According to legend, Joseph P. Kennedy knew it was time to get out of the market when his shoeshine boy started to give him tips on high-flying equities. In a similar parallel, I believe that we’re getting to the point where Tesla (NASDAQ:TSLA) is not only overvalued but risks facing a sharp correction. Don’t get me wrong – although with anything Tesla stock, that’s a useless plea – I’m not here to hate on it.

First, I’m not alone in voicing concerns about TSLA. Late last month, Vitali Kalesnik, partner and head of research in Europe at Research Affiliates, stated that “While Tesla is a great company, Tesla stock has very strong signs of being overpriced.” As well, Motley Fool UK contributor Cliff D’Arcy warned that shares of the electric vehicle manufacturer appear to be the “mother of all bubbles.”

A Fundamental Debate

For the record, those aren’t my words. However, they speak to a small but growing contingent of voices that believe Tesla stock is out of whack with its fundamentals. That’s perhaps most apparent when you consider Tesla’s market capitalization. At nearly $669 billion, the EV maker absolutely dominates automotive heavyweights like Toyota (NYSE:TM) and General Motors (NYSE:GM), with $251.5 billion and $59.6 billion, respectively.

But the thing is, Toyota and GM are globally recognized brands with long histories and massive infrastructures. Further, the traditional internal combustion engine provides advantages in terms of everyday conveniences that you’re not going to get with an electric vehicle. (Remember, the world’s average infrastructure is nowhere near as fleshed out as it is here.)

While I’m going to avoid hyperbolic language that some critics have used – because that could be life-threatening – I do think it’s important for Tesla stock stakeholders to consider taking home some profits. Here are three reasons why.

Tesla Stock Must Contend with a Narrow Market

It’s no surprise to declare that Tesla caters toward the more affluent market. Though I realize that the Model 3, currently priced around $38,000, was heralded as making the company much more accessible, that’s still a lot of money for a car. Once you factor in taxes and registration, you could be talking about a $700 monthly car payment over five years.

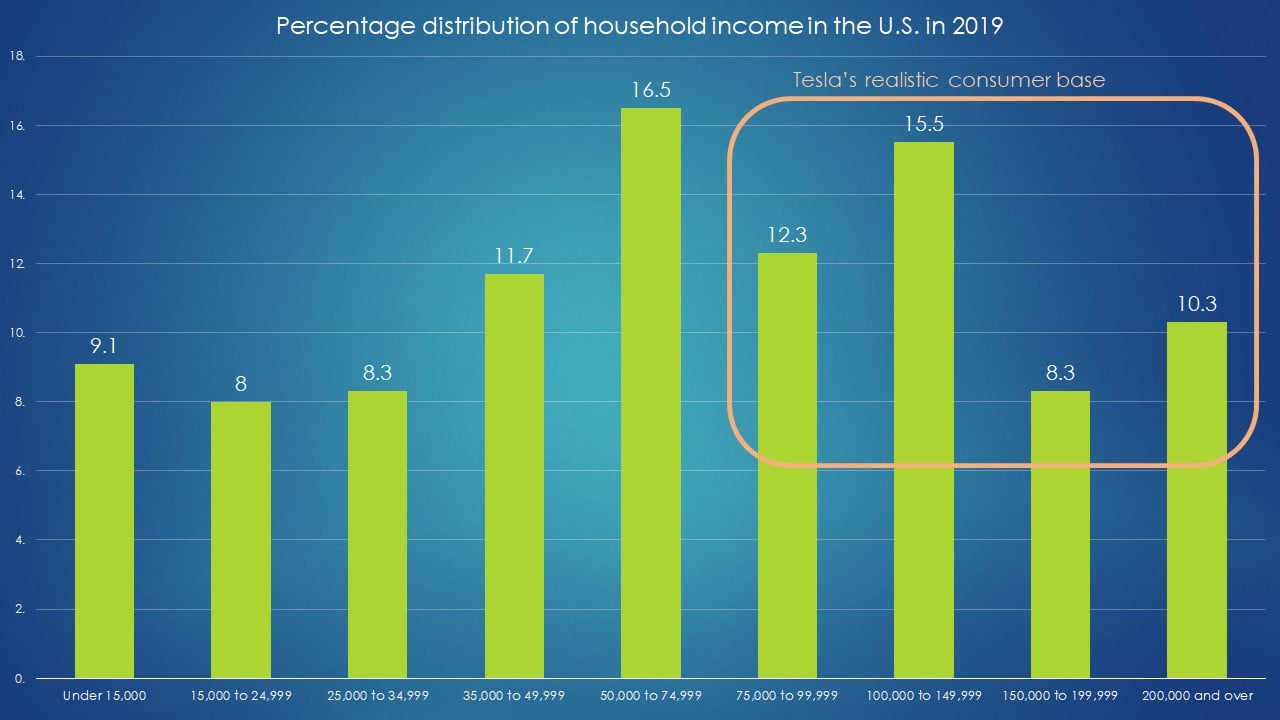

In my opinion, that’s not sustainable for what Tesla stock is presently valued at. According to data from the U.S. Census Bureau, the majority of American households (16.5%) make between $50,000 to $74,999, which is right inline with economy-model offerings from Toyota, GM, and Ford (NYSE:F). With the U.S. household count being approximately 123 million, this key demographic nominally turns out to be 20.3 million.

To be fair, 15.5% of households (the second largest income bracket) make between $100,000 to $149,999, which is largely Tesla’s target demo. Thus, you’re still talking about 19 million people, a very large addressable market.

Click to Enlarge

However, Toyota sold more than 2.7 million units in the North American region during its fiscal year 2020. Likely, this works out to be at least 10% of its target consumer base. On the other hand, Tesla delivered 499,550 vehicles in 2020. Even if we assume all those vehicles went to the U.S. market, that only represents 2.6% of Tesla’s target base.

And yet, the market cap of Tesla stock is more than the combined total of two Toyotas, GM, Ford, and Ferrari (NYSE:RACE). I’m sorry but that’s unreal!

Infrastructure Is Tesla’s Achilles’ Heel

One of the main criticisms against Tesla stock has been infrastructure. More than likely, a 100% transition to EVs will require upgrades to our electrical grid. Eventually, that will happen. But the California blackouts last year should tell you that we’ve got a long way to go before this becomes a reality.

Nevertheless, with President-elect Joe Biden’s push for a clean, renewable energy future, and with advancing technologies driving down costs while enhancing efficiencies, this green utopia will be possible at some point. But the issue becomes the infrastructural upgrades for the rest of the world. And that’s another dilemma facing Tesla stock at its present valuation.

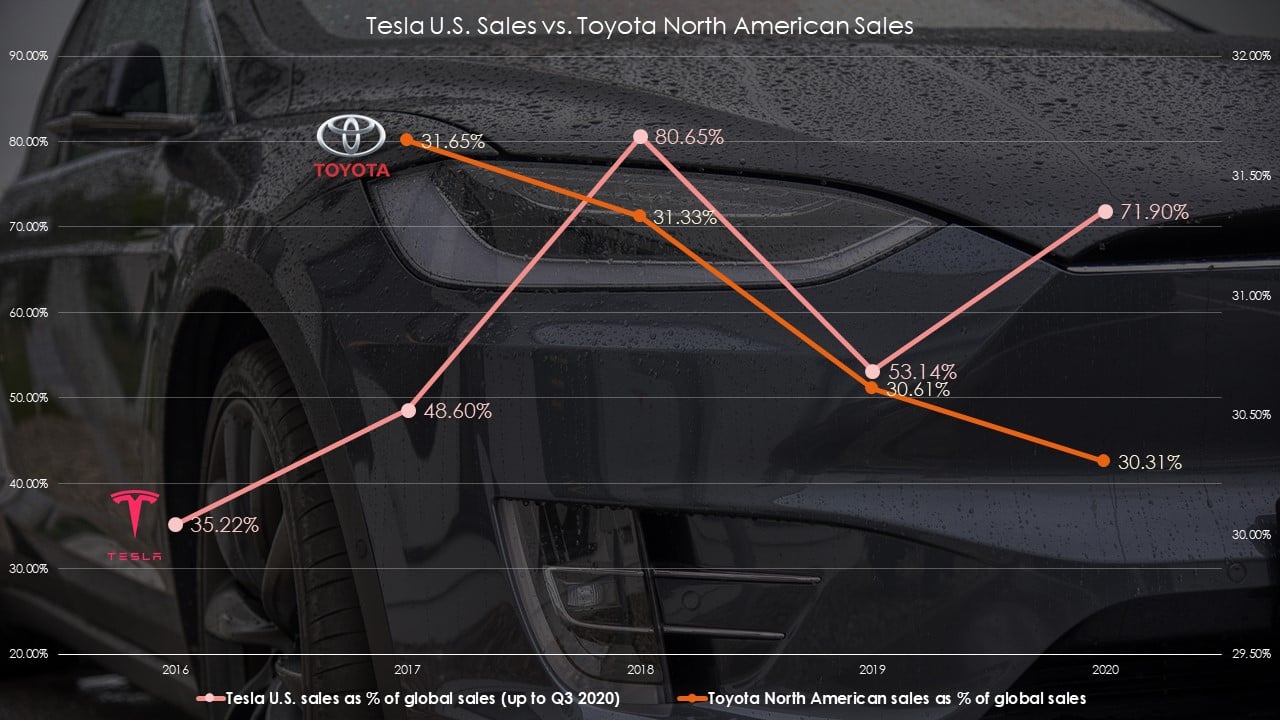

Here’s the deal – most Tesla EV unit sales have been directed toward the domestic market in recent years. Back in 2016 and 2017, Tesla’s U.S. sales represented approximately 43% of global sales. Between 2018 through the third quarter of 2020, U.S. sales accounted for nearly 67% of worldwide sales. On average since 2016, U.S. sales make up almost 63% of Tesla sales globally.

Click to Enlarge

Generally speaking, Tesla’s allocation toward the American market increased. Now, you can look at this both ways. On one hand, this shows you the power of Tesla’s brand among American drivers, which isn’t a bad gig. But on the other hand, this demonstrates that other countries’ infrastructures are lacking, making EVs inconvenient or impractical.

Interestingly, Toyota’s sales were relatively stable over the last four years. However, the automaker has been gaining traction in Asia (excluding Japan), Europe, Africa, and the Middle East. These markets will take time to adapt EV-specific infrastructure, which means combustion carmakers will dominate for years to come.

The way Tesla stock is priced, it’s assuming that these regions will go electric tomorrow.

TSLA Is Demographically Challenged

In my years working for and with major corporations, we’ve deliberately laid out plans to win key U.S. demographics, including Hispanics, women and people of color. Not once have I ever heard someone say, what can we do to win the whites?

Of course, that’s because whites are an “everyman” demo – generally, whatever whites like, others do as well. But marketers have to be careful in not appealing too much to white people as it limits product evangelization opportunities.

For instance, hockey is losing popularity and part of the reason could be its narrow appeal. According to a 2014 Nielsen report, NHL viewership was 92% white. That’s whiter than golf viewership, which was at 87%. Really, the only thing whiter was motor sports, with 94% white viewership.

On the other hand, you take something like soccer, which has tremendous growth potential due to its international pull. Sure enough, whites made up 65% of viewers, while Latinos made up a whopping 34%.

Well, Tesla stock finds itself in the same league as the NHL and golf in terms of demand. According to Hedges & Company, 87% of U.S. Tesla owners are white, 8% are Hispanic and 5% are other races/ethnicities.

Click to Enlarge

I’m not sure if I’ve ever seen anything like this. According to the National Golf Association, 72% of golfers are white. From a personal perspective, I could care less. But from a marketing standpoint, I believe catering too strongly to one demographic is a handicap when you’re trying to evangelize a new platform (EVs in this case) to the world.

For example, Hispanic consumers have a strong affinity toward Japanese automakers. That’s built over decades of reliable performance. So, when they come out with their EVs to compete seriously against Tesla, they’re going to carry a reputation advantage that appeals to almost everyone: Hispanics, whites, Asians, Blacks, women, you name it.

Before You Send That Email …

When something seems so perplexing, it’s helpful to have a lifeline that can help shed light on unseen biases. My lifeline is Will Ashworth, the cornerstone writer for InvestorPlace, and someone who helped me tremendously while I was getting my feet wet with the platform.

In an embarrassingly profane stream of consciousness, I spewed onto Will’s lap my unfiltered thoughts – Elon Musk style, ironically – about the possibly unsustainable rise of Tesla stock. He saw the humor in it (I guess it’s an acquired taste) but proceeded to give me much-needed insights and counterarguments.

First, Ashworth reminded me that despite the craftsmanship not being up to par with competitors in the price ranges which Tesla’s EVs compete, they’re right enough to keep selling more and more vehicles. Further, a combination of EV acceptance, lower battery costs and greater economies of scale will make Teslas within reach of most car buyers. And by deduction, make Tesla far less of a rich white man’s toy.

Second, the infrastructure that’s available to Tesla – the U.S., China, and western Europe – will provide plenty of fuel for Tesla stock. And folks in these regions will pay a healthy premium for the “in” thing: just look at the meteoric rise of home prices in desirable neighborhoods!

Finally, Tesla stock is an aspirational investment, meaning it shouldn’t be compared to the valuation of a legacy automaker. Eventually, TSLA may “grow” into its premium, as many growth companies do.

The Bottom Line on Tesla

These are fair points, so you want to be careful if you’re thinking that this is an easy short play. It’s not. However, I will say that aspirations eventually have to make business sense. For instance, Tesla’s non-battery battery day left many people perplexed.

Further, I disagree with the implications of the term “legacy.” Tesla sells its vehicles at a loss and is showing net profit largely due to selling carbon credits. What happens when instead of purchasing said credits, “legacy” automakers decide to make their own EVs (which they’re doing, by the way)? Yes, this adds to greater economies of scale to EVs through competition but that’s not necessarily helpful to Tesla stock exclusively.

As well, the valuation of Tesla stock implies that of a car company that caters to the masses (i.e. Toyota) but actually sells to the affluent (i.e. Ferrari) but without the latter category’s profitability. Bear in mind that Ferrari made a $94,000 profit, not loss, on each car in 2019.

And yes, Ferrari is a legacy brand. Its founder, Enzo Ferrari, was born in the, get this, 19th century. Yet I don’t see that being a detriment to Ferrari. If anything, it adds to its classic allure.

However, if you want to pay a premium for the aspirational value of Tesla stock, be my guest. But for me, I still think it’s out of touch with reality.

On the date of publication, Josh Enomoto held a long position in F stock.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare.