Switchback Energy Acquisition (NYSE:SBE) is a special purpose acquisition company (SPAC), a “blank check” shell corporation designed to take companies public without going through the rigors of a traditional IPO. In this environment, SBE stock should be a slam dunk. But it’s not.

Don’t get me wrong. Readers of these pages know that I am a sucker for electric vehicle (EV) stocks. However, the searing rally led by Tesla (NASDAQ:TSLA) is enough to make anyone’s head spin.

TSLA stock has risen over 20,000% since listing in 2010, and the momentum shows no signs of stopping. However, that must mean Switchback Energy is a buy.

Switchback’s target is ChargePoint, an electric vehicle infrastructure company founded in 2007.

After going public, the company is expected to have 305 million outstanding shares. Based on a share price of $37.98 per share, you have an $11.58 billion valuation.

By its own estimates, SBE expects $135 million in 2020 revenues, translating to a price-to-sales of 85.77 times. Even though shares are off their 52-week high of $49.48 a pop, I would still wait for shares to drop more before buying in.

Tailwinds Are Already Priced-In to SBE Stock

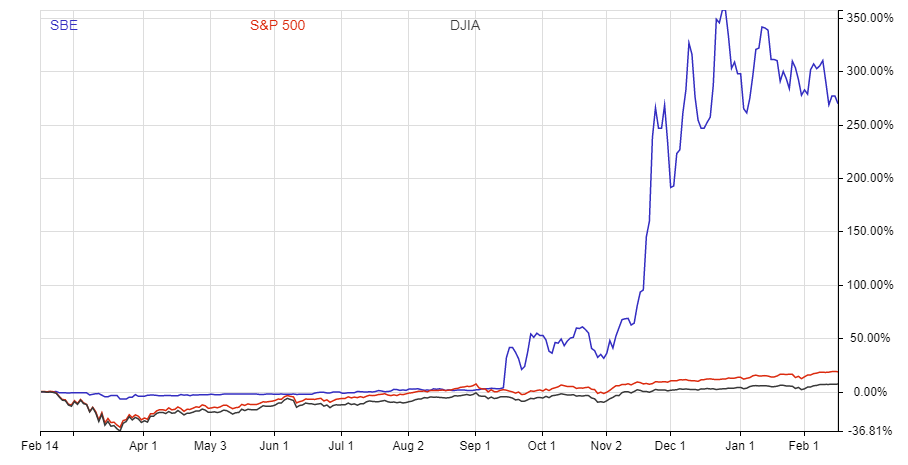

Click to Enlarge

The EV revolution is here in full force. Last year was a whirlwind. While some SPACs were hits, a large amount, like Nikola (NASDAQ:NKLA), were misses.

However, you have to treat each case on its merits, and that’s where SBE stock becomes an interesting play. ChargePoint claims to have “the world’s largest network of electric vehicle (EV) charging stations in North America and Europe.”

In September 2019, the company had 100,000 charging points under its belt. It plans to have 2.5 million charging points by 2025. That’s a conservative target.

According to at least one report

, “the global electric vehicle charging station market size is projected to reach 30,758 thousand units by 2027, from an estimated 2,115 thousand units in 2020, at a CAGR of 46.6%.”

Governments the world over are aggressive when it comes to the adoption of EVs. President Joe Biden has outlined a $2 trillion climate plan that has acted as a tailwind for renewable stocks, including SBE.

However, all of this hoopla has led to an astronomical valuation. In a recent presentation, the company projected revenues of $2.07 billion by 2026. If you take that number, you get a 2026 P/S ratio at almost six times.

Now, six times is a ratio you can afford to live with for a buy-and-hold investment, not the 85.77 times it’s trading now.

Do Not Be Around When the Bubble Bursts

The top question on everyone’s mind is when the EV bubble will burst, if ever. For several investors, it’s still jarring that Tesla is the biggest automaker in terms of market cap. And it’s not just Tesla. Chinese EV maker Nio (NYSE:NIO), a relative newcomer, is now worth more than General Motors (NYSE:GM), despite selling a fraction of the cars.

So let there be no mistake. We are in the middle of a bubble. However, considering that production continues to ramp up and sales targets keep getting hit, expect the positive momentum to continue.

It will have a knock-on effect on SBE stock as well, along with other EV charging plays.

However, it goes without saying that fundamentals and market cap will soon catch up to each other. Maybe it’s not the apocalyptical situation we saw with the dot com bubble. Instead, the air will probably let out gradually from the balloon.

It is not a matter of “if” but “when” that happens, and before that, you should only be invested in sure-shot winners in the space.

Even If You Want to Buy, It’s Best to Wait

Right now, arguing against any EV play seems futile. Retail traders have made excellent returns through trading on these risky speculative bets. Nonetheless, even if you want to engage in short-term trading, there is little to no upside left on this stock. You can easily buy into SBE once shares cool off in a few weeks.

If you believe in the company’s long-term vision, wait for a few quarterly reports before investing. EVs are here to stay, and the charging infrastructure at the heart of SBE is gold. However, there will be many peaks and valleys until the company reaches that 2.5 million charging station mark.

In the short term, expect further incremental gains. However, once insider lockup agreements expire, typically between 90 days and 180 days of merger close, you will see the stock price plunge.

On the date of publication, Faizan Farooque did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Faizan Farooque is a contributing author for InvestorPlace.com and numerous other financial sites. Faizan has several years of experience analyzing the stock market and was a former data journalist at S&P Global Market Intelligence. His passion is to help the average investor make more informed decisions regarding their portfolio.