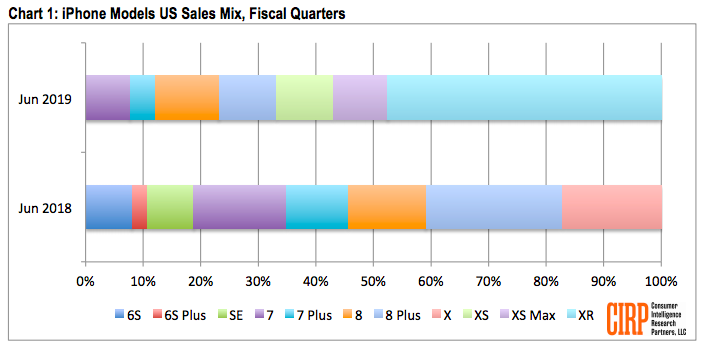

Apple’s (NASDAQ:AAPL) sales mix within the iPhone segment are moving towards lower-priced models. A recent CIRP report showed that iPhone XS and iPhone XS Max had a share of less than 20%, while the lower-priced iPhone XR had close to 50% share in the sales mix. This is a double-whammy for Apple stock as customers are delaying their upgrades of iPhones and choose lower-priced models when they do upgrade.

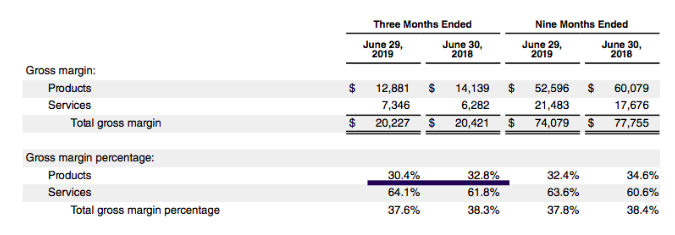

This trend has put pressure on the margins within the Products category of Apple. The gross margin for Products fell from 32.8% in the year-ago quarter to only 30.4%, a decline of 2.4 percentage points. Despite an improvement in Services margin, the fall in Products gross margin has led to 70 basis point decline in the total gross margin. Apple is also showing a decline in operating margins as the R&D expense rapidly rises.

We should see the trend of declining margins continue in the next cycle as the new iPhones will be an incremental improvement over current models. The phones unveiled during today’s Apple event won’t have 5G capability either, risking having their customers defect to rival smartphone makers ahead of the game. A big dip in margins and EPS with stagnant revenue base will limit any bullish sentiment towards Apple stock in the near term.

AAPL Stock Squeezed on Two Fronts

Source: CIRP

CIRP’s report shows that iPhone XR had a 48% share in the overall sales of iPhones in the last quarter. On the other hand, XS and XS Max have less than 20% share. Both XS and XS Max together have a share which is equal to the share of iPhone X in the year-ago quarter.

The popularity of older iPhone models, as well as XR, has limited the sales of higher-priced models. Hence, even though there is a big focus on iPhones over $1,000 among analysts and news coverage, the contribution of these models is very low.

Samsung also mentioned in its recent earnings that sales of Galaxy S10 have been weak. The two most important features desired in a smartphone are camera quality and screen size. Both these features are available in older models or the XR, which reduces the incentive to splurge over $1,000 on more pricey models.

At the same time, the upgrade cycle is getting longer with every iteration. It is highly likely that more customers will skip the 2019 iPhone cycle because of a lack of a 5G feature and few incremental improvements in the models. This will again push the margins lower for the next few quarters and shift the focus of Wall Street on the 2020 iPhone launch, a major negative for Apple stock.

Fall in Margins

Lower demand for higher-priced iPhones ends up hurting the Products margin.

Source: Apple Filings

There has been a 2.4 percentage point decline in the gross margin of Products category, a large part of which is made up of iPhones. This decline has more than made up for any positive improvements in the Services gross margin. Hence, the total gross margin has declined by 70 basis points. Even on a longer timeline of nine months, the decline in Products gross margin has been 2.2 percentage points.

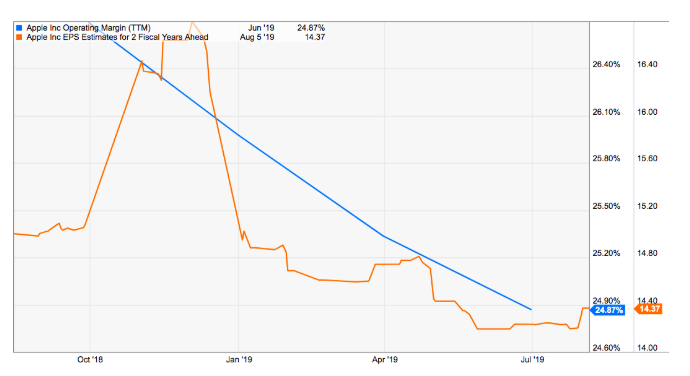

This trend has had a negative impact on operating margin which has declined by 223 basis points in the recent quarter. Apple has now reported a year-on-year decline in operating margin for 13 of the past 14 quarters. The 2019 iPhone cycle is unlikely to change this trend.

While the improvement in Service gross margin in commendable, it should be noted that in the last nine months the gross margin from Services was $21.5 billion out of a total of $74 billion. Hence, the gross margin share of Services is less than 30%.

Future Trend for Apple Stock

Faster growth in Services and a decline in iPhone revenues should lead to greater revenue share of Services. This will increase the positive impact of Services margin on the total margins, but Apple would need to deliver good margins on the new services it has launched this year.

This can be very tough considering the strong competition it will face in several services segment. For example, Apple would need to compete against some of the biggest players like Amazon (NASDAQ:AMZN), Disney (NYSE:DIS), and Netflix (NASDAQ:NFLX) to establish its video streaming business. It is difficult to see how Apple would be able to show healthy margins in this business in the near term.

A continuous decline in the operating margin will lead to further cuts in future EPS estimates. This makes Apple stock more expensive with a much higher valuation multiple.

The EPS estimates for two fiscal years ahead is close to $14 which is equal to 15 times the current Apple stock price. This might look as a reasonable multiple, but investors should also look at the possibility of further EPS decline and a stagnant revenue base.

At the current price level, Apple would need to deliver strong performance in several segments to make up for a declining iPhone business. It is highly likely that the fall in operating margin and EPS will continue in the 2019 iPhone cycle which should limit the bullish sentiment for Apple stock over the next few quarters.

Investor Takeaway on AAPL Stock

Apple’s margin for Products is falling rapidly. In the latest quarter, there was a 2.4 percentage point decline in gross margin for Products. More customers are opting for the lower-priced iPhone versions which also limits the margins in the biggest segment for Apple.

The 2019 iPhone cycle is going to have only incremental features which can limit the upgrades as customers wait out for a 5G version in 2020. Apple could be forced to give discounts to push sales which will pressurize margins and lead to further EPS decline.

Apple has reported a decent jump in Services margin. However, the new services launched by Apple are in business segments which have very low margins. In addition to that, Apple would need to compete against rivals like Netflix, Disney, and Amazon who have huge resources and are willing to operate at lower margins.

We should continue to see a decline in margins and EPS from Apple over the next few quarters which reduces the attractiveness of Apple stock as a buy-and-hold bet.

As of this writing, Rohit Chhatwal did not hold a position in any of the aforementioned securities.