Currently, fundamental indicators suggest that contrarians take the bullish approach to credit card giant Visa (NYSE:V). For one thing, U.S. novel coronavirus cases appear to be flattening, implying that the worst is over. Second, previously impacted nations are slowly opening their economies, which obviously bodes well for V stock. But for investors, it all comes down to consumer sentiment.

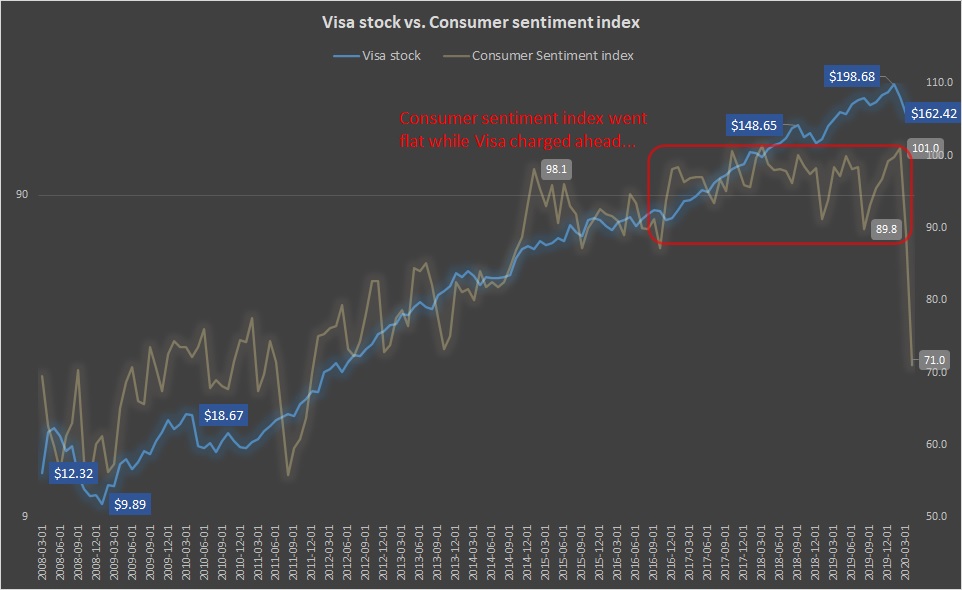

In December, I discussed the relationship between V stock and consumer sentiment. Unsurprisingly, if the consumer is confident about economic prospects, Visa shares tend to perform well. However, I noticed an interesting break in this longstanding relationship.

But since 2017 – coincidentally the beginning of the Trump administration – Visa stock has enjoyed tremendous demand. However, consumer sentiment is not keeping up. In fact, it’s moving down rather sharply this year compared to last. Thus, we have an inverse relationship: V is moving higher, but consumer sentiment is weakening.

What gives me pause is the unusual nature of this trend. Since Visa became a publicly traded equity, it has closely tracked consumer confidence. Again, you would expect this relationship. But that all changed once Trump took office.

Am I blaming him for this phenomenon? No. One person can only do so much. But something is happening here, suggesting a cautionary approach.

If only I would have known that this “something” was the coronavirus! Then, I would have warned everyone to avoid V stock – you know, because I don’t hold public office.

Click to Enlarge

But today, we have an even more peculiar situation: the consumer sentiment index was rocked but V stock is still trading at respectable levels.

Can this absurd situation last or should you abandon ship?

The Slim Window of Opportunity for V Stock

At first, you’d think that Visa is a no-brainer to dump. One of the most painful aspects of the Covid-19 pandemic is that it has affected all of us substantially.

True, those who are suffering the most are families who have lost loved ones. But even young, healthy Americans are impacted, particularly regarding their livelihood.

This segues into the biggest concern for V stock and other bellwether investments. According to the Washington Post, 5.2 million people filed for unemployment benefits

last week. Thus, over the last four weeks, 22 million workers lost their jobs.

Moreover, two economists that the Post interviewed stated that the U.S. unemployment rate is already over 20%. If so, that would put an immediate damper on V stock, which obviously depends on positive consumer sentiment.

However, it’s fair to point out that the economic devastation has sharply impacted certain sectors over others. Logically, retail sales are down but within this broad segment, clothing and accessories took the most sizable drop between February and March at a 50.5% loss. The other hardest-hit retail segments are restaurants and bars and furniture/home furnishing services, down 26.5% and 26.8%, respectively.

Naturally, you would expect that the millions who lost their jobs worked lower-paying positions in these sectors. And that’s exactly what the Bureau of Labor Statistics suggested during its most recent Employment Situation Summary, stating, “About two-thirds of the drop [job losses] occurred in leisure and hospitality, mainly in food services and drinking places.”

Typically, older demographics utilize Visa cards the most. Plus, older people usually earn more, which statistically leads to higher savings. Therefore, the bulk of the credit card company’s prime customers are largely insulated from this sudden economic crisis.

Not Worth the Risk

If you’re going to gamble on V stock, you really need a V-shaped recovery. Should that happen, then yes, Visa’s prime consumer base is insulated and can supply necessary financial firepower.

But if we have a prolonged road to recovery, then buying Visa stock now makes little sense. For example, while the obvious retail segments are hurting, if this pain continues, then it’s only a matter of time before other segments start tapping out.

Primarily, I’m looking at motor vehicle sales and the energy industry. These sectors offer myriad employment opportunities, many of them high paying. If they go under, that will cause a ripple effect throughout the economy.

And let’s not forget that while it’s great to see Kroger (NYSE:KR) and Clorox (NYSE:CLX) turn into sexy names, they were never meant to have such appeal. We’re supposed to be a nation of innovators, not a nation of toilet paper hoarders.

Therefore, with so many areas of the economy flashing red, I’m reluctant to get involved with Visa. Maybe it will be attractive at some point, but not today.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.