Warren Buffet’s famous quote “Cash Is King” emphasizes the importance of a company’s value. The argument is that strong cash flows both increase a company’s growth prospects and provide a higher intrinsic value to the stock. In today’s article, we’re covering companies with outstanding cash flow. I’ve selected a mix of stocks to buy that provide prospects for dividends, deep value, and growth.

The market’s getting rid of a bit of froth, and investors must opt for high-quality stocks moving forward. I believe that good earnings make good companies, and good companies make good stocks.

Let’s get into my seven stocks to buy, and I hope you all enjoy the read!

- International Business Machines (NYSE:IBM)

- Pool Corporation (NASDAQ:POOL)

- Target Corporation (NYSE:TGT)

- Deere & Company (NYSE:DE)

- Crocs, Inc. (NASDAQ:CROX)

- ROKU, Inc. (NASDAQ:ROKU)

- Hibbett, Inc. (NASDAQ:HIBB)

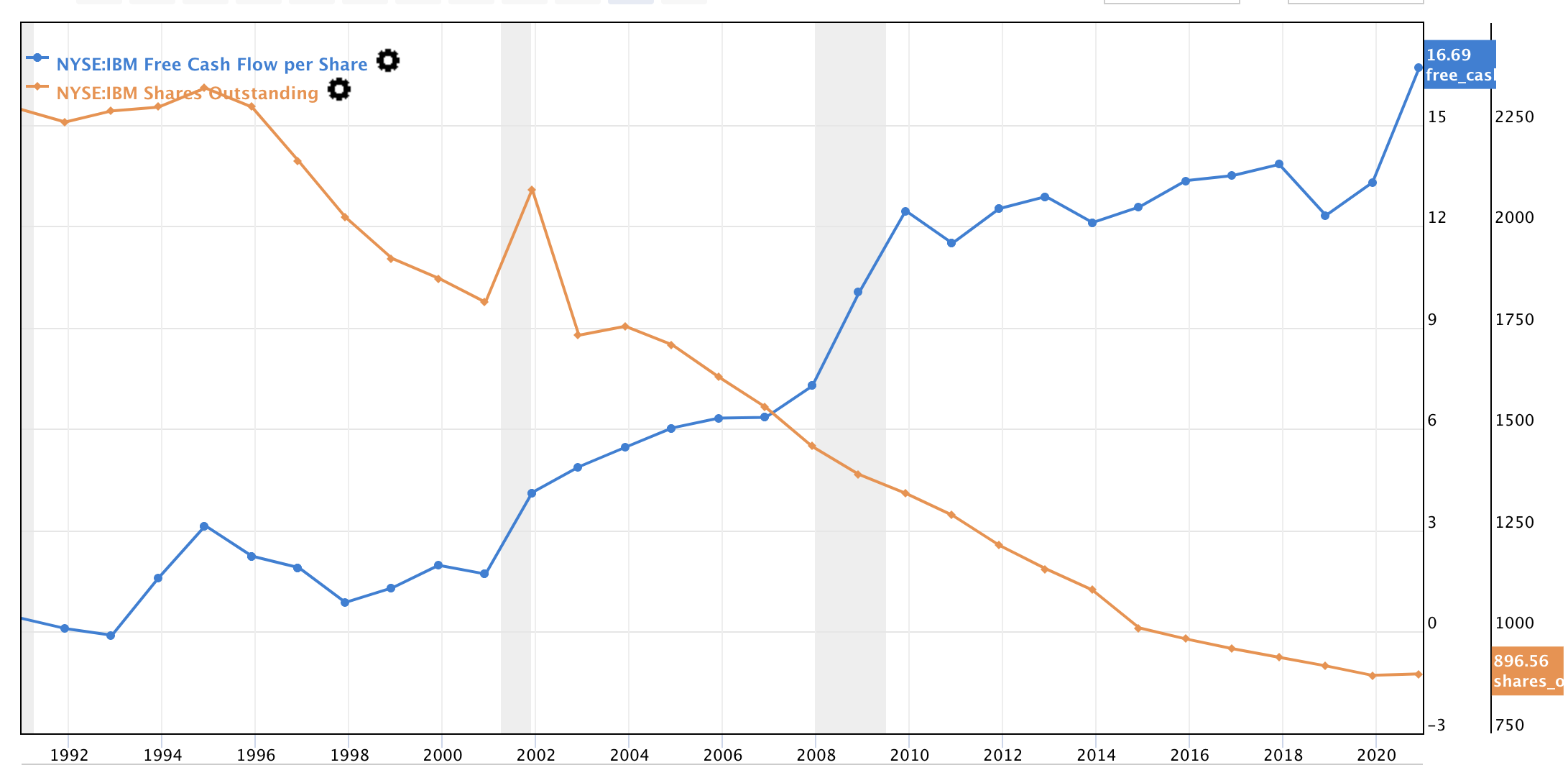

Stocks to Buy: International Business Machines (IBM)

IBM has done well in increasing its operating efficiency through both productivity gains and growth acquisitions. The company is well positioned to benefit from cloud uptake, and the acquisition of Red Hat will assist with synergies in the hybrid cloud market. A quality patent portfolio and the company’s blockchain, security and other digital transformation products provide prospects for sustainability.

Due to strong cash flows, IBM can be both a dividend and a value play at the moment. A five-year average free cash flow yield of 10.3% beats the sector median of 1.1%. IBM has predominantly used its cash to repurchase shares as well as pay attractive dividends. IBM’s dividend yields 4.5%, and the company’s paying out 60% of its net income.

Based on a multiples valuation, the stock is set for tremendous upside. The forward P/E multiple implies a price target of $283.55, while the intrinsic value based on free cash flows suggests a $212.77 price target. Wall Street has a more modest outlook, with Bank of America being the latest to release a report with a $175 12-month price target.

In my opinion, big banking analysts are often behind the curve and will probably revise their targets upward as the company continues to produce strong EPS.

Pool Corporation (POOL)

Click to Enlarge

Being the world’s leading distributor of pool equipment says a lot about the efficiency of the company. Pool Corp has expanded well the past year, with 57% year-over-year growth in overall sales.

In addition, The company has also acquired additional distribution centers in New York, New Jersey, Texas and Florida in the past year.

Pool’s free cash flow of $284.9 million is at its highest since 2009. Share repurchases accompanied by strong operating cash flows have resulted in an increase in free cash flow yield.

Goldman Sachs set a $535 price target on the stock last month. Pool Corp’s residual to investors has consistently increased over the years, and in May, it decided to increase its quarterly dividend by 38%, subsequently pushing the forward yield up to 0.74%. Pool is an underfollowed stock with a high-quality business model.

I think factors such as the company’s increasing cash flows and profitability, the low number of shares outstanding, and repurchase programs make it cheap at the moment.

Stocks to Buy: Target Corporation (TGT)

Earlier this month, Target increased its quarterly dividend by an astronomical rate of 32.4%. Target’s cash from operations has increased nearly 50% year over year to $10.5 billion. Aspects such as an omnichannel strategy, same-day delivery, and brand creation have served the company well of late. The company’s Q1 comparable sales for in-store purchases were up 18% while digitally-oriented rose 50.2%, implying that they’ve balanced in-store and online shopping well.

A free cash flow yield of 8.7% exceeds the industry average of 3.5%. Target’s been repurchasing shares aggressively over recent years, which has maximized shareholder value.

The stock is undervalued according to relative valuation metrics. I think the stock’s cheap due to the current share buyback program and EPS consensus being positive. I also believe that dividend investors can’t go wrong with a stock that’s been paying out a dividend for 53 consecutive years at a five-year growth rate of 3.96%.

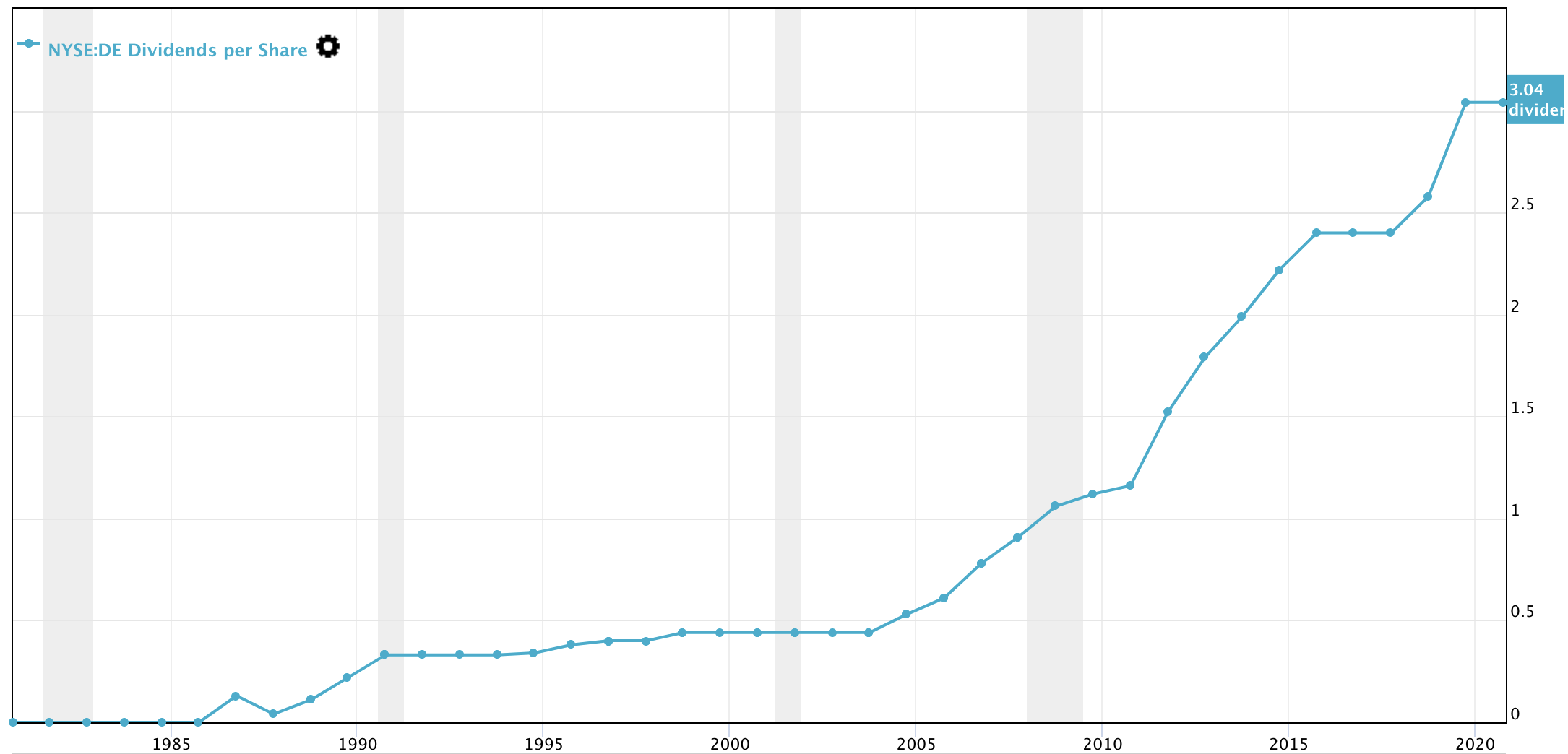

Deere & Company (DE)

Click to Enlarge

Despite a recent pullback, I still believe that Deere stock is highly inexpensive. Increased productivity in the farming and construction industries will most probably lead to higher profits for Deere. From a long-term perspective, further market share is anticipated, since the company is growing rapidly in precision farming and tapping into underserved markets.

In last quarter’s earnings report, Deere’s unlevered free cash flow nearly doubled year over year. A 5.6% free cash flow yield along with a forward dividend growth rate of 1.01% adds to my optimism.

According to Evercore, the stock could reach $455 per share within the next 12 months. Dividends have increased at a five-year rate of 6.7%.

Dividend investors should pay attention, as net income is at its highest point in seven years; I expect dividend growth to persist.

Stocks to Buy: Crocs (CROX)

It has not just been Crocs products that have returned to fashion of late — the stock has as well. Crocs stock has beaten the S&P 500 by nearly six times over the past year.

The company’s growth in both online and in-stores sales has surged of late, with its latest earnings release reporting a 64% year-over-year growth rate in revenue. Its operating income has increased by 22.83% since 2015 due to increases in asset and inventory management efficiency.

Crocs doesn’t pay a dividend, but it holds significant value and growth prospects. The free cash flow has increased by $109.30 million year-over-year. Piper Sandler recently placed a $140 price target on the stock.

Roku (ROKU)

Roku’s performance has been labeled a lockdown anomaly by many, but I believe in its longevity.

Roku’s user growth had increased gradually prior to the pandemic, and the lockdown period was just what the stock needed to really get going. Deutsche Bank sees secular gains ahead for ROKU due to its market positioning and predicted sustainability in online streaming.

ROKU turned in a net profit during the last quarter worth $113.4 million.

If the company looks for acquisitions for growth purposes with its residual, it will continue to produce impressive cash flows. The stock returns will be bound to ROKU’s ability to maintain market share and the synergies it adds to its arsenal.

Stocks to Buy: Hibbett (HIBB)

The last stock I’m covering today is Hibbett. Hibbett is a very underrated company and stock, in my opinion. The sports apparel retailer has targeted underserved locations since 1945. The company has managed to open more than a thousand stores across the United States in high-growth areas.

Central to the company’s recent growth has been e-commerce development, selective store expansion, and its customer loyalty programs.

Hibbett’s has a 5-year free cash flow yield of 16.5%. The company’s managed to increase its cash by an impressive $164.6 million in the past quarter.

Click to Enlarge

The company is tremendously shareholder-driven with constant share repurchases since 2005. Hibbett announced in May that it would increase its share repurchase program by $500 million; the extension is authorized until February 2025.

Hibbett’s already gained north of 300% over the past year, but I don’t think that investors should cash in their profits just yet. The stock’s still trading well below its peers on key multiples. The stock’s P/E ratio is still below its five-year average, which is an indicator of relative value.

Hibbett is still a buy with a $110 price target, according to Bank of America.

All of the stocks in this article hold value based on cash flow and should perform well under efficient market circumstances. I’d recommend that investors diversify a portfolio by adding at least a few cash flow-driven stocks to their major holdings. If you have any questions regarding my picks, feel free to contact me directly!

On the date of publication, Steve Booyens was long POOL and HIBB. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Steve Booyens co-founded Pearl Gray Equity and Research in 2020 and has been responsible for equity research and PR ever since. Before founding the firm, Steve spent time working in various finance roles in London and South Africa, and his articles are published on various reputable web pages such as Seeking Alpha, Benzinga, Gurufocus, and Yahoo Finance. Steve’s content for InvestorPlace includes stock recommendations, with occasional articles on crowdfunding, cryptocurrency, and ESG.