If you’ve been paying attention, you know that tech stocks have been the rocket fuel propelling this bull market to dizzying heights. However, these high-flyers could come crashing back to Earth when the downturn hits.

Many tech darlings have already suffered steep pullbacks. And if macros get worse, the pain for these overvalued names will only worsen. It’s time to take a page out of Warren Buffett’s playbook and start rotating into safer assets.

Dividend stocks are looking mighty attractive at these valuations, and Treasury yields are juicier than they’ve been in years. Sure, a recession isn’t guaranteed. But with so many indicators flashing warning signs, it’s a good idea to take some profits.

No one can predict how ugly things might get. But if you’re looking to play some defense, here are seven tech stocks to sell before the potential plunge:

Palantir (PLTR)

Palantir (NYSE:PLTR) provides data analytics software to government agencies and large corporations. The company has seen strong revenue growth, especially from its U.S. government contracts which grew 24% year-over-year in Q2 2024.

While Palantir’s deep government ties make it a stable long-term investment, I wouldn’t touch this stock with a ten-foot pole heading into a potential recession. Trading at a nosebleed valuation of 83 times forward earnings and 24 times sales, Palantir is priced for perfection. However, with analysts expecting revenue growth to decelerate to the 20% range next year, I doubt the market will keep paying such a hefty premium.

Bears like Mizuho’s Gregg Moskowitz are already sounding the alarm, recently downgrading Palantir to “Underperform” on valuation concerns. He notes the stock trades at “an exceedingly large 160% premium” to software peers. When the economy turns south, and investors flee to safety, high-flying names like Palantir could be in for a rude awakening. If you own it, I’d lock in profits before the bottom falls out.

Coinbase (COIN)

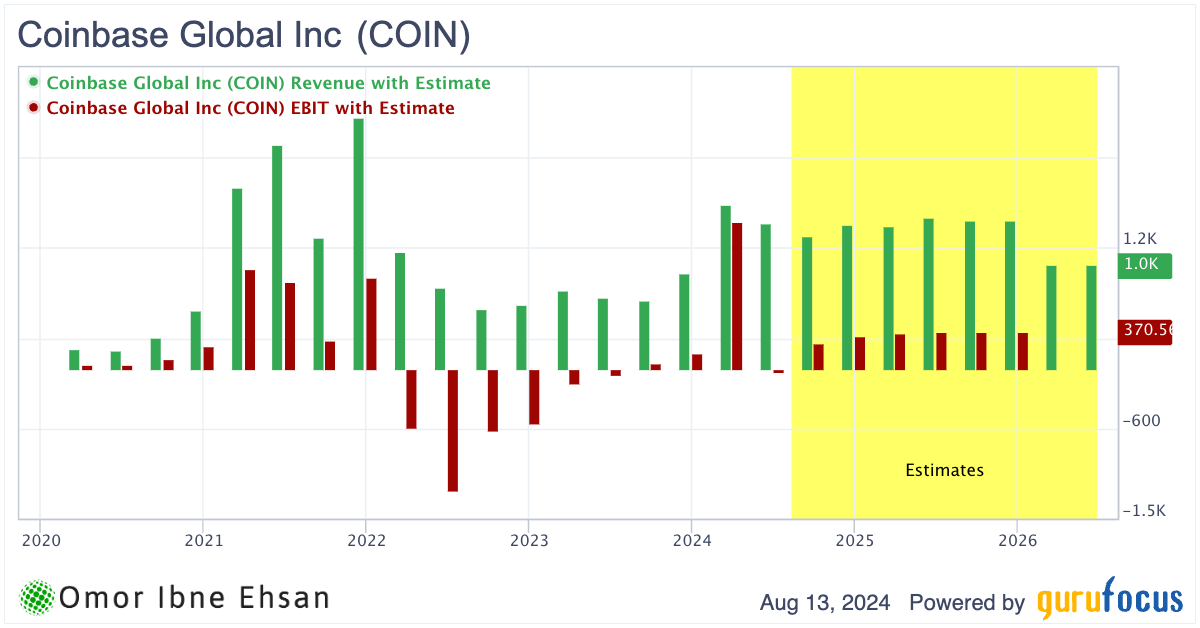

Coinbase (NASDAQ:COIN) operates a cryptocurrency exchange platform. The company has been struggling lately, with its stock price down over 28% from its 2024 highs amid a broader crypto market downturn.

If you’ve paid any attention to the crypto market, you know it’s prone to extreme volatility and sentiment-driven swings due to the speculative nature of most cryptocurrencies. Coinbase’s fortunes are strongly tied to this erratic market, which is why I believe it’s one of the riskiest stocks to own heading into a potential recession.

Bitcoin (BTC-USD) has only weathered one recession so far in 2020, and it didn’t exactly shine. With BTC still trading at lofty levels, there’s plenty of downside risk. Coinbase also relies heavily on the altcoin market for revenue, and that’s been absolutely crushed lately. In a recession, expect altcoins to get obliterated as investors flee to safety.

Despite this, Coinbase trades at a steep 35 times earnings and over eight times sales.

Click to Enlarge

Analysts expect revenue to decline in coming years until the next Bitcoin halving (possibly) sparks another speculative frenzy. In my view, blockchain stocks are only worth chasing at rock-bottom valuations, not these nosebleed levels.

Robinhood (HOOD)

Robinhood (NASDAQ:HOOD) operates a popular commission-free trading platform for stocks, options, and cryptocurrencies. The company has been on a wild ride lately, with its stock up nearly 200% from its 2023 lows to its July 2024 peak before plummeting 23% in the past month amid the broader market correction.

Robinhood reported record Q2 2024 results, with revenues surging 40% year-over-year to $682 million, GAAP earnings per share of 21 cents, and net deposits growing 41% to $13.2 billion. The company is benefiting from renewed interest in meme stocks and crypto trading. However, the Securities and Exchange Commission issued a warning in May about potential enforcement action against Robinhood’s crypto business.

In my view, Robinhood is pretty similar to Coinbase. Sure, Robinhood is more insulated since it doesn’t rely entirely on crypto, but the platform attracts a lot of sentiment-driven users targeting volatile stocks. I think a recession could be a nightmare for HOOD stock. The recent correction caused a steep 23% drop in just a month.

I expect HOOD to amplify any market moves going forward, so with a potential recession looming, this is a no-go for me.

Matterport (MTTR)

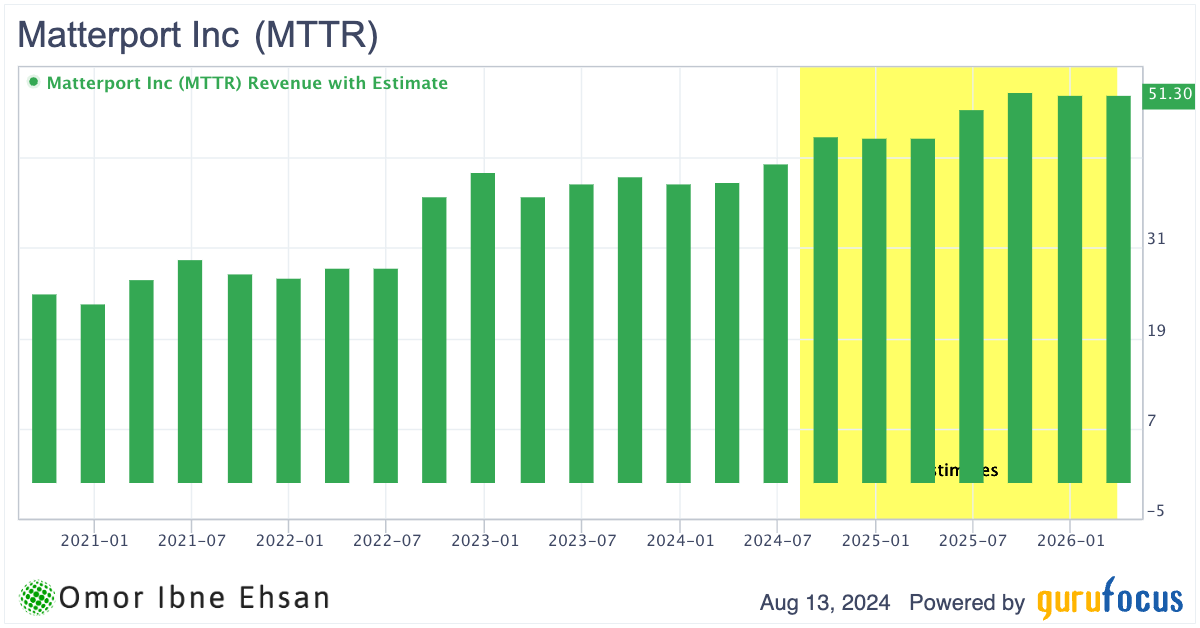

Matterport (NASDAQ:MTTR) offers a spatial data platform for digitizing and managing buildings, but I’d steer clear of this stock and most others in the space industry right now. The company has been experiencing solid growth, with Q2 revenue up 6.7% year-over-year to $42.2 million, but its losses are mounting at an alarming rate. Net loss ballooned to a staggering $141.6 million in Q2, a 150% increase from the prior year.

The space sector is highly dependent on external funding, which will likely dry up fast if a recession hits in the coming quarters. With only around $364 million in cash remaining, Matterport could burn through its reserves. Even if a downturn is avoided, this startup will still be unprofitable for a while with low revenue growth.

Click to Enlarge

A stock with fundamentals like this does not deserve to trade at nearly 8x forward sales.

There are also plenty of other companies in the geospatial data sector that are already profitable and get much more attention from investors.

C3.ai (AI)

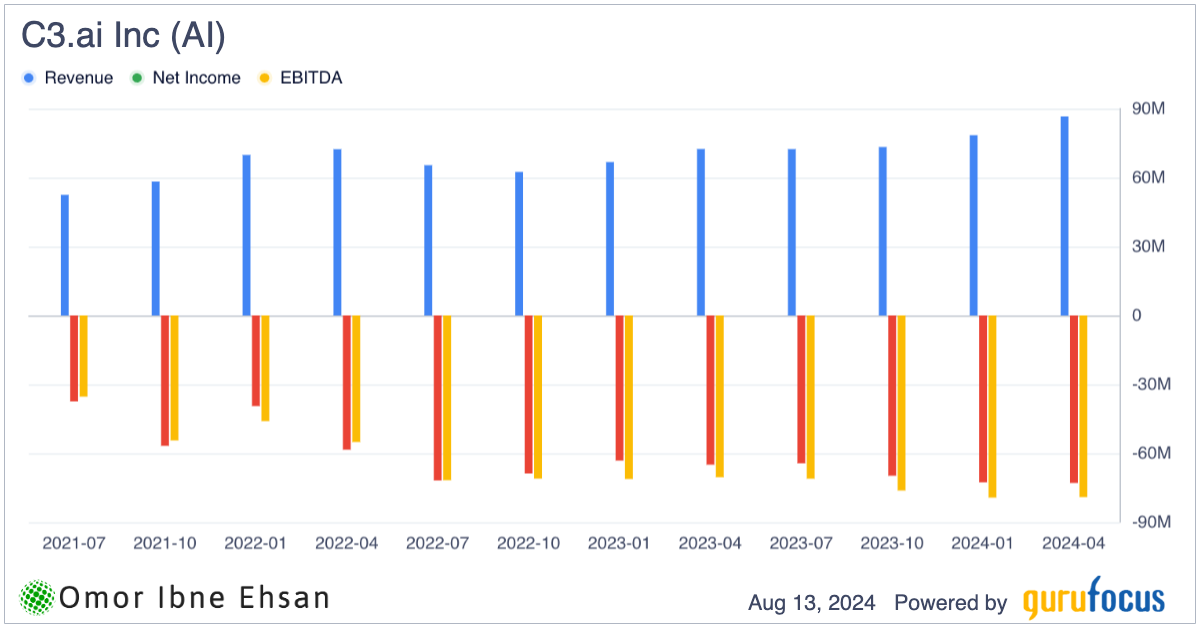

C3.ai (NYSE:AI) provides enterprise AI software for accelerating digital transformation. The company has been riding the recent AI hype wave, with its stock price soaring over 200% year-to-date despite lackluster fundamentals.

In my opinion, C3.ai is probably one of the worst stocks you could buy heading into a potential recession in 2024. The company’s recent Q4 FY2024 results showed revenue growth of 20% to $86.6 million, but it still posted a hefty net loss of $82.3 million. Subscription revenue, while growing 41%, comes with a dismal -84% gross margin. Analysts at firms like Morgan Stanley remain skeptical about the company’s path to profitability, with current projections not expecting positive earnings until fiscal 2027.

Management is sitting on lots of cash, but even then, I don’t think Wall Street will be too keen to keep paying premium for a business that has such terrible margins.

Click to Enlarge

I believe C3.ai’s rally has been driven more by its fortunate ticker symbol and “AI” in its name rather than the actual substance of its business. The company touts AI capabilities, but in reality, it’s more of a buzzword – its products are closer to traditional enterprise software. C3.ai also has significant customer concentration risk, with oil services giant Baker Hughes (NASDAQ:BKR) accounting for a large chunk of revenue.

If the AI hype fizzles out or the economy sinks into a recession, C3.ai could be in for a rude awakening.

Virgin Galactic (SPCE)

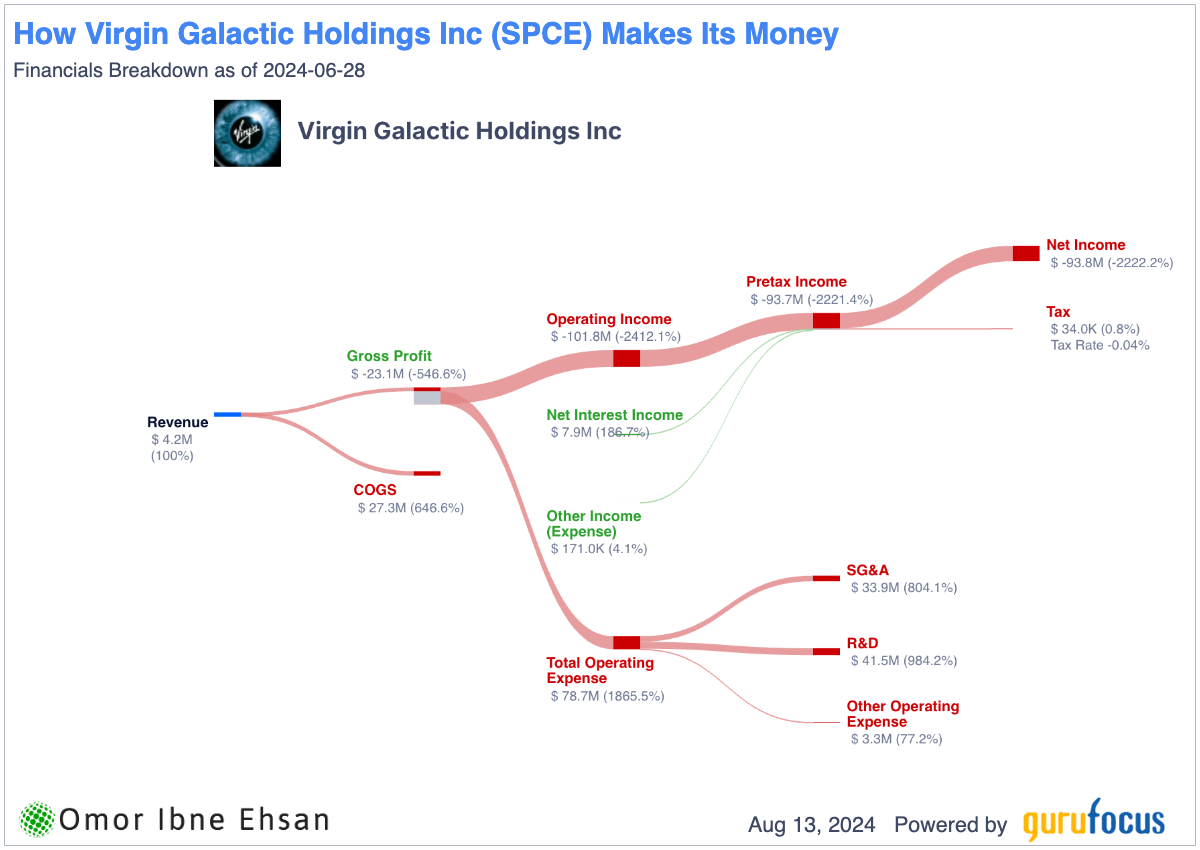

Virgin Galactic (NYSE:SPCE) is a space tourism company that aims to send paying customers to the edge of space. Recently, the company has been struggling financially and operationally despite completing its final mission with the VSS Unity spaceplane in Q2 2024. In my opinion, Virgin Galactic is a stock I’d stay light years away from in a normal economic climate, let alone a potential 2024 recession.

The company is hemorrhaging cash, reporting a net loss of $94 million in Q2 2024 and burning through $114 million in free cash flow.

Click to Enlarge

If it survives, I really don’t think this company will ever break even.

Analysts like Wells Fargo remain bearish, citing a lack of positive catalysts and cutting their price target to a dollar. I simply think Virgin Galactic is too far ahead of its time. Even with plans to launch the Delta class ships in 2026, it could take many years, if not decades, for space tourism to become solidly profitable.

While the wealthy are the target market, ticket prices around $300-450k aren’t exactly affordable, and I question the sustainability of customer demand. Space tourism seems more like a once-in-a-lifetime experience rather than a recurring revenue generator. With a recession looming, I believe you should jettison this stock from your portfolio before it crashes back down to Earth.

Lucid (LCID)

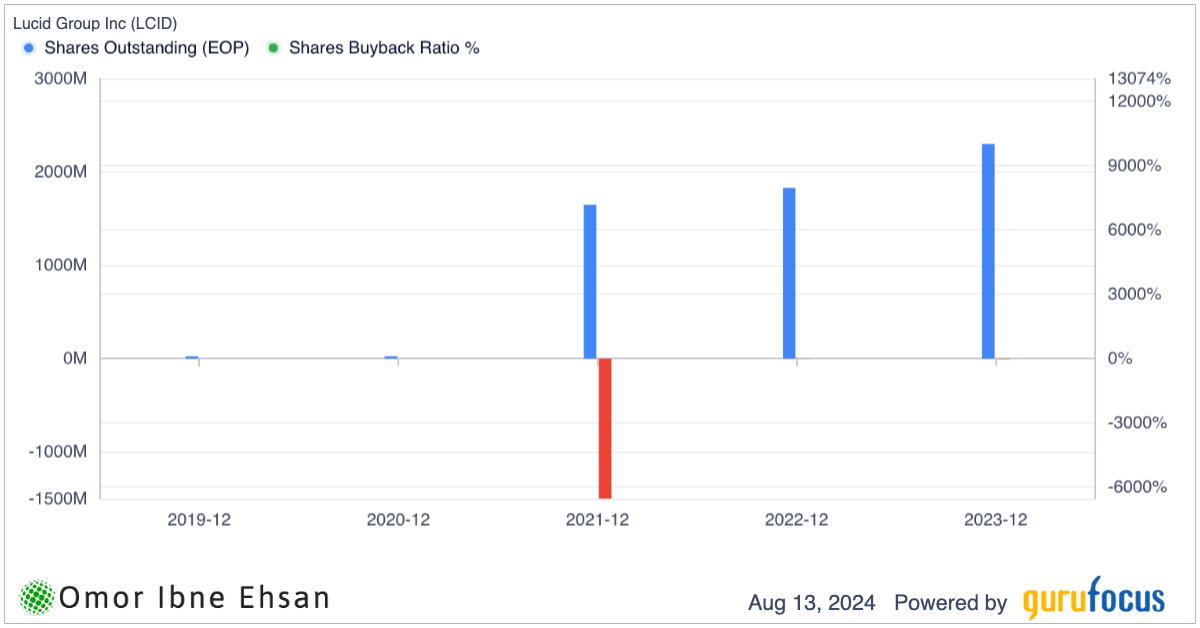

Despite reporting record deliveries in Q2 2024 and securing $1.5 billion in additional funding from Saudi Arabia’s Public Investment Fund, I think Lucid (NASDAQ:LCID) will still head to bankruptcy. The company posted a net loss of $643 million in Q2 on revenue of just $201 million.

I don’t think the company can achieve the scale and efficiency needed to compete with established EV makers. Its biggest rivals are already profitable and dominate the market. Lucid’s upcoming Gravity SUV will also face stiff competition from Rivian (NASDAQ:RIVN).

Plus, Lucid’s reliance on Saudi investment is the most concerning part. The Saudi PIF clearly believes in Lucid’s long-term potential, but if a recession hits, tanking oil prices could force them to pull back.

Click to Enlarge

In the meantime, Lucid will likely continue diluting shareholders to help fund operations.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.