This article is excerpted from Tom Yeung’s Profit & Protection newsletter. To make sure you don’t miss any of Tom’s picks, subscribe to his mailing list here.

When we at InvestorPlace launched Tom Yeung’s Profit & Protection earlier this year, I knew that markets were in for a rough ride. Oil had reached multi-year highs and “inflation” was starting to mean more than my pandemic-related pounds.

But the stress on ordinary Americans has been a surprise, even for yours truly. Real estate prices are now so high that someone earning a starting salary in Chicago would need two roommates to afford the average 1-bedroom apartment. In New York City, that person would need four.

Career professionals are also feeling the heat. Inflation is eating away at 401(k) values — leaving savers with less than before — while blue chips from Amazon (AMZN) to the Vanguard Long-Term Corporate Bond ETF (VCLT) have fallen a quarter this year. Stagflation fears are even making me lose my appetite.

Some Conservatism Goes a Long Way

But the quality-growth picks of Profit & Protection’s core list have done remarkably well. 3D printing firm Desktop Metal (DM) is up 25% since May, while online discount retailer RealReal (REAL) is up 15%.

That’s because this newsletter focuses on high-potential companies with significant downside protection.

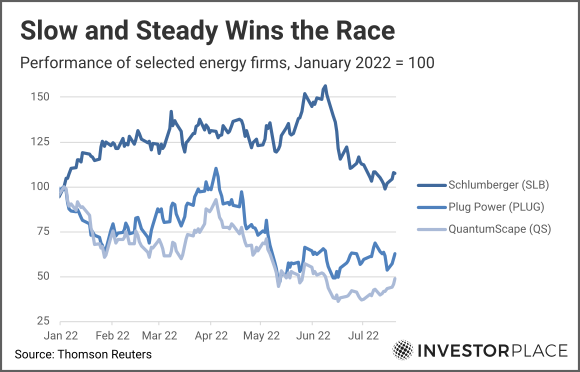

Often, this means ignoring stocks with the highest upside potential. Profit & Protection’s core list passes over green energy moonshots like battery developer QuantumScape (QS) and hydrogen mobility firm Plug Power (PLUG), despite their potential to go 10x. Instead, this newsletter’s lone energy pick is Schlumberger (SLB), a company that has avoided losing two-thirds of its value in the past year, unlike its flashier peers.

Nevertheless, this newsletter still partakes in some longshot investments. When a fat pitch comes along, it’s worth swinging for the fences

Companies Trading at Book or Liquidation Value

In 1934, Warren Buffett’s mentor Benjamin Graham introduced “net-net” investing — the concept of buying stocks below their current asset values.

Mr. Graham had plenty of choices at the time; the 1929 market crash had sent prices down so far that many firms traded for less than liquidation value

In 2022, we too, still have some choices if we know where to look.

SoFi (SOFI)

In June, I highlighted SoFi (SOFI) as a top pick:

“SoFi (SOFI) is now trading at all-time lows. It’s now a buyout target with 2x to 3x return potential and is one of my favorite speculative picks.”

That’s because shares of this fintech firm had suddenly dropped below book value — a rare phenomenon among high-growth startups.

Squint hard enough and you’ll see some of the reasons why SoFi traded at such a discount. Investors were caught off guard by the student loan moratorium extension that President Biden signed in June, and rising rates have put a lid on debt refinancing.

But SOFI’s stock had become too cheap. Since adding SoFi to my list of favorite speculative picks, shares have risen 22%. The company now earns a Profit & Protection “A+” for its improved momentum and remains a solid speculative pick under $10.

Desktop Metal (DM)

In May, this Boston-based 3D printing company briefly traded at its takeover price.

“Businesses returning to the U.S… could make Desktop Metal worth billions… [but a] corporate failure might value the firm closer to a $1.50 buyout price”

When shares did fall to $1.50, I was so excited that I immediately sent a note to our company’s CEO to tell him the good news (He was less enthused that a top stock had fallen so far).

Since then however, shares of Desktop Metal have surged back to almost $3.

And there’s still more room to run.

That’s because Desktop Metal stands at the cutting edge of 3D printing technology. The firm has wisely focused on high-speed metal and fiberglass printing, giving it an edge over rivals in industrial applications. And bipartisan support for re-onshoring American manufacturing has become a much-needed tailwind in the industry.

Desktop Metal still has plenty of growing up to do. The firm loses nearly $2 for every $1 of revenue. And the firm still has to convince manufacturers — which largely still rely on casting — to make the jump to a new production method.

But with its “A+” Profit & Protection grade, Desktop Metal stands as the most promising bet on an emerging technology. Should the company gain scale, shares won’t stay under $10 forever.

HanesBrands (HBI)

Rounding out the list of unusual valuations is HanesBrands (HBI), the maker of innerwear and Champion-branded activewear.

The firm is an unusual case of a mispriced company — though it trades at 4x book value, much of its brand assets don’t show up on its balance sheet.

Instead, value investors need to look at Hanes’ strong cash flow to get a sense of intrinsic worth. The apparel firm generates up to $600 million in free cash flow every year, valuing the firm at $5 billion or more.

Demand for underwear is non-cyclical — a major draw for investors seeking a haven in uncertain times. HBI has generated positive cash flow every year since its spinoff from Sara Lee in 2006.

That makes HanesBrands an extraordinary value play when countercyclical stocks are trading for premiums. Though HBI has nudged past $10, investors still have time to jump in on a company trading at 6x cash flow.

Redfin (RDFN)

Last week, I added Redfin to our list of tactical trades:

“Redfin’s business doesn’t rely on mortgage refinancing or the number of homes sold (Its loss-making mortgage business only exists as a convenience to homebuyers).

Instead, the company’s top line depends on the total volume of housing transacted. Analysts expect that figure to rise 6% to 8% as increasing home prices offset a decline in the number of units sold.”

In other words, Redfin has fallen victim to a massive misunderstanding. Because home prices are still rising, Redfin’s revenues will rise surprisingly even as the house sales volume declines.

That stands in contrast to other tech-based real estate firms. Zillow’s (ZG) revenues will fall over the next two years as it retreats from its home-flipping business. And fintech mortgage firm Rocket Companies (RKT) has already seen declining demand for its refinancing business.

Redfin’s association with these businesses has pushed its shares’ value to historically low levels. Investors buying in today will receive a company that’s trading for 0.4x forward sales.

And investors can sleep soundly at night too. The company earns an “A+” in the Profit & Protection system thanks to its high “value” and “momentum” scores.

RealReal (REAL)

Finally, investors looking for a higher-risk wager should consider RealReal, a company I called “the top ecommerce company to buy for summer 2022.”

“At first glance, the RealReal looks like a bust when it comes to ecommerce plays. Founder/CEO Julie Wainwright abruptly resigned earlier this week after overseeing a 90% share price drop since its 2019 IPO.”

Those events pushed the value of RealReal’s shares under $3 for the first time in its short history.

And why it caught my eye:

“RealReal has become so cheap that it’s now a potential acquisition target.

As the quant-based Profit & Protection pointed out, the firm’s rapid growth rate and improving profitability make its $3-per-share price as tempting as some of its online offerings… I estimate that investment bankers will start sniffing around at $2.50/share, and offers come in no lower than $2.00.”

Analysts expect the firm to grow 40% this year and 25% over the next, giving the company a solid “A+” grade for growth and an “A+” overall.

There are plenty of risks, of course — a fact I highlight at length in my detailed report. But those willing to take the gamble could see a 2x… 5x… even 10x return on their investment.

Other Moonshots Worth Considering

Bouts of market depression can create opportunities in high-risk stocks. Consider Apple in 1997… Amazon in 2000… Facebook in 2012…

These stocks would go on to make millions for their investors.

And there’s one thing in common that defines these companies:

They made products that were so different that competition couldn’t keep up.

A similar trend is now happening in the world of bioengineering. And Ginkgo Bioworks (DNA) is leading the way.

The Boston-based firm uses gene editing to turn ordinary plant and bacteria cells into miniature factories. Want food-grade animal proteins from yeast? Or microbes that convert garbage into valuable chemicals? These realities are closer than they appear, thanks to advances that Ginkgo Bioworks is pursuing. The firm is added to the “speculative picks” section of the Profit & Protection list.

Meanwhile, value-oriented investors are also finding incredible deals. This week, I’m also adding XL Fleet (XL) as a speculative pick. The vehicle electrification company has struggled to grow — many insiders blame management for lack of a startup mentality. But at $1.25, shares have also become absurdly cheap. Its $330 million cash pile now gives the firm a negative $150 million enterprise value.

In other words, management could liquidate the company today and give $3 back to every shareholder for a 100% gain.

More likely, XL Fleet will get taken over. Don’t be surprised if a larger company swoops in at the $3 to $5 range.

Core Profit & Protection “Buy” List

| Ticker | Name | Date Added | Return |

| Technology | |||

| APPF | Appfolio | 7/15/22 | 3% |

| CRWD | CrowdStrike | 5/27/22 | 10% |

| ETSY | Etsy | 5/20/22 | 18% |

| OKTA | Okta Inc | 6/24/22 | 2% |

| PANW | Palo Alto Networks | 6/24/22 | -1% |

| RDFN | Redfin | 7/15/22 | 15% |

| REAL | The RealReal | 6/17/22 | 19% |

| ZS | Zscaler inc | 5/27/22 | 2% |

| Industrials / Communications | |||

| DM | Desktop Metal | 5/20/22 | 29% |

| T | AT&T | 6/2/22 | -3% |

| TIGO | Millicom | 6/2/22 | -16% |

| Healthcare / Staples / Finance | |||

| BHC | Bausch Health | 6/2/22 | -5% |

| BLCO | Bausch and Lomb | 6/3/22 | -9% |

| HBI | HanesBrands | 5/20/22 | -2% |

| SCHW | Charles Schwab | 7/1/22 | -2% |

| Energy / Materials | |||

| SLB | Schlumberger | 7/8/22 | -1% |

| Speculative Picks | |||

| BEAM | Beam Therapeutics | 7/7/22 | 31% |

| CRSP | Crispr Therapeutics | 7/7/22 | 5% |

| DNA | Ginkgo Bioworks | 7/21/22 | 0% |

| SOFI | SoFi Technologies | 7/1/22 | 29% |

| XL | XL Fleet | 7/21/22 | 0% |