From the top looking down, the narrative for identity and access management firm Okta (NASDAQ:OKTA) is unambiguously optimistic. As everyone knows, the rise of digitalized financial and information transactions has unfortunately facilitated bad actors looking to take advantage. This isn’t just a problem for individuals as corporations are also vulnerable to critical data breaches. Addressing these 21st-century problems is what drives the OKTA stock price.

In 2017, approximately 16.7 million individuals were victims of identity theft. Given the rising scope of cybercrime, this statistic isn’t surprising. But what keeps many corporate head executives up at night is that in the same year, the National Cybersecurity Society reported a 46% increase in business identity theft cases. Most of the incidents involve monetary interests but proprietary information can carry a financial premium in the black market.

To mitigate the impact of such devastating identity and access breaches, OKTA offers rigorous, scalable protection services. Due to the company’s flexibility, corporate clients from myriad industries have jumped aboard, boosting the company’s profile.

Not surprisingly, the tech firm’s equity has doubled this year. However, all the bullishness essentially occurred in the first half of 2019. Since the start of the second half till the time of writing, the OKTA stock price is roughly flat.

For the uninitiated, this may catch some prospective buyers off guard. To help you make a more informed choice on OKTA, we’ll take a quick look at the bull and bear case.

Strong Customer Metrics Bolster OKTA Stock

Recently, the tech firm released its earnings results for the third quarter of its fiscal 2020. From most measures, it was a resounding success for management.

Prior to the disclosure, covering analysts pegged earnings per share to come in at a loss of 12 cents. Estimates ranged from -13 cents to -9 cents. However, OKTA delivered EPS of a loss of 7 cents, beating the most optimistic of targets.

On the revenue front, analysts forecasted a consensus target of $143.9 million. Here, estimates ranged from $143.1 million to $146.4 million. Again, OKTA blew these expectations out of the water, ringing up $153 million. In the year-ago quarter, the company generated sales of $105.6 million or a 45% lift.

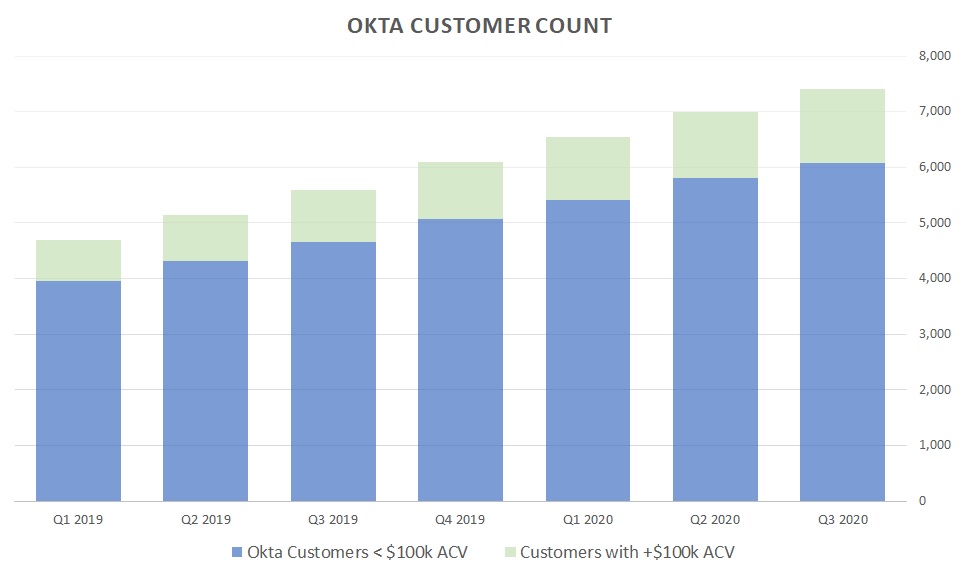

But it wasn’t just these core metrics that impressed observers. Rather, the rise in customer count gave many analysts food for thought. First, you had the total count that increased to 7,400 clients, a massive jump from the 5,600 customers (a 32% increase) from Q3 fiscal 2019.

Click to Enlarge

Second, customers with an annual contract value (ACV) over $100,000 jumped to 1,325 from 937 one year ago. Significantly, this leap of over 41% year-over-year represented a greater magnitude lift than the rise in total customer count.

Now, OKTA’s $100,000-plus ACV clients make up 17.9% of total customers. One year ago, this metric was 16.7%. In other words, not only is the company growing but they’re growing faster with high-dollar clients. That’s nothing but positive for OKTA stock.

Risk Factors Abound

But before you dive into shares, consider that not everything is well with the underlying organization.

For starters, conservative investors may not like what the financials have to offer. Although growth is impressive, OKTA continues to widen its net income losses. As a tech firm, that’s not surprising. To stay relevant and on top of the competition requires cash outlays. That means higher research and development expenses that make the earnings situation worse.

Of course, the immediate counterargument is that longer-term growth should outpace expenses. And as I just mentioned, growth is impressive. Except maybe it’s not that impressive when put into a broader context.

Click to Enlarge

This past October, I mentioned that investors may want to wait out the OKTA stock price. Part of the reason is that growth has slowed significantly from prior years. For example, the most recent quarter’s sales growth rate of 45% is down conspicuously from the 57.8% of the year-ago level.

Coincidentally, since Q3 fiscal 2019, OKTA’s sales growth rate has slipped sequentially on a consecutive basis.

To be fair, OKTA stock may be a takeover target. But as our own Thomas Niel pointed out, shares are overvalued relative to its peers. Thus, this takeover narrative may not hold water for some time.

How to Approach Shares

Ultimately, I believe that OKTA stock facilitates an interesting take on an increasingly important industry. Furthermore, I’m encouraged that high-end clientele are making up a greater portion of the company’s customer count.

However, shares have some upside resistance due to some less-than-favorable financial metrics. As a relatively small company (and therefore aided by the law of small numbers) growth should be robust. It is but the rate is noticeably declining.

In the long run, shares might do well, so I’m not opposed to a bullish position. However, waiting a little bit for a better entry point isn’t a bad idea.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.