Nvidia (NASDAQ:NVDA) has been a beast, surging off the March lows and working its way to new all-time highs. Amid the run, NVDA stock even dethroned Intel (NASDAQ:INTC) in market capitalization.

Can it be sustained? That’s a loaded question and depends on what timeframe investors are working with. I do believe that the run in Nvidia can be sustained for the long term, if only because the company has done such a good job building out multiple secular growth units.

In any regard, the big run has many investors wondering if they should buy the dip or pass on this runaway train. Let’s look at a few pros and cons.

Nvidia Has Strong Growth But Is Expensive

- Pro: Nvidia boasts strong secular growth.

- Con: The stock is expensive.

The company has built out many solid growth units and is now harvesting the fruit from its labors. Whether that’s in the data center and cloud computing, artificial intelligence, gaming, self-driving cars or otherwise, the portfolio is impressive.

Analysts expect 44.5% revenue growth this year to $15.77 billion. Earnings are forecast to grow an even more impressive 57% to $9.09 per share. Next year, estimates call for 18.5% revenue growth and 21.6% earnings growth.

But consider how undervalued Nvidia was previously.

Current year estimates call for revenue of $15.77 billion. At the start of 2020, those estimates stood at about $10.8 billion. Estimates for next year started at $12.8 billion, before quickly climbing to $15.4 billion in February and now ultimately sitting north of $18 billion.

I wouldn’t be shocked to see Nvidia deliver revenue north of $20 billion next year. That said, we’re paying a premium for this growth.

NVDA stock trades at an eye-catching 57 times this year’s earnings estimates. That’s clearly a con, but it depends on one’s comfort level. While valuation matters, it’s not the only thing that matters.

Look at Shopify (NASDAQ:SHOP). Great company, expensive stock. Shares started the year off at a lofty valuation, trading at 30 times sales. Now Shopify is up 145% on the year and trades at 60 times sales.

I’m not sure on the depth of the current correction for NVDA stock. But I am confident that this stock will be higher than where it is now in three years and five years down the road. In an environment where growth is hard to come by, those showcasing growth will command a premium. And those boasting accelerating growth will command an even higher valuation.

Nvidia’s M&A

- Pro: Historically good at M&A; recent Arm deal is huge.

- Con: Nvidia faces regulatory risk.

Nvidia has shown a unique ability to make savvy M&A deals. That’s particularly impressive in the tech space, given the valuations that can be justified— as we just highlighted.

Nvidia scooped up Mellanox on the cheap, announcing the deal

in March 2019. The $6.9 billion deal closed in April 2020 and was immediately accretive to earnings, margins and cash flow. It was a perfect bolt-on acquisition.

However, Chinese regulators could have stopped the deal from going through. That was as the trade war between the U.S. and China was underway.

Now Nvidia has announced a much larger $40 billion deal with Arm Inc. Anyone who knows Arm’s technology knows what this could mean for Nvidia, even if it takes a while to close the deal.

The two are not competitors, so from a regulatory standpoint, that’s a huge positive for Nvidia. But pairing these two companies up would make Nvidia an unstoppable juggernaut — a name you buy, throw in the drawer and then take a look at in a decade or two.

Because of the strength it will have in this tie-up, it could draw some regulatory scrutiny. With China, it doesn’t help that the trade war — while on the back burner — isn’t really finalized. And how the U.S. is handling the TikTok situation really doesn’t help. China isn’t happy about that.

The pro here is simple in that Arm Inc. would be a huge landing for Nvidia. The con is that the deal doesn’t go through.

Relative Strength and Chasing the Stock

- Pro: Charts show relative strength and market leadership.

- Con: It has rallied far and fast, forcing investors to wait and risk missing out on more upside or chase now and risk a larger pullback.

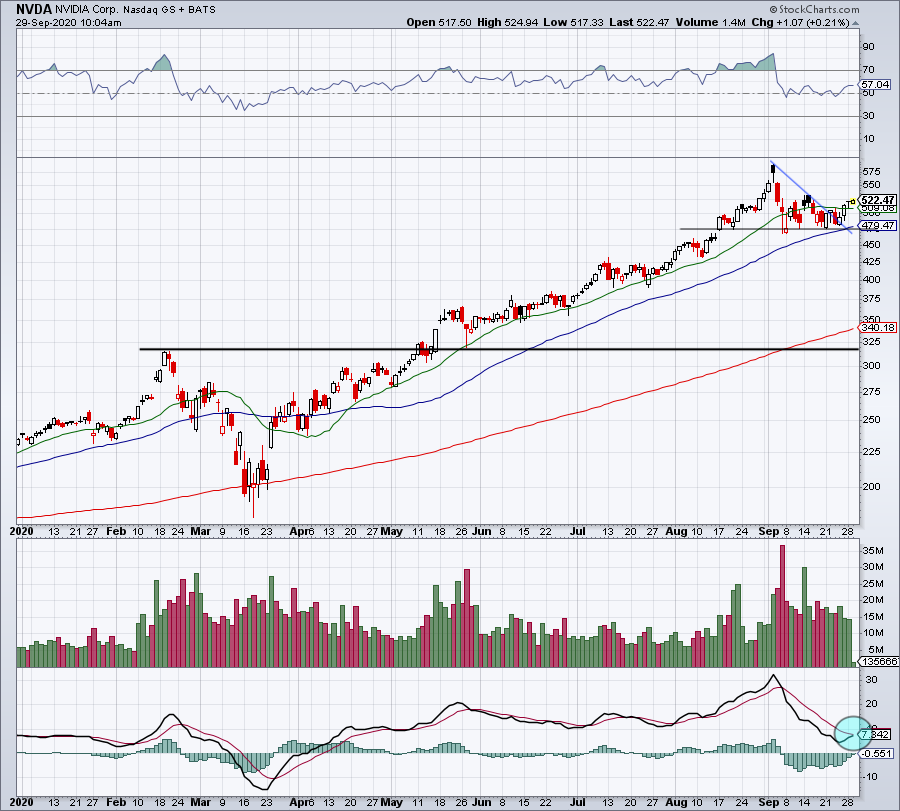

Right as the market peaked in February, NVDA stock was breaking out to new highs on strong earnings. However, it too got caught up in the selling. So while the rebound has been strong, it shouldn’t be a surprise. It’s why I called Nvidia a steal below $200 a share.

Shares ran from $180 to $589, more than tripling in a few months. Digesting those gains now, investors are trying to figure out if this dip is a buy or if a larger pullback will occur. With the drama unfolding in the political sphere and the novel coronavirus still impacting the economy, it’s impossible to discount a larger correction.

Click to Enlarge

That said, technically speaking, NVDA stock continues to trade really well. The 50-day moving average held as support as the stock carved out a nice base along $480.

For some investors, that may be enough to initiate a long position. For others, they may still prefer to wait for some downside. I personally would be comfortable nibbling on the dip, but only with the confidence that the stock will be higher several years from now.

However, should we get a nasty dip in Nvidia, be sure to buy it if you like this name.

On the date of publication, Bret Kenwell held a long position in NVDA.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell.