Like most energy stocks, Energy Transfer (NYSE:ET) stock has been hammered this year. How couldn’t it, given the supply glut and extreme volatility in crude oil? From peak to trough, ET stock fell more than 70% from its 2020 high.

However, recent bulls have been rewarded. From the March lows, shares have more than doubled. Despite the rebound though, ET stock still pays a dividend yield of almost 16%.

For most investors — myself included — seeing a dividend yield approach 20% is a red flag. There’s something seriously wrong when a company’s payout swells that high. It doesn’t mean it’s unsustainable, but it certainly means it deserves some extra scrutiny.

Valuing ET Stock

On Monday May 11th, ET stock reported earnings after the close. A loss of 32 cents per share missed analysts expectations by 66 cents, as the consensus expected a profit, not a loss in the quarter. Revenue fell 11.4% year-over-year to $11.63 billion, which came up well short of analysts’ expectations of $14.4 billion.

However, there’s a reason shares weren’t hammered in after-hours trading. While the company’s $855 million loss was unexpected, it also included a $1.3 billion non-cash goodwill impairment charge. Impressively, adjusted EBITDA came in at $2.64 billion for the quarter, down just $100 million year-over-year. For the year, management expects adjusted EBITDA of $10.6 billion to $10.8 billion.

The company will also cut its capex by $400 million to $3.6 billion. Additionally, there’s another $300 to $400 million worth of capex being reviewed for potential reductions. This is all just extra conversation for many investors though, because all they really care about is the dividend. In the earnings release, the company said:

“Distribution coverage ratio for the three months ended March 31, 2020 was 1.72x, yielding excess coverage of $594 million of Distributable Cash Flow attributable to partners in excess of distributions.”

A distribution coverage ratio below 1 would be a concern and suggest that the payout may be unsustainable. At 1.72 times, the payout from ET stock should be okay, particularly if we get a rebound in crude oil prices. Lately, that’s been the case as demand picks back up and as production moderates.

Of course, no one can guarantee Energy Transfer’s distribution. However, the quarter has now come and gone and management seems completely focused on reducing capex and maintaining positive free cash flow. That should bode well for ET stock and its payout.

Trading Energy Transfer Stock

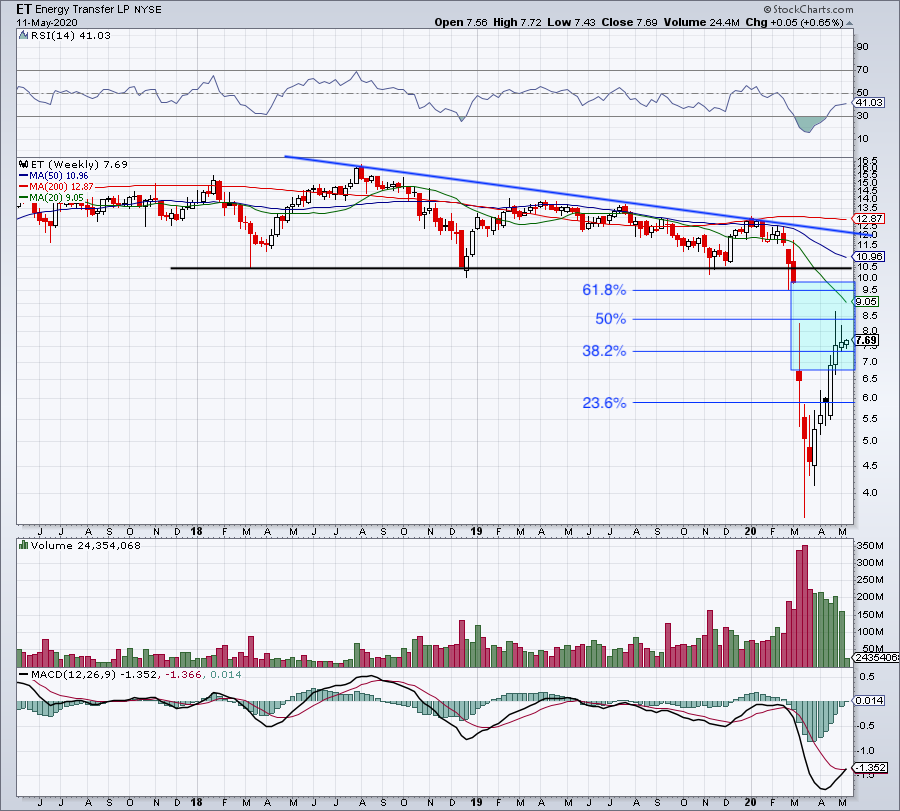

The chart looks about like what one would expect for a security that’s fallen more than 70% at one point. However, when we zoom out to a multi-year weekly look, we can see just how much Energy Transfer has been struggling.

The stock has put in a series of lower highs since mid-2018. Each dip down to $10.50 was bid back up, as this level stepped in as support. That is, until February 2020.

While shares initially broke down to $9.50 and rebounded back above the key $10.50 level, ET stock broke back below this mark the very next week, closing below $10. It opened the next week with a brutal gap down near $6.75 before plunging below $4 in the following week.

The selling pressure was unrelenting during this stretch. However, ET stock eventually stabilized near $4.50 and has begun filling into the gap (blue box). Now what?

I would really like to see ET stock hold up in this gap by staying above $6.75. If it can continue higher, let’s see if we can eventually get a gap fill up toward $10. That will require the stock to push through the declining 20-week moving average, as well as the April high near $8.69. Above these two levels puts a gap-fill in play.

Below $6.75 puts the 23.6% retracement just below $6 on the table. If investors find Energy Transfer too risky, they can always opt for an oil major like Exxon Mobil (NYSE:XOM) or an exchange-traded fund like the Energy Select Sector SPDR ETF (NYSEARCA:XLE).

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he held no position in any of the aforementioned securities.