- Lucid Motors (LCID) tops views but fails to impress investors.

- Production forecasts remain challenging to trust and LCID stock remains a riskier investment.

- Investors should smartly steer clear of LCID stock.

April was a car wreck for Lucid Motors (NASDAQ:LCID) with shares tumbling 28%. This month the stock hasn’t caught a break either. And let’s just say 2022 hasn’t been anything to celebrate with LCID stock spiraling lower by 58%. And despite all that, shares still aren’t a buy.

If misery loves company, there’s plenty in the world of electric vehicles (EVs) for LCID stock bulls to commensurate with. Some of the damage is worse as Rivian Automotive’s (NASDAQ:RIVN) 78% bear market can attest. And in other spots the fallout is slighter but still painful. Tesla’s (NASDAQ:TSLA) shareholders who are down 24% year-to-date (YTD) can vouch for that.

It’s not a secret rampant inflation, at-risk consumers, supply chain disruptions, unpleasant and concerning rate hikes have wreaked havoc on EV stocks. And while Lucid did manage a headline quarterly beat this past week, a review of other key evidence, off and on the price chart, warns that buyers in LCID stock remain at higher and avoidable market risk.

| LCID | Lucid Motors | $15.38 |

Bulls’ Issues With LCID Stock

In spite of smashing earnings forecasts by 84% last Thursday, maintaining full-year production guidance, confirming more than 30,000 reservations on top of a multi-year order for 100,000 EVs from Saudi Arabia and ample cash of $5.4 billion to take Lucid well into 2023, LCID stock is down roughly 16% to fresh YTD lows in the report’s wake.

So, what gives? One thing is certain, it’s not entirely a case of investors’ throwing the baby out with the bathwater in a risk-off environment.

Importantly, while guidance of 10,000 – 12,000 vehicles remained intact, Lucid already cut its production outlook by 45% at the range midpoint from 20,000 in February as supply chain items like glass and carpet joined popular semiconductor snarls as bearish talking points. Moreover, with Covid-19 and Russia still manufacturing scarcity on a global scale, the idea of LCID stock having another shoe to drop can’t be dismissed. Not today at least.

Another feature weighing on investors was Lucid’s decision to raise prices on new reservations for its EVs by 10% to 12% beginning next month. With rising interest rates and wallets stretched by the basics, already pricey big ticket items like the Air EV may prove out of reach — and the Air’s rather measly $300 reservation, acceptable collateral damage from would-be buyers.

Lucid Motors Remains a Riskier Buy

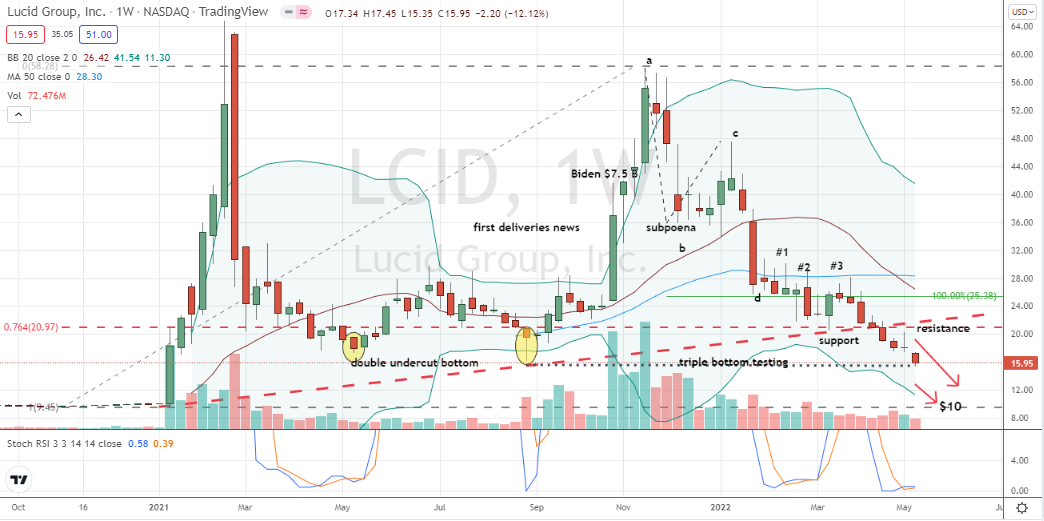

Click to Enlarge

It’s hard to ignore last November’s peak of $57.75 or last January’s all-time-high of $64.87 and not reminisce about the good ol’ days or simply get excited with LCID stock’s current price of $15.95, right?

Those hyped halcyon days have been squarely put to rest. But Wall Street isn’t impressed with LCID stock. And at the moment neither should you.

Aside from the fact that Lucid has done an admirable job of putting the rubber to the road during the pandemic and a compounding Russian headwind, LCID stock remains a higher multiple proposition with no profits and negative cash flow.

If sales forecast of $1.295 billion for this year are met, that still means a large-cap valuation of $30 billion for Lucid shares at roughly 23 times 2022 revenues. And outside of more normalized markets, that’s always going to be expensive. What’s more and given today’s operating constraints, the risk is the possibility of much lower production, not a meaningful upside surprise. Not this year.

Steer Clear of LCID Stock

Technically, the case for an oversold and developing triple bottom pattern in LCID stock can be made. But it’s not a bullish formation that’s worth buying into.

Confirmation for a weekly low remains absent. And coupled with a weak-looking Bollinger band setup, a trading environment that’s been unforgiving to those type entries and many “de-SPACed” stocks now trading at much deeper discounts to their former net asset values (NAV), a return move to $10 or lower in LCID stock shouldn’t be dismissed.

Today, a move from around $16 to $10 or worse could prove a highly profitable venture for Lucid bears wishing to join the ranks of the stock’s roughly 19% short interest. If that’s you, I’d only suggest using a limited risk put or bear vertical as to avoid always possible, larger-than-expected losses.

And if you’re bullish and unwilling to concede on an anticipated costly purchase in-the-making, I’d similarly point to LCID stock’s options and where upside price objectives can be maximized alongside defined exposure with relative efficiency.

On the date of publication, Chris Tyler did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.