It was an ugly series of earnings releases for major department stores last week. First quarter revenue for Nordstrom, Inc. (JWN), Kohl’s Corporation (KSS), Macy’s, Inc. (M), and J.C. Penney Company Inc (JCP) fell a combined average of 2.6% against the year-ago quarter.

Although actual earnings per share performances were mixed, with Macy’s and JCP each beating their consensus targets, the underlining message was hard to ignore.

Consumers simply don’t have an appetite for department stores as they once did. Is this purely the rise of Amazon.com, Inc. (AMZN), or is there something more at play?

Of course, it’s easy to point fingers at Amazon — mostly because it’s true.

Since sparking the initial wave of the e-commerce revolution, AMZN and its ilk have been unstoppable. Online purchases account for more than 6% of all retail sales in the U.S., and that percentage is virtually guaranteed to increase.

There’s simply no beating the convenience of doing all of your shopping right at home. This was particularly true when national gasoline prices were blowing the rooftop. But even without that tailwind, Amazon has continued to challenge department stores at every turn.

Click to Enlarge

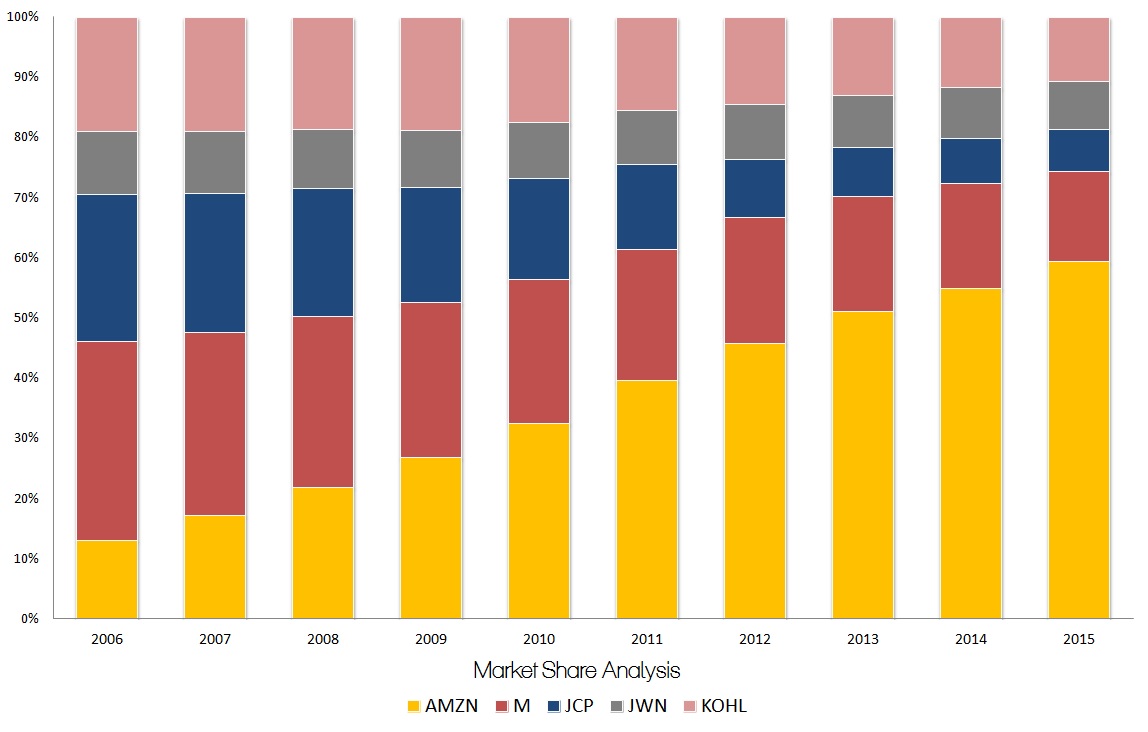

It’s really all in the numbers. Ten years ago, annual sales at the four department stores, plus Amazon, totaled $66.1 billion, with Kohl’s, Macy’s and JCP claiming 76% of market share. However, by the end of 2009, AMZN sales accounted for the majority against the department stores.

Last year, combined sales tallied up more than $180 billion. The difference maker? AMZN brought in over $107 billion in sales, or a whopping 59% of market share. If U.S. retail was the Republican Primary, AMZN is Donald Trump.

But before we jump to the obvious conclusion, consider this: between 2006 and 2013, market share for Amazon jumped 289%. However, since 2013, AMZN has only increased its footprint by 16%. This is nothing to scoff at, but it’s a far cry from earlier gains.

Further, it points to a readjustment in strategy among department stores to arrest the stunning rise of AMZN. So far, battered department stores have avoided the critical knockout punch from Amazon, but sales still lag.

What Else Is Killing Department Stores?

Strangely enough, what’s killing department stores recently may have less to do with e-commerce and more to do with “skinny jeans.”

Deutsche Bank analysts have noted that while sales of colored denim apparel have gained 4.5% in 2012, enthusiasm has since tapered down to a range between 1% to 1.6%. In other words, without a compelling reason to buy new clothes — outside the need for replacement — many consumers are simply holding off.

But it’s not just fashion designers that are to blame for lackluster sales at department stores. Brick-and-mortar stores, like Ross Stores, Inc. (ROST) and TJX Companies Inc (TJX), are hitting department stores where it hurts the most — their profit margins.

As off-price retailers, ROST and TJX deliver many of the same goods as their more illustrious competitors, but at reasonable prices. And with fashion apparently stagnating, the incentive to buy apparel at premium markups is simply non-existent.

Again, the numbers speak for themselves.

Click to Enlarge

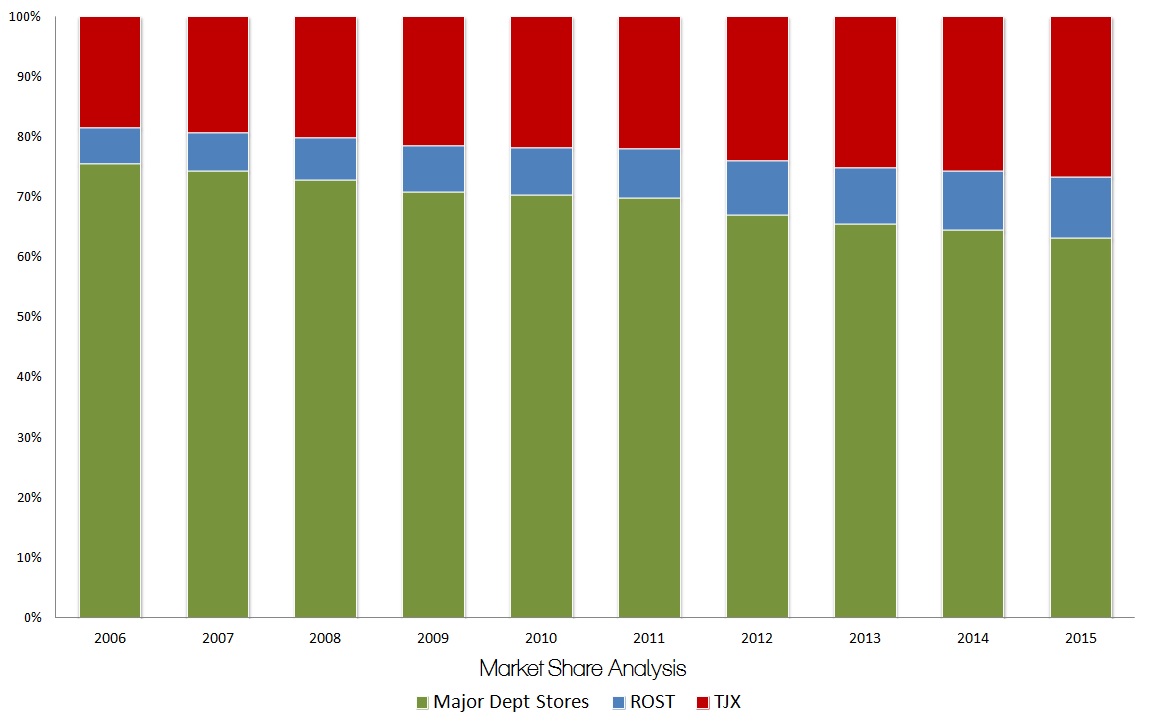

In 2006, sales of the three major department stores combined with ROST and TJX totaled $94 billion.

Of that amount, department stores took nearly 76% of market share.

Today, that footprint has dropped to 63%. ROST and TJX, on the other hand, have seen their market share increase by 51%. At the current rate, the two off-price retailers will collectively overtake major department stores inside ten years.

Although that forecast sounds slow compared to the meteoric rise of AMZN, off-price retailers might end up hammering the final nail in the coffin.

Department stores can directly compete with Amazon by improving their e-commerce channels. It’s a much harder proposition against stores selling similar goods, but at everyday low prices.

The sharp reduction in foot traffic at department stores suggests that consumers are finding their shopping needs wholly satisfied at discount outlets. Therefore, traditional retailers must cut back, or risk the ire of already panicky shareholders.

There is zero doubt that Amazon has gutted the future prospects of department stores. AMZN has completely changed the retail market, and there is simply no going back. At the same time, AMZN is a big cog in an even bigger gear.

While department stores are busy addressing the top-line threat of e-commerce, off-price retailers are steadily poking at their margins.

Fashion trends being stagnant, discount outlets are functionally offering identical products at steep markdowns, and that is what may ultimately send department stores to the abyss.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.