- Clover Health (CLOV) stock discussions are binary.

- The pro argument has a billionaire’s endorsement.

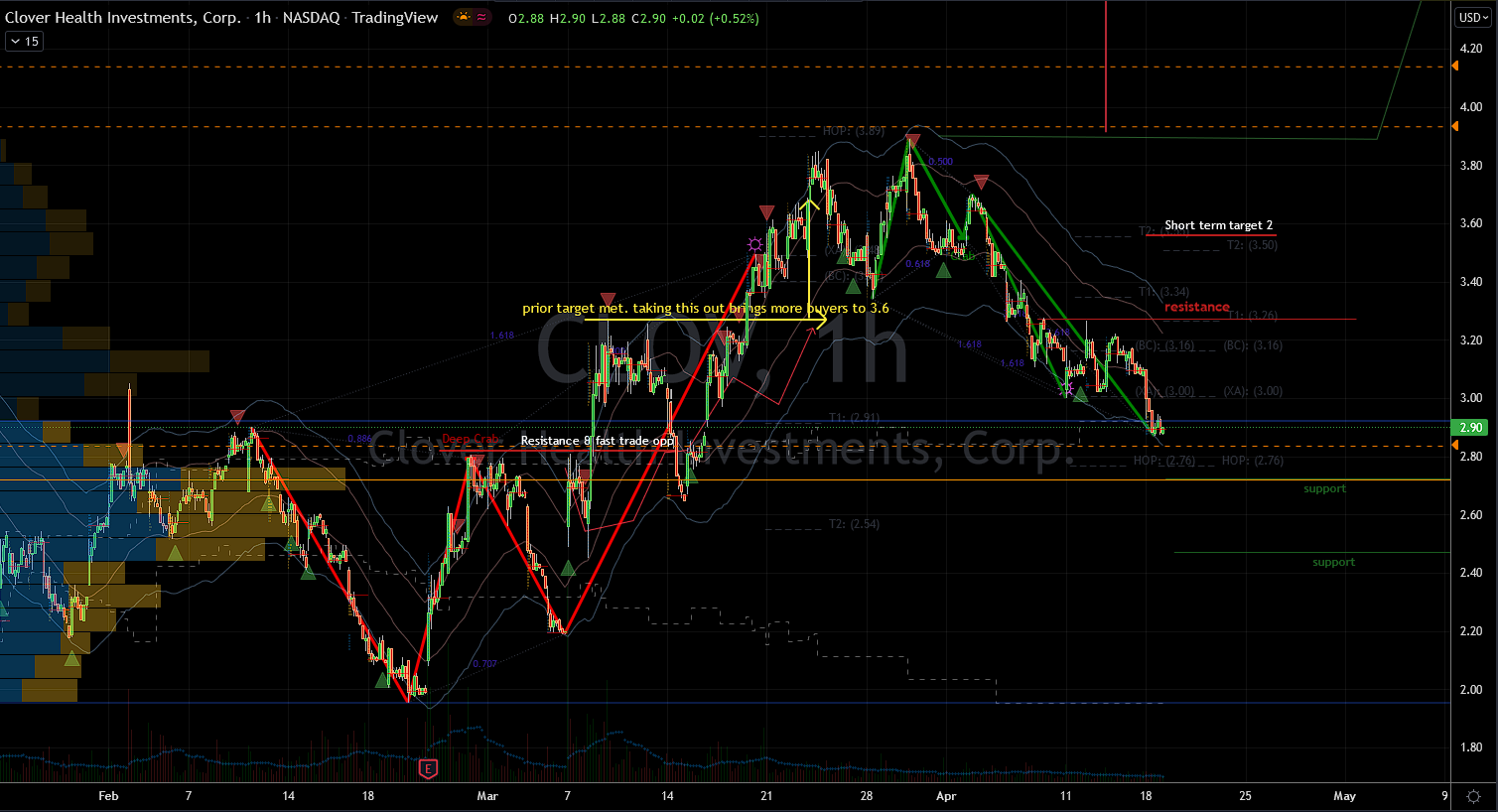

- CLOV stock showed relative strength when markets were weakest.

Here’s the punchline first, that Clover Health (NYSE:CLOV) stock will prove itself worthy in the end. Meanwhile, investors are still uneasy about the state of the global economy. This is in spite of having an extremely robust U.S. economy. Mainly this is possible from the trillions that the government poured into it to restart affairs post pandemic lockdowns. Therefore, the high volatility now is not so much because of the corporate results, those are still breaking records. However, the worries stem from external factors like a war in the Ukraine and Federal Reserve rate hikes.

Today’s topic of discussion is almost always controversial. So it’s not a surprise that CLOV stock journey has been turbulent. Perhaps the problem was the way it came to market as a special purpose acquisition company (SPAC). Those carry a stigma that it will have to bare for a while. In due time, the company’s performance may erase its effects but not just yet. A comforting aspect of this one is that it has a decent pedigree.

Famous billionaire investor Chamath Palihapitiya brought Clover to market. He has needed to publicly defended it often. Late last year he even divested a few other losers to add to his favorites including CLOV. Sadly, this did not abate the selling in the stock, as it fell to $2 per share in February. In all fairness, the whole market crashed then on the news of Russia’s invasion of Ukraine.

The opinions over CLOV’s business are binary. Offsetting the billionaire backing are hordes of critics who basically mock it. I contend that between it being a fraud or a billion dollar business, I side with the bulls. Eventually, results will be the evidence we need to tell a positive story with a shaky start. Not everyone hates Clover health. Recently the stock soared on news that former first daughter Chelsea Clinton had invested in it. The news provided strong lift in the bid for CLOV.

However, it is important to note that it had already showed relative strength late February. While markets were weakest on Feb. 24, CLOV stock was the first to turn green on my screen. It basically marked the very sharp “v” bottom that week. This goes to show you how silly the overall Wall Street mantra has become. According to Yahoo Finance, Clover has an annual revenue run rate of $1.5 billion. This of course doesn’t guarantee a rally. But it does reinforce the legitimacy of the business.

| CLOV | Clover Health | $2.91 |

CLOV Stock Upside Outweighs the Risk in the Long Run

Click to Enlarge

The fact that it fell to $2 per share makes the upside opportunity likely larger than the downside risk. In the short term, it will not be able to rally alone, so it will need healthy markets. Investors will need to show better resolve on Wall Street. Monday started out shaky but ended on a good note, the bulls were able to stave off a bad day. Moreover the

CBOE Volatility Index lost ground after showing strength earlier. But we are still teetering going into an earnings season starting with Netflix (NASDAQ:NFLX) today. It stock reaction will also most other stocks like Meta (NASDAQ:FB), Apple (NASDAQ:AAPL) and Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL).

The overall extrinsic risks have not changed in months. In reality they are likely to remain a stalemate without expanding aggravation. Investors will slowly learn to live with them. Theories aside, the charts suggest that the CLOV stock bulls have help. The mid March support zone looks dependable barring new headlines. With footing in place, the bulls can tackle the resistance levels with relative confidence.

Technically, there are chart patterns that target $3.3 per share, but with resistances in the way. Mainly there should be sellers lurking approaching $3.1 per share. In the long run, the easiest course of action is to follow in Mr. Palihapitiya’s footsteps. Investors could do well by taking a partial position to start, then appropriately add along the way. This approach diversifies the need to be surgical picking the perfect spot to buy.

Regardless of on which side of the Clover Health argument you are, I suggest you keep medium conviction at best. There are so many extrinsic factors influencing the individual stocks that we must remain humble with all expectations.

On Penny Stocks and Low-Volume Stocks: With only the rarest exceptions, InvestorPlace does not publish commentary about companies that have a market cap of less than $100 million or trade less than 100,000 shares each day. That’s because these “penny stocks” are frequently the playground for scam artists and market manipulators. If we ever do publish commentary on a low-volume stock that may be affected by our commentary, we demand that InvestorPlace.com’s writers disclose this fact and warn readers of the risks.

Read More: Penny Stocks — How to Profit Without Getting Scammed

On the date of publication, Nicolas Chahine did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.