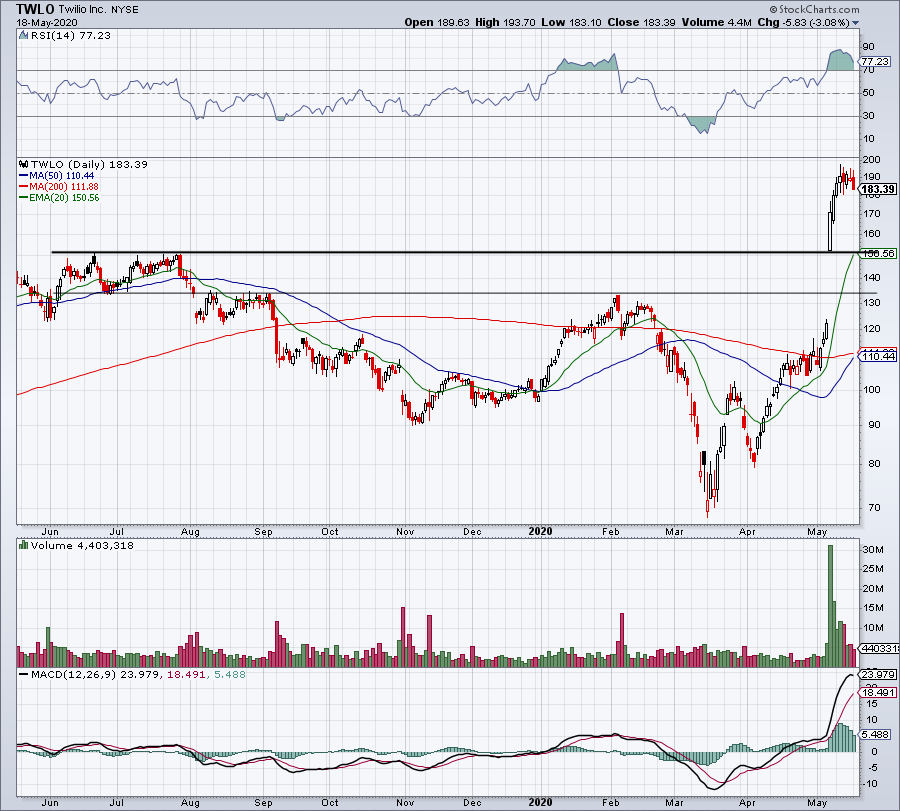

Twilio (NYSE:TWLO) is erupting higher after surging from $122.40 ahead of earnings, to roughly $190 after the print. To say TWLO stock has been on fire would be an understatement.

Shares are up about 55% since the company reported its first-quarter results on May 6. From the lows, Twilio has surged about 180%, putting an end to any talks of its growth.

The company is clearly on fire as shares climb to new all-time highs. For investors though, that puts them in a difficult position. Should they chase TWLO stock or have they missed the boat?

Growth Aplenty for TWLO Stock

Twilio reported earnings of 6 cents per share, beating estimates by 17 cents as analysts were expecting a loss. Revenue of $364.8 million ripped 54% year-over-year and beat estimates by more than $36.5 million. There are a few things to extrapolate from the quarter, though.

First, when the company reported earnings in February, profit was the culprit behind the selloff. After reporting a top- and bottom-line beat for Q4, management’s revenue outlook for next quarter and the full year topped consensus expectations. But in both time frames, they forecasted a loss rather than a profit.

Even though Twilio is still a growth story, profits need to eventually come. That irked investors at the time, so to see it swing back to profit this quarter while beating revenue estimates was impressive.

Second, the company is churning out strong growth — while maintaining focus on the bottom line — in arguably one of the most difficult environments possible. Due to the novel coronavirus, the business landscape has shifted for everyone. I’ve made the case before that companies with strong growth amid Covid-19 are worth an even larger premium than usual. That’s as growth has become even more scarce than it was before.

Lastly, guidance blew the doors off.

Management expects Q2 sales between $365 million and $370 million, and earnings between 8 cents and 11 cents per share. That compares to consensus expectations for revenue of $323.4 million and a loss of 14 cents per share, respectively. Management withdrew its full-year outlook because of the virus, but look at the staggering difference in expectations vs. guidance. It’s like the analysts aren’t even looking at the same company.

For these reasons — a positive profit surprise, growth amid coronavirus, and robust guidance — we still like TWLO stock. But we need a better price.

What Now for Twilio?

Now we know why Twilio is surging, but for those without a position, what do they do now?

We wait to buy the inevitable dip. No matter how great a growth stock is, the dip always comes. Before Shopify (NASDAQ:SHOP) surged more than 100% to its recent highs near $750, shares had slumped almost 50% to the low-$300s. Despite its monumental size, Apple (NASDAQ:AAPL) stock routinely dips 30% to 40% every few years.

Even our star pupil Twilio hasn’t been immune to a good old-fashioned slump. Shares fell 40% from the July high to the November low and almost 50% from the February high to the March low.

A 40% retreat from the highs in TWLO stock would land it near $117. But banking on a 40% drop is tough business. Short of a market-wide hammering, we’re unlikely to get anything like that in Twilio. Particularly after such a strong quarter.

Instead, what about a correction of “just” 23% from the highs, landing shares near the prior all-time highs at $151? Or a little deeper correction of 32% down to the $133 area, a major mark over the past year?

These levels may or may not play out in the future, but it’s worth being aware of them. We like Twilio for its strong growth, but need a dip first.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.