With the devastation that the novel coronavirus imposed on the oil and gas industry, it’s a wonder that Halliburton (NYSE:HAL) was able to score any positives from its otherwise ugly first quarter 2020 earnings report. On an adjusted basis, the company delivered earnings per share of 31 cents. This beat the consensus target of 24 cents. From there, it was fundamentally all bad news for Halliburton stock.

For one thing, the drilling services company posted a $1 billion net loss. Additionally, management closed $1.1 billion in impairment charges related to the Covid-19 pandemic. As well, revenue dropped from the year-ago quarter by 12% to $5 billion. In response to the unprecedented turmoil, HAL reduced overhead expenses by roughly $1 billion. Further, the leadership team is cutting capital expenditures to $800 million.

Not surprisingly, there were human costs as well, with the company laying off hundreds and furloughing thousands. Perhaps a token show of solidarity, executives announced voluntary pay cuts.

Amid these disclosures, though, Halliburton stock technically benefited from strong momentum. Following the Q1 earnings report, HAL has posted robust double-digit gains. At the same time, I think it’s fair to point out that cost-cutting measures have a tendency of exciting shareholders. But the question now is, will this be enough to save shares?

Although I generally have a contrarian mindset, I don’t see a rational pathway for Halliburton stock to recover longer term. Yes, in the nearer term, sentiment can turn irrational. Eventually, though, I believe that fundamentals eventually matter.

And that’s really the true story behind Halliburton. This is a narrative that is focused on finding the new normal of rational valuation.

Halliburton Stock Is Currently Trading in Denial

Underlining the enthusiasm for Halliburton stock is the concept of the V-shaped recovery. As President Trump reminded us during the last State of the Union address, the economy prior to the coronavirus was strong. Indeed, he would probably say it was the best economy in the history of the world.

Assuming this is true, the Covid-19 pandemic is “merely” a black swan event. Yes, it’s a horrible situation. But once we take care of it, the economy will bounce back; hence the term, V-shaped. Naturally, this bodes well for HAL, along with other major oil players such as Exxon Mobil (NYSE:XOM) and Chevron (NYSE:

CVX).

But what if the initial assumption wasn’t true? What if the economy was already weak despite strong headline numbers and that the coronavirus only exposed the ugly truth? In that scenario, Halliburton stock wouldn’t be so appealing in its current bounce-back trajectory.

But that’s my argument. Moreover, I have the data that every prospective Halliburton buyer should consider.

Click to Enlarge

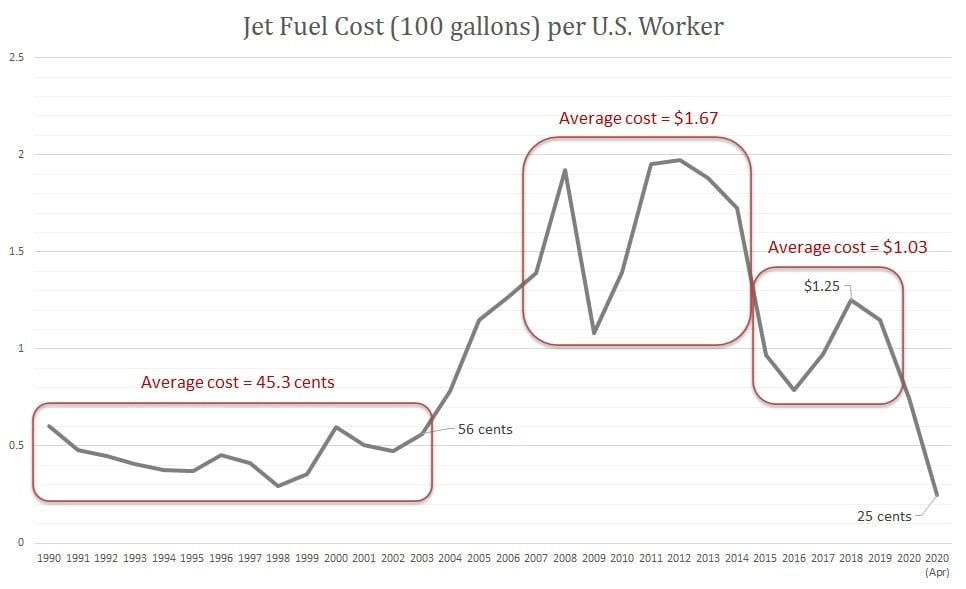

Currently, one of the biggest oil-related markets that has suffered is jet fuel. With dramatically fewer people flying, it’s no shock that demand has plummeted. But when you consider jet fuel (per 100 gallons) costs per each worker in the U.S. labor force, you quickly realize that the heady days from the mid-2000s to last year were economically unsustainable.

In fact, jet fuel costs were already declining sharply from their all-time highs well before the coronavirus. Really, the pandemic only accelerated an already negative trend.

Right now, every U.S. worker is paying about 25 cents per 100 gallons of jet fuel. Given the immediate chaos, this price could drop even more. But when it recovers, I believe the price will settle in an economically feasible range, around 50 to 60 cents.

The New Reality Will Haunt the Oil Industry

Back between 1990 to 2003, the average per-worker cost of jet fuel was 45.3 cents. Between 2007 and 2014, the average cost spiked to nearly $1.67, or around a 268% increase.

During the two time frames, the U.S. labor force increased an average of 14%. Therefore, you would expect some increase in jet fuel because of higher demand. Plus, you can assume a premium because job growth equates to higher discretionary incomes. But a 268% premium in jet fuel? I don’t think that’s reasonable.

Obviously, there’s not much you can do when big oil sets their prices. Therefore, the regular joe was forced to pay up. But again, this coercion just wasn’t feasible. I’m not saying it — the free market gave the clearest indictment against the oil companies.

And this why I’m hesitant to buy Halliburton stock. I just don’t think the industry recognizes that they’re in a new paradigm. Furthermore, we will likely never see the prices that we saw during the 2011 commodities boom for a long time.

Sure, they’ve made their cuts. But when you repeat the above exercise with data from other oil segments, such as gasoline, you’ll find a similar picture. Gone are the crazy days of the old normal. We’re now entering a new normal of austerity.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.