¡Salud! Santé. Na zdrowie. Cheers!

Don’t worry; you’re not stuck on Disneyland’s “It’s a Small World” ride. Although when listing various toasts “to health,” it could feel like it.

Nearly every language has its own version of this sentiment. And these proclamations often accompany raising a drink or clinking glasses. But no matter the country, the wish is globally the same: goodwill.

This year, the healthcare industry could use its own toast “to health.”

In a stock market packed with richly priced companies, the pharmaceutical sector has become a conspicuous outlier. Investors have been rushing to the stage to cheer AI rock stars like Nvidia Corp. (NVDA) and Alphabet Inc. (GOOGL), while dismissing most pharma names as has-beens.

Ironically, in a market obsessed with AI stocks, few investors seem to care how extensively the biopharmaceutical industry has integrated AI technologies.

That oversight is exactly what creates opportunity.

Away from the crowds and the blinding lights, drug companies are quietly entering a period of renewed strength, much like they did in the early 1990s.

That’s why I’m raising a glass to an overlooked biopharmaceutical company with the hidden capacity to deliver outsized gains.

Below, I’ll share some details on this company… and where you can find more drug stocks that possess market-beating potential.

But first, let’s take a closer look at the health of the healthcare sector, and why it’s primed for opportunity…

A Once-in-a-Generation Discount the Market Is Ignoring

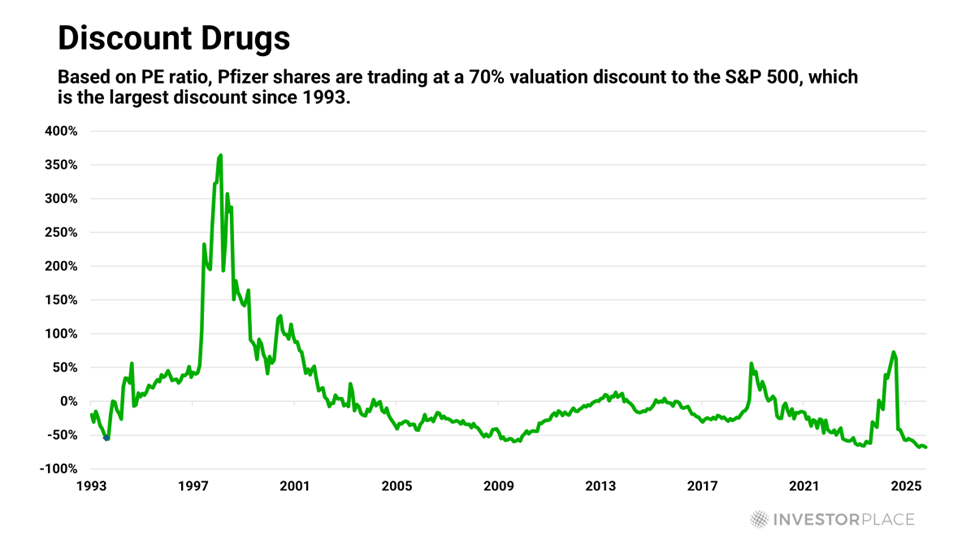

Valuations across the healthcare sector have tumbled to record lows relative to the S&P 500. You’d have to go back more than 30 years to find valuations this depressed.

Consider Pfizer Inc. (PFE) as an example, which is trading at a record-low 70% discount. Put differently, investors are now paying about 70% less for a dollar of Pfizer earnings than for a dollar of earnings from the S&P 500 as a whole.

This is the largest discount since 1993 – right before the start of a powerful bull market for healthcare stocks. Over the next six years, PFE soared more than 1,000% over the S&P 500 index.

In hindsight, that opportunity should have been obvious. The company was entering a new growth phase, producing profit margins twice as high as those of the S&P 500.

Today, the fundamentals look even stronger than they did in that 1994 trough. Pharma’s cash flows are on the rise, gross margins are still roughly double the S&P’s, and the sector is integrating AI in ways that will likely make drug development faster, cheaper, and more precise.

As an added plus, the sector offers a healthy 3% dividend yield – more than double the S&P 500’s.

For patient investors, the setup is enticing: a sector priced for disappointment, despite fundamentals that point in the opposite direction.

One company is a clear example of this disconnect. Its valuation suggests stagnation, yet its operations tell a different story: accelerating growth in newer therapies, a deepening pipeline across major disease areas, and a strategic embrace of AI that should make future innovation faster and more predictable.

Here are the details…

Gaining Momentum at a Discounted Price

The company I’m referring to is Bristol-Myers Squibb Co. (BMY).

It is one of the largest pharmaceutical companies in the world, with a number of drugs that treat diseases in immunology, cardiovascular, and oncology.

Plus, I believe this company possesses enormous potential to generate robust profit growth from its AI initiatives.

That means that Bristol-Myers is no longer just a drugmaker. It is becoming a digital-first biomedical company.

CEO Chris Boerner put it plainly in the company’s latest earnings call: “We are integrating digital technology and AI across the company to drive efficiency and speed in how we discover and develop medicines.”

The impact is already visible. Trials start sooner. Patients are matched more efficiently. Data quality improves.

In drug development, speed lowers cost and higher-quality data increases the odds of success. Bristol-Myers is applying AI to improve both.

Boerner also remarked, “Q3 was another strong quarter, reflecting focused execution across the business as we continue to make progress on our plan to position Bristol-Myers Squibb for long-term sustainable growth.”

The results backed him up.

The company’s “Growth Portfolio” – the group of newer drugs that must replace its aging blockbusters – grew 17% year over year. Opdivo and Qvantig, key cancer immunotherapies, continued their steady advance.

Given these positives, the company raised its midpoint revenue guidance for the year from $46 billion to $47.75 billion and bumped its earnings-per-share guidance to $6.50. Free cash flow is rising sharply, and net debt continues to decline.

Bristol-Myers trades for about seven times forward earnings – one-third of the S&P’s multiple – and yields more than 5%, backed by strong free cash flow and an A-rated balance sheet.

Those numbers suggest a tired, no-growth company, yet its business is clearly regaining momentum. Bristol-Myers is not trying to reinvent itself; it is simply executing, steadily and visibly, in ways that the market has yet to appreciate.

But I believe the stock still offers significant upside.

And it’s not the only healthcare play that offers significant, market-beating potential…

Two Healthcare Winners Already Proving the Bears Wrong

I currently recommend two drug stocks to my paid members at Fry’s Investment Report. Both have advanced nearly 50% year-to-date, compared to the S&P’s 13% gain.

I consider these companies to be new-and-improved “Buys” right now. That is why I spotlighted them in the November monthly issue of Fry’s Investment Report that I released just yesterday.

You can learn how to access the names of these healthcare recommendations here.

As I mentioned, Wall Street has its attention squarely on dazzling AI darlings like Nvidia, which releases its latest quarterly earnings report later today. (I’ll share more on that tomorrow.)

That means that the healthcare sector’s current discounted valuation, in combination with its considerable long-term growth potential, offers compelling opportunities in today’s richly priced market.

And to that I say: Cheers!

Regards,

Eric Fry