JetBlue (NYSE:JBLU) has quietly been one of the best airline stocks in the group. That’s not to say JBLU stock hasn’t had its share of turbulence, but relative strength compared to many of its peers is a good sign.

Shares are still down about 44% from its 2020 highs, but it lags only Southwest Airlines (NYSE:LUV), which is down about 38%.

It’s only slightly better by American Airlines (NASDAQ:AAL) and Hawaiian Holdings (NASDAQ:HA), but either way, JBLU is looking good. Can the airline maintain altitude and continue to outperform? Let’s dig a little deeper on this one.

Valuing JetBlue Stock

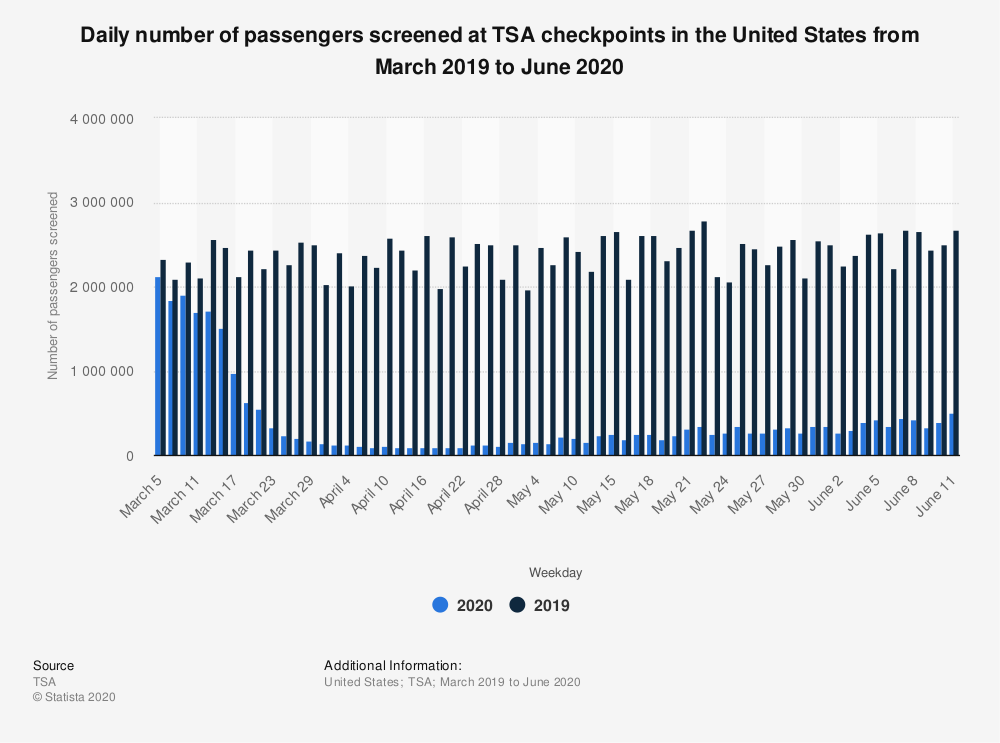

Making a fundamental case for the airline group is difficult, to say the least. Revenue was almost shut off overnight, as passenger volume dried up across the board. We know this by looking at TSA traffic across U.S. airports. Traffic dropped by more than 90% at its trough and has been quite slow to recover.

While the “reopening America” trade

has been in full force over the past few weeks, the fundamentals tell a different story. Airlines are burning millions of dollars per day. That’s even as traffic comes back faster than previously expected.

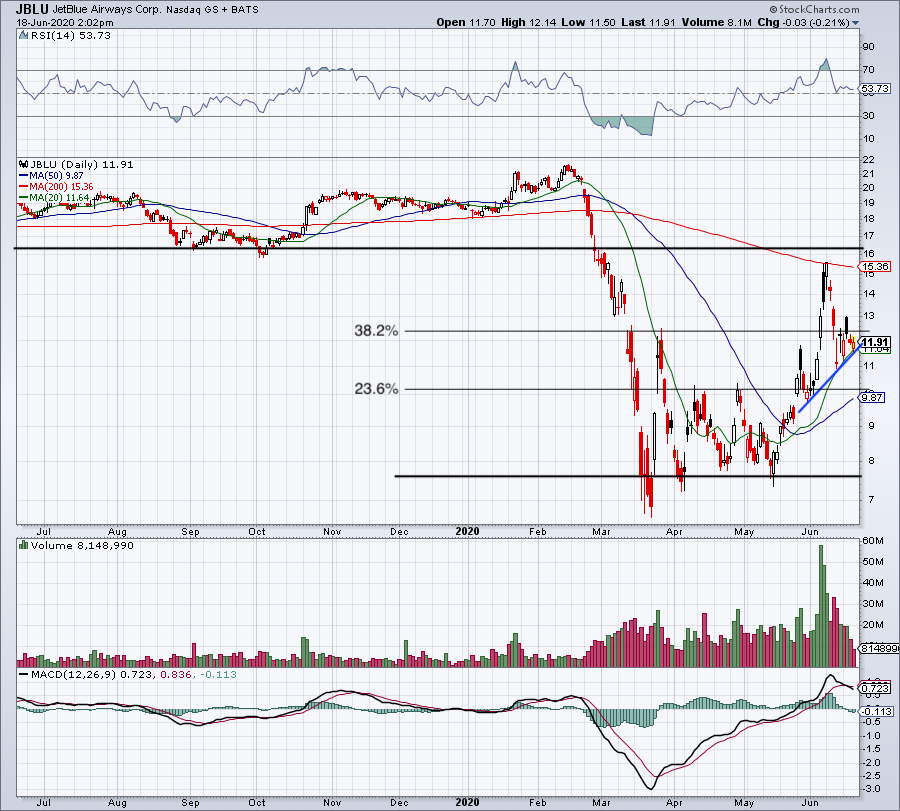

Click to Enlarge

While Delta Air Lines (NYSE:DAL) and others are looking to lower their cash burn down to a $50 million per-day average by the end of the quarter, JetBlue is much lower than that. Of course, having a market cap of just $3.2 billion versus Delta’s $19.5 billion market cap helps in that regard.

But JetBlue expected its cash burn to fall below $10 million per day in May and down to $5 million per day through the end of Q3 (JetBlue is in fiscal Q2 right now). At the end of April, the company had more than $3 billion in liquidity, ensuring that the current cash burn will not force JBLU stock into a liquidity issue.

That is, assuming we continue to see a return to normalcy among the public and do not see a second wave of the novel coronavirus trigger a series of lockdowns across the U.S.

For JetBlue, analysts expect the company to lose $3.50 per share this year, as revenue sinks 53% to $3.8 billion. These estimates are bound to change, but because the company is a regional carrier rather than having a large international presence, it’s forecast to rebound more quickly in 2021 than some of its peers.

Consensus expectations call for a 63% rebound in sales next year, alongside earnings of 44 cents per share. While not wildly profitable, a return to stability will bode well for investors. Although one should know, this industry will have a multi-year struggle/recovery in effect for quite some time.

Trading JBLU Stock

Click to Enlarge

If JetBlue is such a leader among its peers, what does its chart look like?

The decline was brutal, just like it was for the rest of the industry. However, the rebound has been solid over the past month. In mid-May, JBLU stock flirted with a breakdown below $7.50.

However, shares then reversed higher, ultimately doubling until they hit the declining 200-day moving average. Now pulling back, JetBlue is finding support along the 20-day moving average. It’s also putting in a series of higher lows.

From here, let’s see which way JBLU stock goes. On the upside, a move over the 38.2% retracement at $12.36 could trigger a rotation back over $13. If that’s the case, we could see a gap-fill up toward $14.25, followed by a retest of the 200-day moving average.

On the downside, see that current support continues to hold. If it fails, it puts $11 in play, followed by the 23.6% retracement near $10 and the 50-day moving average.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he did not hold a position in any of the aforementioned securities.