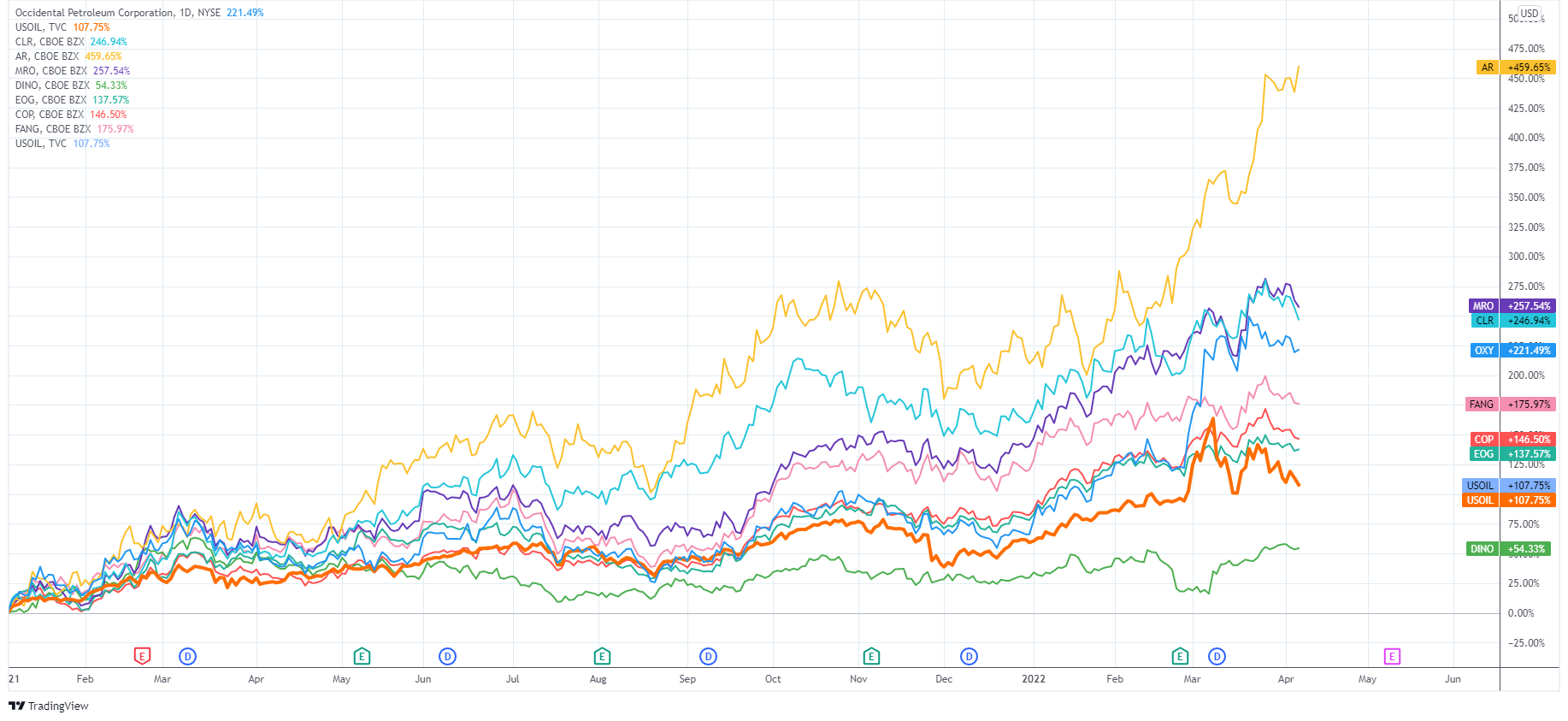

- Occidental Petroleum (OXY) — Strengthening free cash flow and attractive multiples make the Permian producer a buy.

- Continental Resources (CLR) — Despite a vigorous stock performance there is still space for appreciation, as CLR’s profitability enhances in 2022.

- Marathon Oil (MRO) — The oil stock has a strong execution and allocated a large portion of free cash flow to shareholders.

- HF Sinclair (DINO) — With refining margins expected to expand, this oil refiner is a good investment for steady gains.

- EOG Resources (EOG) — A healthy balance sheet and cheap valuation metrics compared to its growth prospects.

- ConocoPhilips (COP) — The oil stock has a prosperous track record and comfortable profit margins.

- Diamondback Energy (FANG) — With high net margins and an elevated average target price, the independent oil firm is set for additional bullishness.

Crude oil prices increased significantly in the past month in response to mounting anticipations that sanctions to penalize Russia over the invasion of Ukraine will leave less crude to fill an increasing oil demand.

After reaching a high of $123.7 per barrel in March, WTI crude oil prices retreated near the psychological threshold of $100 per barrel. In the meantime, the United States Oil Fund LP (NYSEARCA:USO) gained 37.6% year-to-date to $74.8 per share, outperforming the broader equity market.

Click to Enlarge

Crude oil stocks are set to continue to benefit from high prices and rising tensions between Western countries and Russia. However, oil weakness is not off of the table, after the International Energy Agency (IEA) announced the release of 120 million barrels from strategic reserves to curb oil prices. Yet, a growing number of rumors suggest that European countries might soon decide to ban Russian oil and gas imports, a significant bullish catalyst for crude prices.

With that being said, here is a selection of crude oil stock to buy in anticipation of a bubbly second quarter:

| OXY | Occidental Petroleum | $57.91 |

| CLR | Continental Resources | $62.02 |

| MRO | Marathon Oil | $25.38 |

| DINO | HF Sinclair | $38.12 |

| EOG | EOG Resources | $122.38 |

| COP | ConocoPhilips | $98.46 |

| FANG | Diamondback Energy | $135.49 |

Oil Stocks: Occidental Petroleum (OXY)

Occidental Petroleum (NYSE:OXY) stock is one of the world’s largest oil groups in the U.S. and a leading player in the Permian Basin, one of the most prolific oil basins in the world. Occidental produced 1,289 million barrels of oil equivalent per day (Mboepd) in 2021 and its stock surged over 100% year-to-date to $57.91 per share.

Crude oil firmness benefitted broadly to OXY and should continue to do so if oil prices remain above the $100 per barrel threshold. Net sales ballooned 61.8% in 2021 to $26.31 per share and the consensus expects another robust advance this year, up 19.5% year-on-year to $31.44 billion. After a strong 2021, OXY’s free cash flow (FCF) is estimated to jump by a whopping 50.6% in 2022 to $11.12 billion, providing a strong bullish catalyst.

Besides, OXY is committed to strengthening its balance sheet and returning capital to shareholders. In February, Occidental boosted its annual dividend distribution from 4 cents per share to 52 cents per share, providing an expected yield in 2022 of 0.74% compared to 0.14% last year.

With these positive developments, the oil stock has relatively low multiples compared to its historic mean, posting 2022e Enterprise Value (EV) on earnings before interest, taxes, depreciation, and amortization (EBITDA) of only 3.83x and a forward price to book (P/B) ratio of 8.51x. Besides, Wall Street analysts give the stock an average price target of $64.75 per share, an upside of 10.74% from today’s price.

Continental Resources (CLR)

Continental Resources (NYSE:CLR) is an oil and gas company with operations in the North, South, and East regions of the U.S, with a total throughput of 329.6 Mboepd in 2021. CLR shares jumped 39% to $62.02 per share since the beginning of the year, slightly underperforming oil stocks. Nevertheless, the oil and gas specialist gained 246.94% since 2021, posting one of the sturdiest advances in the oil industry.

The strong fundamentals are mainly behind this performance. After jumping 121.2% to $5.71 billion in 2021, CLR’s revenues are expected to maintain a rapid growth this year, up 37.2% year-on-year to $7.93 billion. On the other side, net profit should expand even fast, posting a 2022 increase of 89.9% to $3.15 billion, corresponding to a strong profit margin of 37.2%.

Besides, Continental deleveraged and is expected to continue to deleverage rapidly in 2022. Net debt was established at $26.8 billion at the end of 2021 and it is projected to dip 47.3% to $14.1 billion this year. The leverage ratio of the oil stock is expected to decrease to just 0.76x in 2022, which is constructive for CLR’s financials and for the appreciation of CLR shares, given the Federal Reserve’s tightening monetary stance.

Despite CLR’s stock surging in the past year, the oil company exchanges at a low valuation metric at 3.7x 2022e EV/EBITDA and a forward P/E of 6.71x.

Oil Stocks: Marathon Oil (MRO)

Marathon Oil (NYSE:MRO) specializes in the exploration and production of oil and natural gas with over 172,000 barrels of oil and gas condensate sold per day in 2021. MRO stock outperformed its peers lately, posting a 55% increase to $25.38 per share year-to-date.

The oil and gas stock beat earnings and revenue guidance in the three quarters and distributed over 70% of fourth-quarter FCF to shareholders, somewhat explaining the rapid advance of the stock year-to-date.

Besides, the company has a constructive outlook. Revenues are projected to expand 23.5% to $6.75 billion in 2022, whereas FCF generation is estimated to top at $3.45 billion, up 59.4% year-on-year.

With the robust prospects, MRO exchanges at attractive metrics, namely at 3.85x forward EV/EBITDA and 6.88x P/E.

HF Sinclair (DINO)

HF Sinclair (NYSE:DINO), formerly HollyFrontier, is an independent energy and refining company. The company converts discounted, heavy and sour crudes into gasoline, diesel, and other high-value refined products.

Since the beginning of the year, DINO stock advanced moderately, up 16% to $38.12 per share, largely lagging the performance of crude oil stocks. Despite that, DINO has grown steadily over the past few years and net sales are projected to advance 51.8% to $27.92 billion in 2022. On the other side, net income should lift 40.8% to $786 million, representing a low margin of only 2.81% for the year.

Nevertheless, refining margins are expected to balloon, following U.S. and British ban on all Russian oil imports. Besides, HF Sinclair is well-capitalized with an expected net debt of only $2.84 billion, equivalent to a leverage ratio of $1.45x.

In addition, valuation metrics remain attractive for this stable refining firm. The company has a 2022e EV/EBITDA of 5.88x, a forward P/E of 9.71x, and has an expected dividend yield of 2.56% for this year.

Oil Stocks: EOG Resources (EOG)

EOG Resources (NYSE:EOG) specialized in crude oil and natural gas exploration and production. The company had an oil exposure of 71.8% and an overall throughput of 828.9 Mboepd in 2021. EOG slightly underperformed the oil complex year-to-date, advancing 38% to $122.38 per share, despite record earnings and free cash flow last year.

Nevertheless, FCF growth is projected to advance strongly, up 30.2% to $6.99 billion. Besides, EOG Resources has one of the fittest balance sheets in the industry, with a net cash position of $100m at the end of Q4 2021.

The oil specialist has increased capital returns to shareholders significantly in the past quarters. EOG recently announced a special dividend of $1 per share, delivering an expected dividend yield in 2022 of 3.48%. In terms of valuation, EOG trades in line with other oil stocks, trading at 4.45x 2022e EV/EBITDA and at 8.78x P/E.

ConocoPhilips (COP)

ConocoPhilips (NYSE:COP) produces, transports, and markets crude oil, bitumen, natural gas, and liquefied natural gas (LNG) worldwide, with a total production of 1,567 Mboepd in 2021. This oil stock has performed in line with the sector over the year, surging 36% to $98.46 per share.

Yet, ConocoPhilips has a strong track record, beating analysts’ earnings and revenue estimated in the last four quarters. Top-line growth is estimated to climb robustly this year, up 29.5% to $62.6 billion, even if revenues skyrocketed last year, advancing 151.1% to $48.3 billion. Net profits are however projected to expand even faster this year, up 65.6% to $13.3 billion, representing a high-profit margin of 21.4%.

COP’s net debt remains manageable. With net debt of $14.4b at the end of 2021, the oil stock has a low leverage ratio of 0.67x. In terms of valuation metrics, COP exchanges with a slight premium compared to oil stocks at 5.01x forward EV/EBITDA and 8.98x 2022e P/E. Besides, the consensus of analysts is bullish on COP’s equity story, offering an average target price of $116.50 per share, corresponding to an upside of 18.3%.

Diamondback Energy (FANG)

Diamondback Energy (NASDAQ:FANG) is another independent U.S. oil and gas exploration and production company, with an exposure of 87.4% to crude and an average production of 223.3 million barrels of oil per day. FANG stock underperformed crude oil stocks year-to-date, posting an advance of 25% to $135.49 per share.

Diamondback’s profitability is forecasted to improve significantly this year. After bouncing 148.3% to $2.18 billion in 2021, net profits are estimated to lift 83.8% to $4.01 billion, offering a high-profit margin of 49.9% per year.

In terms of the balance sheet, FANG’s stock is expected to reduce 47.2% net debt in 2022 to $3.23 billion, offering a leverage ratio of just 0.51x. With these strong financials, Diamondback is projected to produce a yield of 1.83% in 2022 and the crude stock remains cheap, trading at a forward EV/EBITDA of just 4.34x and a 2022e P/E of 6.1x. In addition, the average target price provided by the consensus stands at $169.05 per share, an upside of 23.44% from today’s price.

On the date of publication, Cristian Docan did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.