Despite the awful nature of the novel coronavirus, for some organizations, earnings season is a way to set the record straight, promoting a more positive perception. In all likelihood, this will not be athletic apparel maker Under Armour (NYSE:UA, NYSE:UAA). Already playing second fiddle to leaders Nike (NYSE:NKE) and Adidas (OTCMKTS:ADDYY), the company had a tough road prior to the pandemic. Now, it’s difficult to see how Under Armour stock will get out of this bind.

Ahead of UA’s first quarter of 2020 earnings report, covering analysts are forecasting earnings per share to come in at a loss of 21 cents. This is a brutal fall from the year-ago quarter, where Under Armour delivered EPS of 5 cents. Consensus at the time called for a loss of a penny.

Unfortunately, things don’t look better for Under Armour stock on the revenue front. Analysts are targeting $981.7 million, with individual estimates ranging from $857.3 million to $1.2 billion. In Q1 2019, the company rang up $1.2 billion in sales.

While I don’t have a crystal ball, I would be shocked if UA comes close to either target. Overall, the reality is that the retail segment is the worst-hit sector in the economy. Obviously, no one wants to buy anything that isn’t essential. Unsurprisingly, within this ugly market is the clothing and accessories sub-segment, which has incurred the greatest losses.

Some might take a contrarian position for strong apparel companies like Nike. Clearly, they have a loyal user base that could help sustain shares. But with UA, I just don’t see it. Unless the company can quickly shift the narrative, Under Armour stock remains very risky.

Lack of Relevancy Will Hurt Under Armour Stock

If you’re the type that wants to go contrarian during this market downfall, I’d take a look at another candidate. With such uncertainty clouding the global economy, many good companies are vulnerable to volatility. However, Under Armour is far from a worthwhile organization.

First, according to Matt McCall, his inside source indicated that the toxicity that had earlier plagued Under Armour stock has yet to be fully expunged. That’s just not acceptable in the modern “woke” environment.

But more critically, UA has failed to keep up with its industry’s trends. At a time when its competitors have shifted aggressively toward fashion-centric footwear, Under Armour insisted on the opposite direction. Rather than optics and pop-culture relevance, their products are geared toward athletic performance.

Such a decision may impress the world-class athletes that UA has endorsed over the years. But not that people on this planet have such talent. Therefore, it’s understandable that consumers want something that is more pertinent to their lifestyle. Besides, management made the almost unforgivable business mistake: not giving the customer what they want.

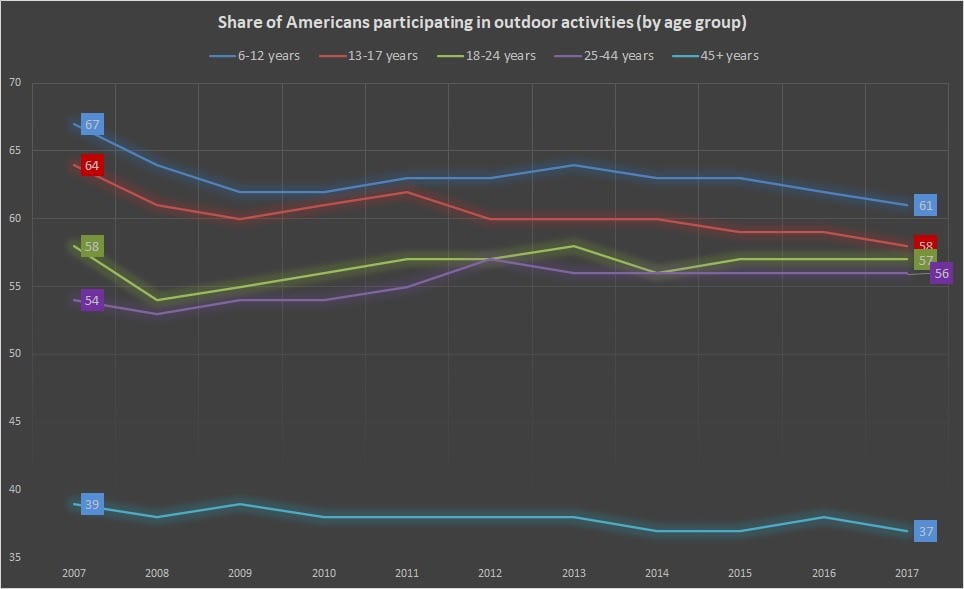

Not only that, demographic trends have clearly indicated that Under Armour’s competitors made the right strategy call. According to a survey from the Outdoor Foundation, most demographics in the U.S. have seen a decline in outdoor-activity participation. Only one demo, the ages 25 to 44 group, saw a slight uptick, from 54% of the category in 2007 to 56% in 2017.

Click to Enlarge

Most worryingly for Under Armour stock is the younger demos’ declining affinity for outdoor activities. As younger populations grow older, they’re likely to carry their relatively sedentary lifestyles forward (as the data shows).

Understanding this, Under Armour should have shifted their priorities toward fashion-centric products. They refused, which could hurt them now.

UA Put Themselves Out of the Game

In the best of circumstances, Under Armour would have been a risky bet. A toxic culture combined with irrelevant products usually spells disaster. But now that the retail market has turned into a game of musical chairs, UA finds itself in the worst situation possible.

Essentially, the company knocked itself out of contention. Last week, the Department of Labor revealed that an additional 4.4 million Americans filed for unemployment benefits. Over a five-week period, more than 26 million have found themselves jobless. When you factor in certain elements such as millions unable to reach their state’s benefits office, the unemployment rate today could be 20% or more.

In this new normal, I find it extremely hard that the average consumer will willingly spend excess funds on non-essential discretionary items. If they do, I imagine those purchases will be carefully deliberated.

Therefore, I don’t see a winning path for Under Armour stock. The consumer has no money. Worst of all, UA isn’t giving them what they want anyways.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.