Facebook (NASDAQ:FB) shares are up about 72% in the past six months and about 23% year-to-date. Moreover, Facebook stock still looks liked good value here, as its free cash flow ramps up from a recent low point.

Facebook’s performance is a lot better than one of its peers in the digital advertising arena, Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL). It has risen just 33% in the past six months and about 9% year-to-date.

But Facebook stock is likely to rise at least another 33% over the next year. This is because its free cash flow (FCF) and earnings will pull the stock higher.

Facebook’s FCF Margins and FCF Yield

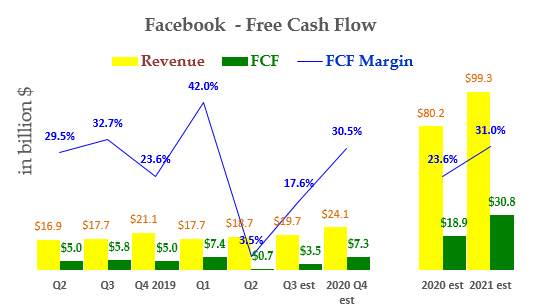

Facebook’s free cash flow (FCF) hit a recent low in Q2 2020. It made $652 million in FCF on revenues of $18.7 billion. This means its FCF margin was just 3.5%.

But if you look at the chart I prepared the right you can see that the company has typically made much higher FCF margins.

Click to Enlarge

Its Q3 and Q4 forecast margins are likely to be much higher. That is because sales will rise but its capex spending will be roughly level.

The chart shows that FCF margins for 2021 will likely be more normal levels of around 31%. This implies that its FCF will actually rise to about $31 billion.

That will have a direct effect on moving Facebook stock higher. For example, Alphabet trades at about an average FCF yield of 3.1%. FCF yield is the ratio of FCF divided by its market capitalization.

Applying this FCF yield measure to Facebook stock produces an estimated price of $343.43. Here is how that is done. Take $31 billion and divide it by 3.1%. The result is a market cap of $978 billion.

Now, since Facebook has 2.849 billion shares outstanding, dividing that market cap by 2.849 equals 343.43 per share.

Therefore, Facebook stock is worth $343.43 per share using FCF yield analysis, an upside of 36% over $252.53 (Sept. 18).

Valuing Facebook Using Historical P/E

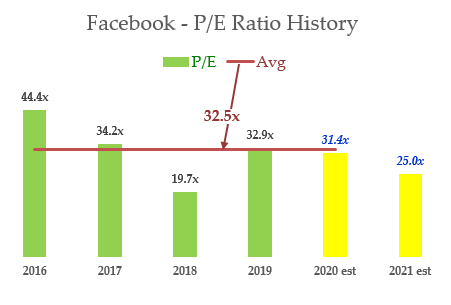

Another way to value Facebook stock is to compare it to its historical price-earnings ratio (P/E). If you look at the chart on the right that I prepared you can see that the average P/E ratio is 32.5 times earnings.

Click to Enlarge

However, earnings estimates are set to rise by 25.9% in 2021 from $8.03 EPS to $10.11. The chart shows that the P/E for 2021 will be just 25 times earnings.

That means that the stock is at least 30% lower than it would be once Facebook stock moves to its historical P/E average.

Of course, there is no guarantee that this will happen. However, over time, investors notice that reversion to the mean is often a theme that plays a role in a stock’s valuation.

What’s Next With Facebook Stock

Therefore, we now have two valuation reference points for Facebook stock. Using FCF yield, it is worth $343.43, or 36% more. And using historical P/E ratios, it is worth $328.94, or 30% higher than today.

The average of these two is $336.18, or an upside of 33%. Even if it takes to the end of 2021 for that to occur, the stock will gain 25.6% on an annualized compound basis over the next year and a quarter. These are very decent ROI numbers for most investors.

At least one major analyst agrees with this price target. Barron’s recently reported that UBS analyst Eric Sheridan likes the company’s new e-commerce initiatives.

Facebook wants to diversify into other revenue streams than just advertising. It set up Facebook Shops, which is targeted at corporate retailers selling their goods in an online store. Facebook Shop is a new app primarily for online corporate store catalogs.

It also has Facebook Marketplace, which is targeted for people selling their own goods. Moreover the company also has a payment technology division it hopes to build up. According to the UBS analyst Sheridan, Facebook hopes to reach more than $10 billion in e-commerce sales by 2024.

That would be about 10% of its revenue by 2021. It will likely have lower FCF margins.

Sheridan has a “buy” on the stock and believes it is worth $330 per share. That is close to my price target of $336.

On the date of publication, Mark R. Hake did not have (either directly or indirectly) any positions in any of the securities mentioned in this article.

Mark Hake runs the Total Yield Value Guide which you can review here.