The second-quarter earnings reporting season kicked off in earnest on Friday as a number of Wall Street titans reported results. Expectations for profitability overall remains high: According to FactSet, factoring in the typical earnings beat rate, analysts have penciled in the second-best quarter of earnings growth since the end of 2011. But now, as hard numbers start flowing out, disappointment is in the air.

Stocks overall apparently couldn’t care less, however, as large caps pushed to new record highs.

Investors focused instead on a batch of poor economic data — specifically, weak retail sales and consumer price inflation numbers. Combined with some dovish commentary from Federal Reserve Board Chair Janet Yellen on Wednesday (focusing on the fact interest rates aren’t likely to rise very far this tightening cycle), this is reigniting the “Fed will save us” dynamic.

In the end, the Dow Jones Industrial Average gained 0.4%, the S&P 500 gained 0.5%, the Nasdaq Composite gained 0.6% and the Russell 2000 gained 0.2%. Treasury bonds were stronger across the curve, the dollar was under pressure, gold gained 0.8% and crude oil gained for the fifth straight session up 1%.

Breadth was positive, with 2.6 advancers for every declining issue on very light volume with NYSE activity at just 70% of the 30-day average. Not exactly confidence inspiring on a move to new highs. Nor was leadership by defensive areas, with REITs leading the way on a drop in yields up 1.1%. Financials were the laggards, down 0.5%.

Zillow Group, Inc. (NASDAQ:Z) gained 3.6% after the Seattle Times reported Amazon.com, Inc. (NASDAQ:AMZN) isn’t preparing a real-estate referral service. Sprint Corp (NYSE:S) gained 4.3% on reports Warren Buffett is considering an investment. And Gap Inc (NYSE:GPS) gained 2.2% after the stock was added to JPMorgan’s buy list.

On the economic front, consumer price inflation fell to a 1.6% annual rate form 1.9% prior. This missed estimates by a tenth, represented the weakest reading since October, and pulls the measure further from the Fed’s 2% target. Retail sales were weak, falling in six of the 13 major spending categories with department store sales down 0.7%. Consumer sentiment is cooling off as well, down from a 13-year high in January.

Turning back to bank earnings:

Citigroup Inc (NYSE:C) shares fell 0.5% recovering from an opening tick drop that took shares down 2.2%. The company reported earnings of $1.28 per share — seven cents ahead of estimates — on a 2% rise in revenues. That seems good, but represents a 3% decline from last year as higher revenues were more than offset by a higher cost of credit and increased operating expenses.

The cost of credit, which jumped 22% from last year, as driven by an increase in net credit losses of $94 million. This is classic late cycle behavior (a rise in non-performing loans and defaults) and could further pressure earnings should it continue and force an accumulation of loan loss reserves.

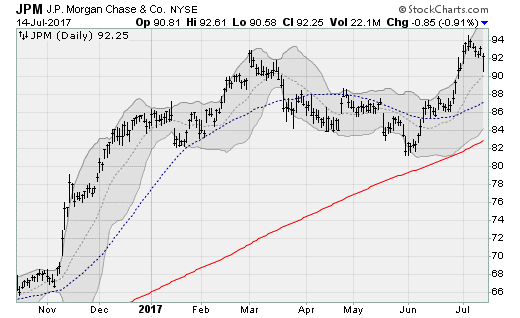

Click to Enlarge JPMorgan Chase & Co. (NYSE:

JPM) lost 0.9%, after falling as much as 2.7% as the open. Pressure was seen in the mortgage business, where revenue fell 26% on higher funding costs and lower production margins.

Also, on the post-earnings calls, CEO Jamie Dimon went a bit crazy and roared about how embarrassing it is, as an American, to listen to “this stupid shit we have to deal with” out of Washington D.C with a few audible pounds on the table for good effect.

And Wells Fargo & Co (NYSE:WFC) lost 1.1% after dropping as much as 2.7% as the open. Auto loan originations fell 17% from the prior quarter and 45% from last year, mortgage loan originations fell 13% from last year, and the mortgage loan pipeline contracted 28% from last year.

Conclusion

Even Wall Street brokerages are now peering behind the veil of this Pavlovian reaction to anything resembling dovishness from the Fed. And they don’t like what they see as therisks of the Fed blowing the market bubble up even further outweigh the risks of sticking to the policy hawkishness that seemed to be in play last week.

In a note to clients today, Bank of America Merrill Lynch strategists released a note to clients entitled “Take that punch bowl away” — pleading with the Fed to stop the charade before it’s too late.

Click to Enlarge In the context of narrow market breadth, extreme sentiment, extended investor positioning, very high leverage, and widespread complacency, if the Fed returns to its hawkishness next week amid an ongoing flow of uneven earnings, we could see a volatility breakout and violent market reversal.

But I also cannot dismiss the risk of a melt-up Fed-driven scenario — which has been seen ad nauseum time and again. But the lack of widespread market participation and tepid volume suggests a lower probability of follow on buying.

The tech-heavy Nasdaq has rallied for six straight session, and in seven of the lasts eight. So a pullback is way overdue.

Today’s Trading Landscape

To see a list of the companies reporting earnings today, click here.

For a list of this week’s economic reports due out, click here.

Anthony Mirhaydari is founder of the Edge (ETFs) and Edge Pro (Options) investment advisory newsletters. Free two- and four-week trial offers have been extended to InvestorPlace readers.