, driven by advancements in in-vehicle infotainment and ADAS. In the third quarter, Micron started ramping shipments to a leading OEM’s advanced autonomous system that used 16 GB of its LPDRAM.

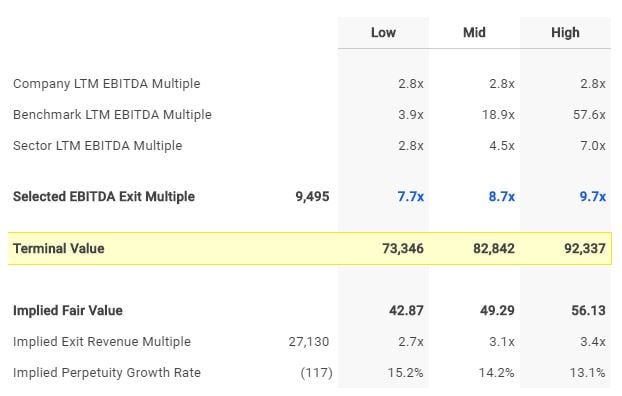

MU Stock Fair Value and Your Takeaway

At a recent price of $42.63, Micron stock trades close to the average analyst price target of $45.86 (per Tipranks). Still, the most bullish investor could use a simplywall.st valuation based on future cash flow to come up with a higher target price. The only thing holding the argument for a lofty target price is that earnings are not expected to grow next year. Still, investors could use a 5-year DCF EBITDA Exit model that assumes revenue falling in the next two years and recovering by FY2021.

Source: finbox.io (click on the link to edit your assumptions)

In that scenario, MU stock has an upside of 18%.

Micron is a volatile stock whose ups and downs comes in phases. The recent downtrend that started just two weeks ago may continue. Investors planning to hold the stock for over a year could start a position at these levels. The reward will come as prices stabilize and demand strengthens. The end of the trade war is just a bonus for MU stock.

Disclosure: As of this writing, the author did not hold a position in any of the aforementioned securities.