Between June and present, CrowdStrike Holdings (NASDAQ:CRWD) tested the $100 level only to bounce higher. Last week, sentiment on CRWD stock completely shifted for the worst. Bearishness accelerated and by the end of the week, the stock lost 10% of its value.

With no news releases from the company, why did the stock fall? The Nasdaq composite rose by 2.1% last week. Short float is only 5.4% of the float.

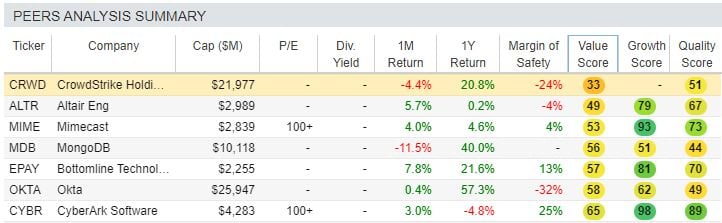

CRWD Stock Is Overvalued

Based on its future cash flow discounted to present value, CrowdStrike is worth around $89 (according to simplywall.st). Analysis at StockRover is even more bearish. In its research, its fair value on Crowdstrike is $77.48.

Click to Enlarge

CrowdStrike has the lowest value compared to its peers. Investors are better off considering Mimecast (NASDAQ:MIME) or MongoDB (NASDAQ:MDB). Both stocks have a higher value score. Conversely, not a single analyst has a price target below $100 issued in the last two months (per Tipranks).

Strong First Quarter

Investors will have to wait until September when CWRD stock posts second-quarter results. For now, it will have to rely on its Q1 numbers. The company demonstrated strong momentum for its cloud-native software as a service endpoint security platform. Annual

recurring revenue grew an astounding 88% YoY to $686 million.

Subscription revenue accounts for 91% of the total, up 89% from last year. It ended the quarter with 6,261 subscriptions.

Subscription revenue is favorable to investors for its predictability. Customers will not suddenly stop paying fees, so CrowdStrike may forecast its revenue accurately. The strong quarter is accompanied by the company’s use of the hottest technology, namely cloud-scale artificial intelligence. By accurately detecting threats, corporations are protected from cyber-attacks.

Risks For CWRD Stock

CrowdStrike’s failure to protect its clients would undermine investor confidence. But the company captures over 3 trillion events and uses AI power, plus local and cloud machine learning models in detecting threats.

Its Falcon platform is affordable, costing just $899 to $18.99 a month for clients. The company offers a free trial. Customers get to compare the protection offered against that of Nortonlock (NASDAQ:NLOK) or BlackBerry’s (NASDAQ:BB) Cylance. A high conversion rate to paying subscriptions would justify the nearly 40x price-sales multiple.

Related Investments

Okta (NASDAQ:OKTA), whose valuations are also unfavorable, offers corporations protection against data breaches. When it reports results later this month, it will likely post strong revenue growth again. In the first quarter, Okta posted first-quarter revenue growing 46%. Subscription revenue grew 48% on a year-over-year basis. It forecast revenue growing 31% to 33% to $770 million to $780 million for the fiscal year 2021.

Both Okta and CRWD stock trade at similar market capitalizations. Okta was founded in 2009, while CrowdStrike was founded in 2011.

CrowdStrike’s large and expanding addressable market suggests its revenue growth is sustainable. For example, it targets distinct silos in information technology departments, such as operations management and threat intelligence services, through CrowdStrike Cloud Modules. Looking ahead, connected devices are growing in the corporate world. The company expects its five-year compounded annual growth rate will be at least 10%.

The combination of strong retention rates and an expanding addressable market suggests that the company may expand its operating margin. The company has a long-term target of achieving an operating margin of 20% or more. It will still spend up to 20% of its revenue on research and development. So long as subscription gross margin reaches 80% of revenue, the company will reach profitability within a few quarters.

CrowdStrike is a compelling growth story. Technology investors should keep an eye on it and consider buying shares if the company posts strong revenue growth again in the next quarter.

Disclosure: As of this writing, the author did not hold a position in any of the aforementioned securities.