Since its disastrous 2018 redesign, Snap (NYSE:SNAP) has since staged an incredible comeback with its revamped Snapchat app. Snap stock is up 90% in the past year, reaching its all-time high on Thursday. The company eclipsed Twitter’s valuation for the first time since its 2017 IPO.

The great news, however, hides a worrying slowdown in user growth. As Snapchat’s popularity among U.S. teenagers starts to wane, investors should get out before its too late.

Because in the case of Snap, one Wall Street truism rings true: with teen-based fads, it’s “up like a rocket, down like a stick.”

SNAP Stock: Sustained by Teenage Whims

I started my investment career in analyzing consumer companies, and teen retailers were some of the hardest to predict.

Once-shining brands like Aeropostale saw its stock rocket from $3 in 2003 to almost $30 in 2010 as teenagers found “the next cool thing” to wear to school. The stock later tanked to $0 as teens abandoned the brand. There’s usually no apparent “reason” why teens might favor a brand in any given year.

Today, as a high-growth tech analyst, I see the same worrying signs about Snapchat. In 2020, over 40% of Snapchat users were below age 20, and users show the same fickle signs.

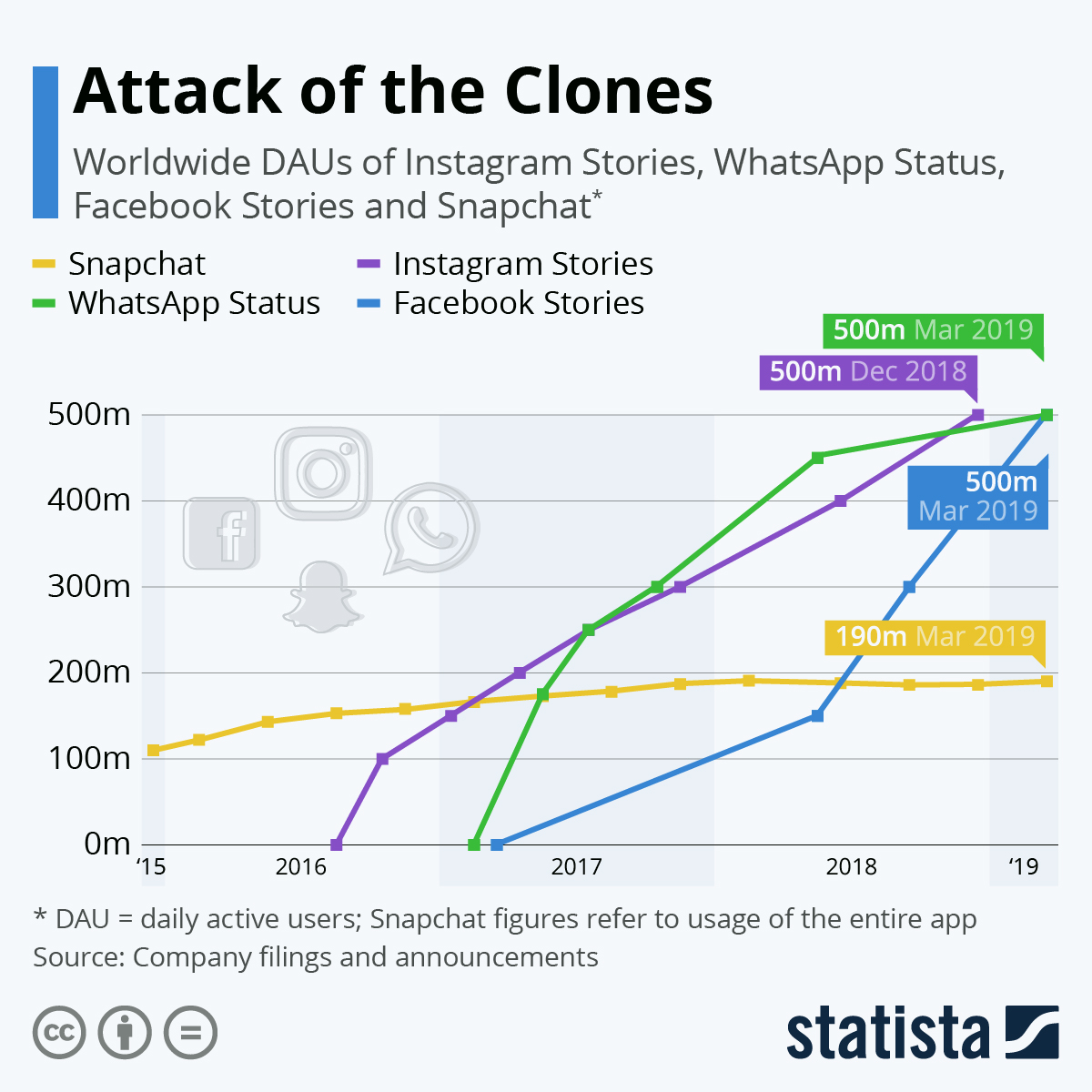

Looking back to Q2 and Q3 of 2018, SNAP users fell -2.6% as the company struggled with an app redesign. For a mature company, such a stumble might end up as a financial footnote. But for teen-focused SNAP, that minor loss turned the company on its head. Its stock tanked 47%, wiping out $9 billion of shareholder value.

Not much has changed in two years – SnapChat users still skew younger, keeping the company just as dependent on teen fads.

Slowing U.S. Growth

Today, SNAP’s overall user growth hides a slowing trend in North America, its most profitable market.

In the first half of 2020, Snapchat saw North American users grow by just 4.6%, a similar rate to far more mature Facebook (NASDAQ:FB). Twitter (NYSE:TWTR), a comparable company to Snap, saw a far faster 16% growth rate.

For Snapchat, growing at the same speed as Facebook is rather bad news. Facebook (and Twitter) already generate high profits – return on invested capital (ROIC) topped 27% in 2019. Snap, on the other hand, is still years from profitability. And slowing growth could mean the company may never make any money.

But don’t get lost in the numbers. To see why Snap is really in trouble, compare the company to its closest rival: TikTok.

Snap Losing Against TikTok

If you’re a parent, consider this: when was the last time you heard your kids talk about Snapchat? And what about TikTok?

For most people, TikTok would come top-of-mind. The social video-sharing app has grown like wildfire since its international launch in 2017. Today, the app counts 300 million global TikTok users and 500 million Chinese “Douyin” users. In Q2, the mobile app surpassed 2 billion installs, generating the most downloads of any app in a single quarter.

Snap, meanwhile, has fallen behind. The company has just 238 million global users and ranked #8 on the most-downloaded list.

Why Is SNAP Failing?

There’s nothing inherently wrong with the Snapchat app – it’s had the same general design since 2015, when “Discover” was added. But therein lies the problem: Snapchat has stagnated.

After the failed 2018 redesign, Snap’s management has shrunk away from making any significant changes. Start with advertising. In a bid to keep feeds uncluttered, the company puts in fewer ads, earning just $1.91 average revenue per user (ARPU). That’s less than a third of Facebook’s ARPU and a fifth of Twitter’s.

Next, consider the company’s stock options. To keep its engineers, the company paid $40 in stock options for every $100 it generated in 2019. Few tech companies come close to that level of generosity.

Finally, look at Snapchat’s usability. Rather than pursue significant changes, the company has instead turned its attention to minor enhancements, like building filters and lenses that can make you look younger or older.

Contrast that to Facebook’s innovation. Among other projects, in August, the social media giant launched Instagram Reels in hopes of competing with TikTok. The project might not succeed, but at least they’re experimenting until something does.

What’s Snap Stock Worth?

{kind=link}

When I see a high-growth tech company stop innovating, I head for the hills.

In an expected-case scenario, assume that Snapchat’s lack of innovation catches up to it.

Revenues could still grow from $1.7 billion in 2019 to $8.7 billion in 2029, but EBITDA margins might stall at 20%.

In that case, a 2-stage DCF model shows a $10.5 fair value, a -62% downside. That’s not a particularly strong investment case.

And even if Snap can regain its mojo, its high-priced shares will struggle to reward investors. If revenues grow to $11.2 billion in 2029 and margins rise to Twitter’s 28% EBITDA levels, a 2-stage DCF model still shows only an $18.7 fair value. That’s a -32% downside.

Of course, Snapchat could still get bought by a competitor – Amazon (NASDAQ:AMZN) has worked with Snap before and has plenty of cash for M&A. Microsoft (NASDAQ:MSFT) could be another contender – the tech giant lost its bid to purchase TikTok, so might make a surprise bid for Snap.

But without those lifelines, Snap looks dead in the water. Teens are indeed a fickle bunch – so don’t get caught at school wearing last year’s “cool.”

On the date of publication, Tom Yeung did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Tom Yeung, CFA, is a registered investment advisor on a mission to bring simplicity to the world of investing.