Canopy Growth (NYSE:CGC) has been on a roller coaster so far in 2019. Like much of the rest of the market, Canopy Growth stock came into the year depressed and under pressure.

However, it didn’t take long for shares to go from sub-$30 to $50+ though. That price action took place in the month of January, but bulls have lost that steam.

Luckily for InvestorPlace readers, many have been bearish since $38.

After plunging all the way down to $22.76, shares are on the rebound. The hard part is determining whether this is a dead cat bounce (i.e. a temporary reprieve before more downside ensues) or a true reversal off the lows. With the recent rally, shares are no longer down more than 50% from the highs, although Canopy Growth stock still sports big losses.

Let’s take a closer look at the stock to determine what the best course of action is.

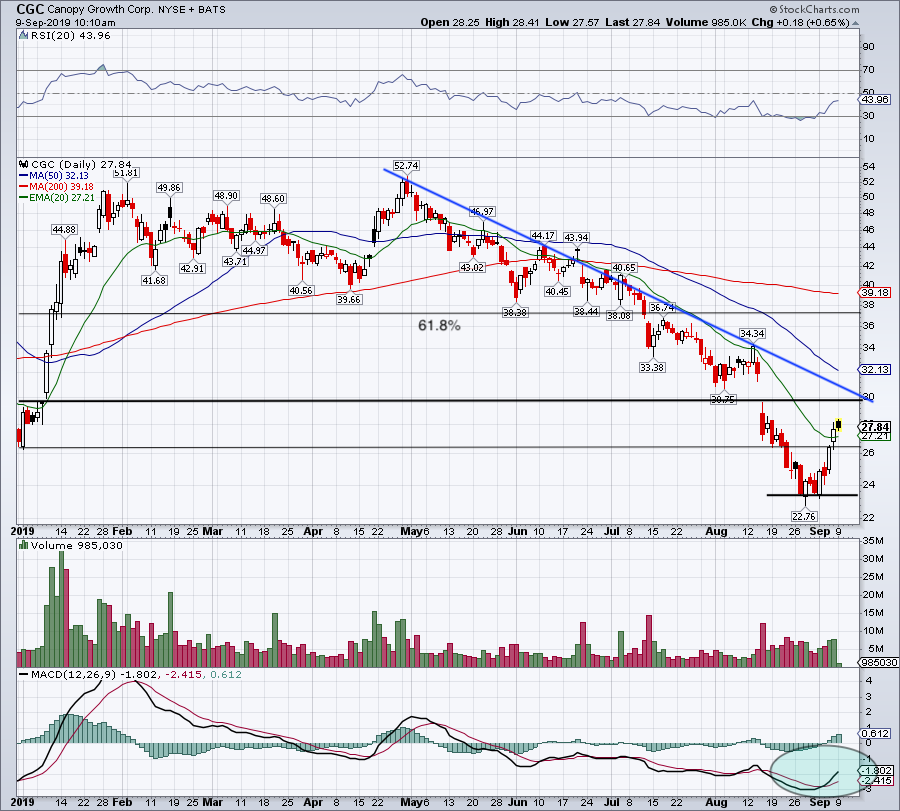

Trading CGC Stock

Click to Enlarge

Last week, CGC was a Top Stock Trade on InvestorPlace and I also flagged the name on Twitter. Even though shares are taking a breather, it’s important to see that they’re holding up above the 20-day moving average.

While it would be discouraging to see CGC lose this mark, As long as it stays above $26.25, it looks technically okay for bulls. However, the big question is whether shares can hurdle $30.

At $30, CGC stock would approach a significant level on the chart, as well as downtrend resistance (blue line). Above here and Canopy Growth stock can start working on filling the gap up to $32. There’s also the 50-day moving average up near $32, although it’s declining on a daily basis as well.

Over $32 and CGC bulls can start thinking about a return to the 61.8% retracement, which is currently north of $36. But let’s not get too ahead of ourselves. We first need to see CGC hold up over $26.25 and push through $30. After that, we can start looking at further upside targets.

Below $26.25 and the recent lows near $23 are back on the table.

Balance Sheet

CGC still has a strong balance sheet, but with negative free cash flow and M&A, it’s weakening over time.

Cash and short-term investments of $2.42 billion are down more than 32% from the quarter ending in December 2018. Current assets are down ~$916 million (-23.7%) to $2.95 billion in the same period, although total assets are up 4.2%.

That also comes with 31.3% spike in current liabilities to $284.6 million. Total liabilities have gone from $891 million six months ago to $2.1 billion, up roughly 135%.

So while total assets still outweigh total liabilities by nearly three-to-one and there are no concerns about CGC meeting its short-term obligations, the balance sheet is weakening vs. six months ago.

Sizing up Canopy Growth Stock

Many considered Canopy Growth stock (and many others still do) the

blue chip cannabis stock to be long.

It had the strongest balance sheet, early-mover advantage in both the U.S. and Canada, and strong backers via the $4 billion investment from Constellation Brands (NYSE:STZ).

But it’s not just CGC stock that’s been under pressure. We’ve seen weakness in Aphria (NYSE:APHA), Tilray (NASDAQ:TLRY), Cronos Group (NASDAQ:CRON), Aurora Cannabis (NYSE:ACB) and most others.

Many of the bullish catalysts for CGC and the cannabis industry as a whole are still in place. Both the U.S. and many parts of the globe are working toward legalization. Many companies and startups are focused on cannabis-related treatments and recreational uses.

While Canopy reported 250% year-over-year revenue growth for Q1 last month, the results missed expectations. Earnings per share badly missed estimates, although the miss can be explained away by some financial engineering related to expiring warrants. Still, it would have been nice to be provided an adjusted number in the release.

Further, it doesn’t help that Constellation Brands and Canopy’s management had a “strategy clash” in July, which results in Canopy CEO Bruce Linton leaving the company. That adds some uncertainty to the picture.

Where does that leave us? The valuation is rich for CGC and most other cannabis plays and that’s putting it lightly. That’s no secret, but when the news flow is negative and momentum is bearish, the valuation will hurt the share price. We need to see the charts start to cooperate for Canopy Growth to look good on the long side.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.