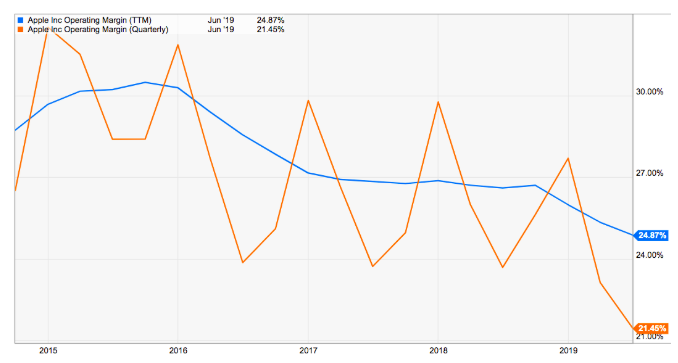

Apple (NASDAQ:AAPL) has continued to show a massive decrease in its operating margin (OPM), in the recent quarter. Apple reported OPM of 21.45% in the latest earnings. This is 223 basis points less than the year-ago quarter. It has now delivered a falling OPM in 14 out of the last 15 quarters. This trend is hurting its profits and EPS, making Apple stock more pricey on a valuation multiple.

With the increase in tariffs on Chinese imports, we should see a further decline in OPM. The company would be forced to absorb some of the tariffs to stimulate demand. If Apple’s management decides to move a part of the supply chain into other countries, it will lead to higher cost and fall in margins.

AAPL is betting on new services like video streaming which have a lower margin compared to the App store or licensing business. This move will lead to further shrinking of the margin in the near future which can hurt any bullish sentiment towards Apple stock.

Apple Stock’s Negative Trend

Fig: YOY operating margin decline shown by Apple. Source: Apple Filings, YCharts

June 2015: 28.39%, June 2016: 23.86%, June 2017: 23.71%, June 2018: 23.68%, June 2019: 21.45% Cumulative decline: (694 bps)

Sep. 2015: 28.39%, Sep. 2016: 25.10%, Sep. 2017: 24.95%, Sep. 2018: 25.62%, Cumulative decline: (277 bps)

Dec. 2014: 32.50%, Dec. 2015: 31.86%, Dec. 2016: 29.81%, Dec. 2017: 29.76%, Dec. 2018: 27.69%, Cumulative decline: (481 bps)

March 2015: 31.51%, March 2016: 27.67%, March 2017: 26.65%, March 2018: 26.00%, March 2019: 23.12% Cumulative decline: (839 bps)

Apple reported over 450 basis points of OPM decline in June 2016 quarter compared to June 2015 quarter. There was a moderate decline in OPM in 2017 and 2018. However, in the past three quarters, there has been a major downswing in OPM with over 200 basis points of decline for all the quarters in this fiscal year.

One of the reasons for this decline is the heavier discounts and exchange offers given by the company on iPhones. This strategy has helped in boosting sales to some extent but it has also ended up hurting the margins significantly.

AAPL Stock’s Main Culprit

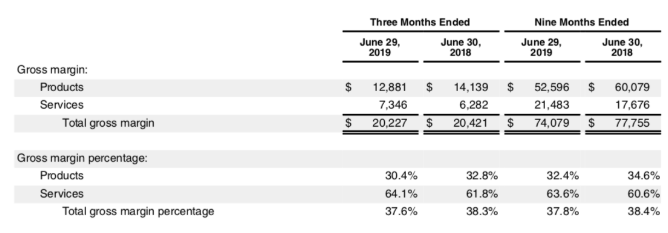

Source: Apple Filings

We can see from the above figure that Apple’s Products category has seen a massive decline in gross margins. In the recent quarter, Products had a gross margin of 30.4%, a decline of 2.4 percentage points from the year-ago period. On the other hand, Services margin has increased from 61.8% to 64.1%.

Most of the bullish analysts have estimated that the revenue share of Services will increase which will improve the overall margins. But there is a big caveat in this theory. Most of the profits made in the Services segment are from the licensing agreement with Google (NASDAQ:GOOG, NASDAQ:GOOGL) and from the App Store.

According to Bloomberg, the annual licensing revenue from Google is close to $9 billion and it would be close to the saturation point. As the unit shipments decline drastically, the growth in licensing revenue should also subside. At the same time, Apple is facing significant challenges in the App Store. Bigger players like Netflix (NASDAQ:NFLX) have moved their payments outside the App Store and the company is facing regulatory issues within this business.

The heavily-touted new services launched by Apple will not be able to replicate the massive margins of the App Store or the licensing revenues. For example, the Wall Street Journal mentioned that Macquarie’s analyst Ben Schachter has estimated that Apple Music’s gross margin is close to 15%. On the other hand, the gross margin of App Store is believed to be over 90%. As the revenue from these new services increases, we should see a decline in margins within the Services segment.

Higher Valuation Multiple for Apple Stock

One of the main arguments for a bullish rating in the Apple stock price is the low valuation of the stock compared to the broader market. However, if there is a significant decline in margins and EPS, it will end up increasing the valuation multiple, making Apple stock more expensive.

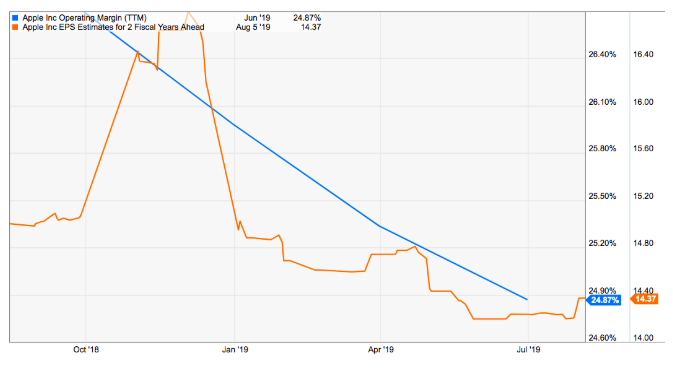

The EPS estimates for two fiscal years ahead has fallen drastically in the last two quarters. By the end of 2018, the forward EPS estimates were at $16.80 which has now come down to $14.37, a decline of 15%. We should see further downward revision in EPS estimates as the trade friction increases and the new tariffs start hurting the domestic purchases.

Apple stock showed a big correction when the new tariffs were announced. The reason is that Apple is in the front lines of a trade war with a lot of exposure to China. A longer-term trade tension will continue to be a headwind for Apple stock and can hurt the long term returns.

Investor Takeaway on Apple Stock

Apple reported 223 basis point decline in operating margin in the latest quarter compared to year-ago quarter. The trend of falling operating margin can be seen for the past 15 quarters. In the latest quarter, the downward swing in OPM has been quite high as the company is forced to offer discounts and trade-in options to increase the attractiveness of the higher priced iPhones.

Falling OPM ends up hurting EPS which has increased the valuation multiple for the stock. The current trailing twelve-month PE ratio stands at 18.5. This might look cheap compared to other stocks. However, falling EPS will make the valuation multiple higher at the same price. Trade tensions and higher tariffs should cause further margin contraction in the next few quarters.

As of this writing, Rohit Chhatwal did not hold a position in any of the aforementioned securities.