Though some sectors are slowly making a comeback from the novel coronavirus catastrophe, this optimism doesn’t apply to the oil market. Indeed, it’s hard to imagine if “black gold” will ever be the same. Certainly, prospects look particularly dim for embattled organizations like Occidental Petroleum (NYSE:OXY). On a year-to-date basis, OXY stock is down 72%, conspicuously more than the broader industry’s decline.

However, the case for Occidental isn’t completely bearish. Due to the company’s acquisition of Anadarko Petroleum last year, Occidental has attractive assets that should generate cash if oil prices recover. According to the Wall Street Journal:

Buying Anadarko effectively doubled Occidental’s production rates, S&P Global Ratings notes. The company is now the largest producer in the prolific Permian Basin, as well as the DJ Basin, and also a top producer in the Gulf of Mexico.

However, oil prices moving high enough to save OXY stock is not a guaranteed event. Unfortunately, because of the sharp decline in the share price since early June, Occidental’s market capitalization is only $11.4 billion at time of writing. But its long-term debt has ballooned to slightly over $36 billion.

That leaves management with fewer options available to keep the ship afloat. From the WSJ article mentioned above, Occidental “might need to continue issuing discounted stock” to Warren Buffett’s Berkshire Hathaway (NYSE:BRK.B) to “pay coupons on preferred shares used to secure Anadarko.”

It’s an awful situation for stakeholders of OXY stock. Additionally, the outside fundamentals don’t spell confidence for any embattled oil firm. Yes,

air passenger volume has roared relative to its April lows and automotive traffic has improved significantly.

Still, it’s not enough to move the needle for Occidental.

The Game Has Changed for OXY Stock

Despite the ugliness in the oil sector, I expect several names to survive. Sure, electric vehicles are crowding into the automotive space. Further, remote work could at least mitigate high-congestion commutes for the next few years. However, for OXY stock, the future looks very bleak.

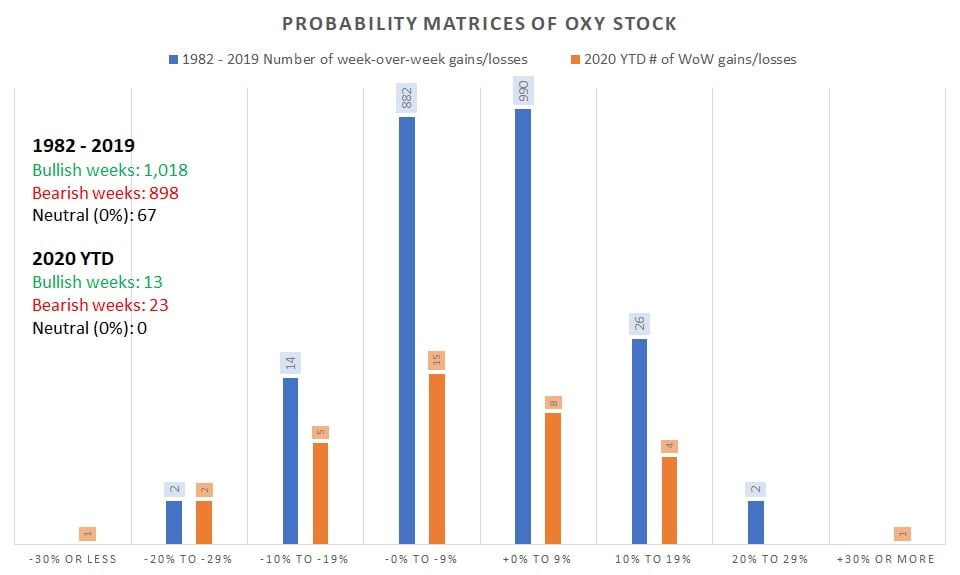

Primarily, the nature or “personality” of Occidental’s price action has undergone a paradigm shift. Of the 20 worst week-over-week performances of OXY stock, seven of them have occurred this year. That’s a whopping 35%, averaging a loss of nearly 21%.

Click to Enlarge

Moreover, from 1982 through the end of 2019, investors had a higher probability of being profitable with OXY stock on any given week. For price action between -10% to +10%, most of the week-over-week performances (990 weeks versus 882) yielded gains.

In the rare cases where OXY’s performance came in between 10% to 20% (or when the stock fell between a loss of 10% to 20%), the bulls still had the upper hand (26 positive weeks versus 14 losing weeks).

This year, the playing field has completely changed. For price action between -10% to +10%, the bears took control of 15 weeks while the bulls only grabbed eight weeks. In the plus/minus 10% to 20% category, sellers had the slight edge over buyers, five weeks to four.

Alarmingly, OXY stock incurred three weeks of losses of 20% or more. Conversely, shares had only one week of gains of 20% or greater.

All told, this shift in probabilities indicates that the smart money is moving away from Occidental. If so, it won’t be long before OXY starts acting like a penny stock, if not looking like one. With the set-it-and-forget-it crowd gone, you’ll have to watch OXY constantly, lest it get out of hand.

Labor Market Reflects Additional Concerns

On the surface, the August jobs report gave market bulls much encouragement. In the face of extreme pessimism, the economy added 1.4 million jobs, while the unemployment rate dropped to 8.4%. During the aftermath of the 2008 financial crisis, the recovery took much longer. So, everything should be just fine, right?

Well, this is the part that gets tricky. We all know that government data like the jobs report is on a significant time delay. In contrast, the stock market is a real-time indicator of demand. So, the much-better-than-expected numbers from the jobs report should be a boon for OXY stock. More people working typically translates to more vehicles on the road: oil demand doesn’t care what kind of job you have.

But the fact that Occidental continues to accelerate its descent indicates that there are severe challenges within the company itself. Look, even the best oil firms in this environment is struggling. I’m just not sure adding more problems to your portfolio is worth the potential headaches.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) any positions in the securities mentioned in this article.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.