Retail stocks supposedly have a lot to look forward to this coming earnings season. Last Friday, the U.S. economy added 255,000 jobs, well ahead of the consensus estimate calling for 185,000 non-farm payrolls. Overall unemployment remained low at 4.9%, boosting both retail stocks and several other industries. Better yet, the jobs data is forcing a reassessment of the economy’s health. It may also encourage the chronically unemployed to get back on the saddle.

There’s just one problem. An improvement in nominal jobs growth with meager wage growth is like a dramatic increase in cell phones with barely any additional bandwidth.

When comparing the average hourly compensation of a production worker in the U.S., salaries have only risen about 10% in the past 40 years. That’s the equivalent of an annual raise of a quarter of a percent, hardly the confirmation of an improving economy. It also isn’t the advertised tailwind for retail stocks.

The other worrying sign is that the latest read from the University of Michigan’s Index of Consumer Sentiment is negative year-over-year, as is the Index of Consumer Expectations. Further, data provided by the U.S. Federal Reserve indicate that despite a rising trend of consumer sentiment since the financial collapse of 2008, Americans are only as confident as just prior to the big crash. Current sentiment is substantially weaker than the peak reading. That presents a top-line risk for retail stocks not named Amazon.com, Inc. (NASDAQ:AMZN).

The threat extends to “luxury-branded” retail stocks as well. Although high-end retailers cater to a more affluent clientele, few companies can afford to live off the rich alone. A declining middle class would negatively impact future sales as more workers find their wages stagnating. The general choppiness of luxury retailers ahead of a critical earnings test casts a shadow on the sector, as well as the underlying economy.

Here are three retail stocks that are flashing warning signs:

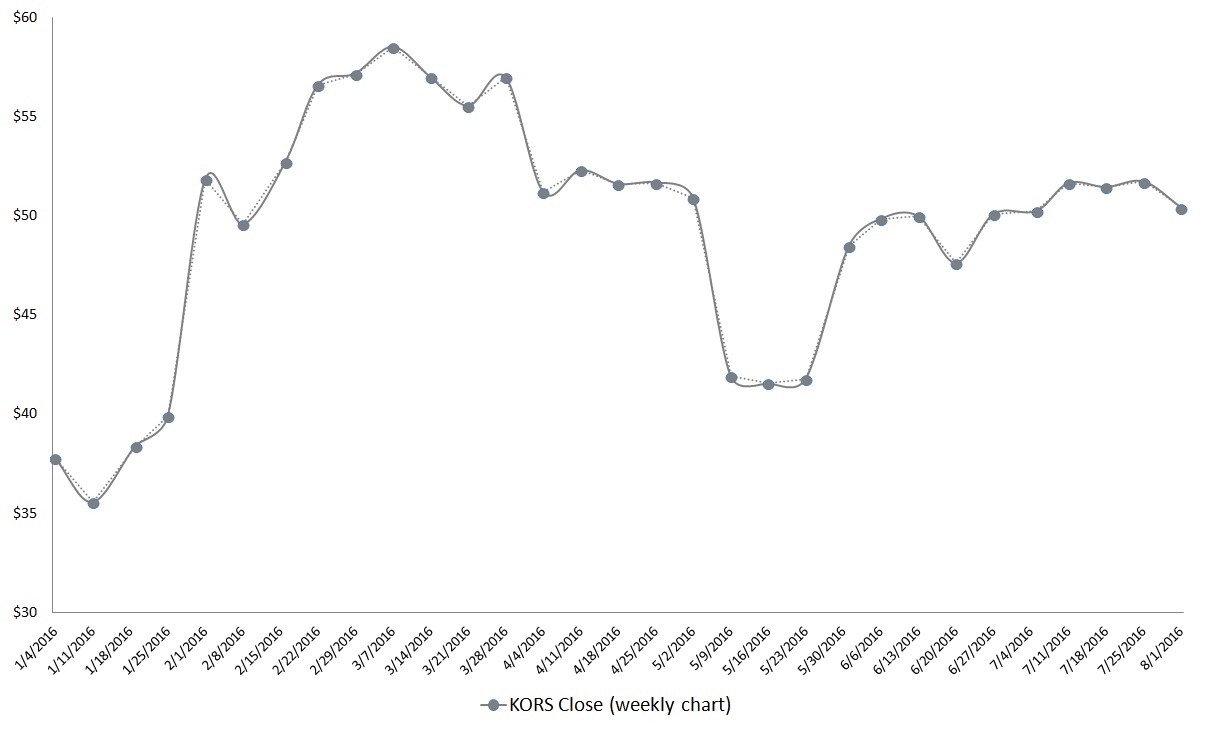

Retail Stocks to Watch: Michael Kors Holdings Ltd. (KORS)

Click to Enlarge

Year-to-date, KORS stock is up 25%, a feat that’s difficult to match in this ho-hum market. However, consumer culture experts have noted the declining image of the designer handbag as a status symbol. If things don’t drastically improve, KORS stock may be facing another steep correction.

The issue comes down to profitability. In a bid to attract customers who are increasingly moving to cheaper outlet stores, Michael Kors locations have increasingly relied on promotions and other discounts. That’s improved revenues but margins are taking a hit. As a result, earnings expectations for KORS stock are downgraded. For its first quarter of fiscal year 2017, consensus target for earnings per share is 74 cents. That’s the second consecutive time now that first-quarter estimates are lower than the year-ago level.

Of course, KORS stock has a history of beating earnings expectations, so a positive surprise in Q1 wouldn’t be out of the ordinary.

Still, there’s a reason why shares are down 14% since mid-March. Since Q4 FY2015, KORS stock has seen five consecutive times in which net margins have moved lower year-over-year. Although the company is considered undervalued against earnings, further hits to profitability makes the luxury retailer less enticing to investors.

For KORS stock, it’s not whether it beats earnings, but by how much. A less than adequate performance could be a problem moving forward.

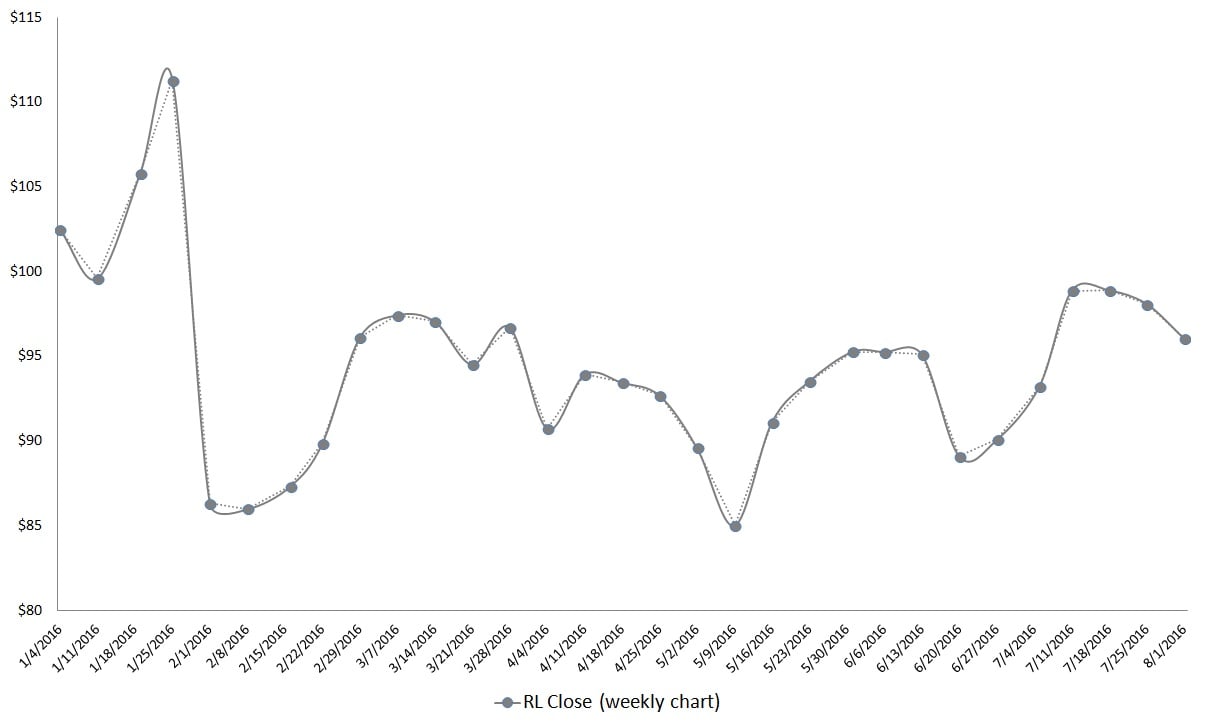

Retail Stocks to Watch: Ralph Lauren Corp (RL)

Click to Enlarge

To help its cause, the luxury brand has rolled out a crisp, conservative look that addresses the criticisms faced for their Sochi fashion faux pas. Most importantly, everything is made in the U.S. Will that be enough to overcome what’s otherwise a rough year for RL stock?

Luxury retail stocks will need something special to produce satisfactory results. Like Michael Kors, RL stock is more often than not on the right side of analysts’ expectations. However, the coming months and years ahead will certainly be trickier to navigate. The top line has been stagnant over the past three years, while net margins have been sinking to lower depths. At an EPS target of 89 cents for Q1 FY2017, downward estimates are alarmingly becoming the norm for RL stock.

With the bar set lower, Ralph Lauren shouldn’t have an issue to at least meet the consensus.

But how long will investors remain patient? RL stock is currently valued at roughly 21 times trailing earnings. That’s somewhat mediocre for retail stocks in the apparel industry. If profitability margins don’t improve, investors will lose even more incentive. Worst of all, RL stock is down 15% YTD, so there’s simply no room for error.

RL stock could experience a rebound, but the reality is that there are better options available.

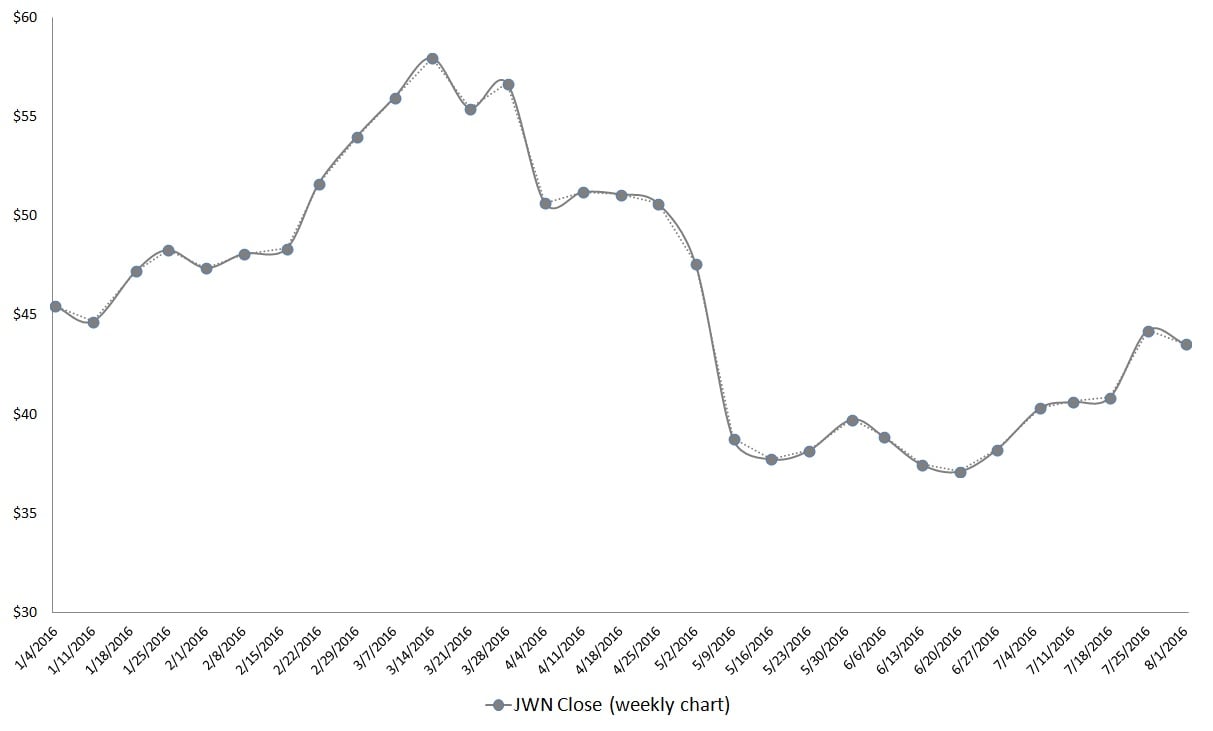

Retail Stocks to Watch: Nordstrom, Inc. (JWN)

Click to Enlarge

But at a loss of nearly 13% YTD, JWN stock is substantially worse than its two primary competitors, Macy’s Inc (NYSE:M) and Dillard’s, Inc. (NYSE:DDS). Macy’s YTD loss is a mere 3%; and even after the 3% beating DDS stock took Tuesday, it’s YTD loss of 7.5% still trumps JWN. Can JWN stock turn things around, or is it destined to follow the footsteps of other retail stocks?

While anything could happen, Nordstrom will have to pull off some serious magic tricks. Earnings results were very poor last fiscal year, missing all targets but one in Q2. For the upcoming Q2 report, the consensus target of 55 cents is 39% lower than the year-ago estimate. But an earnings beat is hardly a likelihood. In Q1, JWN stock badly missed consensus by 43%, despite a substantially reduced EPS target. It very well could be further disappointment for JWN stock.

As evidenced by its choppy trading, investors can’t get a confident read on Nordstrom.

For example, annual revenue has grown 19% over the past four years. But over the same timeframe, cost of goods sold has jumped more than 23%. From top to bottom, margins for JWN stock are stressed. The balance sheet is also wobbly, with massive cash outflows combined with a relatively slight decrease in long-term debt.

JWN stock is good for a speculative bet, but even within the troubled retail sector, there are more compelling opportunities.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.