With tens of thousands of different investment options available, it’s an ongoing battle to determine the winners from the losers. That being said, PayPal Holdings Inc (NASDAQ:PYPL) has always struck me as an opportunity belonging to the former category. Society can’t fully embrace the digital era until we apply our collective technologies to our monetary system. The popularity of payment services company Square Inc (NYSE:SQ) reflects the bullish argument towards PayPal stock.

{kind=link}

Unlike SQ, however, both end users and investors have reason to embrace PYPL. Folks who bought into Square’s initial public offering have been put through the ringer. As of now, SQ is in the red against its debut closing price.

In contrast, PayPal stock is up nearly 15% from its debut. Furthermore, the last time I wrote about PYPL stock — which was in late August of this year — shares have moved up more than 6%.

No, these aren’t what anybody would call stunning numbers. I also understand that there’s a heightened expectation towards technology-based IPOs. PayPal stock wouldn’t qualify as necessarily meeting those standards. Then again, there were a lot of questions in the immediate aftermath of the market debut of Facebook Inc (NASDAQ:FB).

Sometimes, it’s a lot better to start small and move higher, than it is the other way around ala Twitter Inc (NYSE:TWTR).

The Big Picture of PayPal stock

Nevertheless, there are nearer-term concerns.

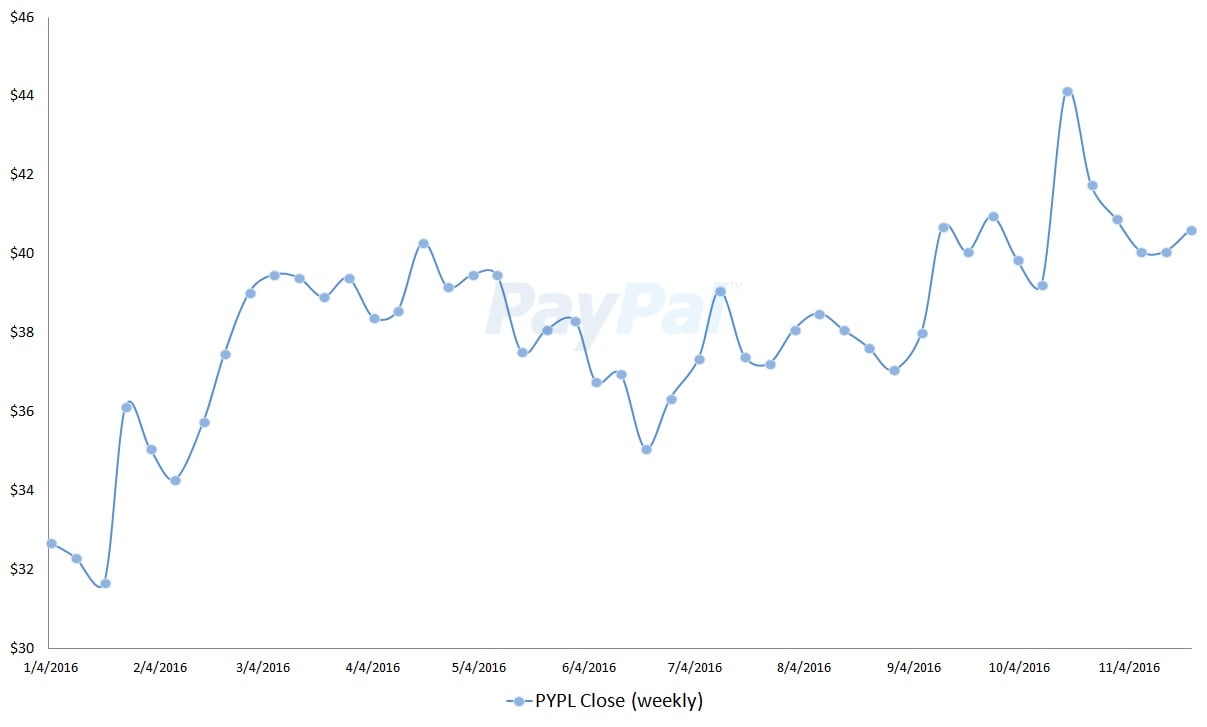

Click to Enlarge

Since peaking to an all-time closing high of $44.15 on Oct. 21, PayPal stock has dropped 8% in the markets. A 4% boost from mid-November helped mitigate the damage.

But optically, the problem remains — it was an ugly drop in capital value. It also raises questions about sustainability. After all, there’s a considerable number of analysts that have a “hold” rating on PYPL stock.

While the apprehension is understandable, I would first encourage potential buyers to look at PYPL from the widest scope possible. The digitalization of money is everywhere. Most importantly, the trend is not going anywhere. Not only are digital payment services and so-called “cryptocurrencies” much more convenient than their paper-backed brethren, they’re also infinitely more attractive to the rest of the world.

Consider the case of Mercado Bitcoin

, which according to Wired is “the first Brazilian bitcoin exchange and one of the largest digital currency operations in Latin America.” Before the rise of bitcoin, this company simply didn’t exist. Now, it is a major operation, swapping the Brazilian real for various digital currencies.

Essentially, the digital platform provides emerging markets an equitable channel to compete with developed nations. No longer is the focus on the national currency, but rather, the quality of the product or service. PayPal stock is popular with insiders because it blurs the distinction among world currencies. If people have a PYPL account, they can transact from anywhere in the world.

Bullish Fundamentals for PYPL Stock

On the home front, the populace trend is exceptionally favorable to PayPal stock. Two years ago, Bloomberg ran an article bluntly titled, “Young Americans Hate Cash.” Guess what? Young Americans absolutely hate cash, with a majority reverting to plastic for even nominally small purchases. In contrast, older people overwhelmingly prefer cash for such trivial expenditures. However, they’re the demographic on the way out, and the millennials are on the way in. Investing in PYPL stock is simply gambling that the sun will rise.

Of course, I’m using hyperbole — nothing is that automatic on Wall Street. However, there’s really nothing that would dissuade against the industry that PYPL stock is in, and that’s no exaggeration. For example, millennials don’t trust big institutions, so government agencies and major banks are out the door. It’s a challenge for which most companies like to think they have a handle. But really — how is that possible when formerly respected Wells Fargo & Co (NYSE:WFC) was caught faking customer accounts?

Fair or not, controversies like the WFC incident put a black eye on the traditional way of doing things — at least from the millennial perspective. And to be even more blunt, that’s the only perspective that matters. Early investors in PayPal stock understand that the company caters to the young and young-at-heart.

For them, seeing a PYPL merchant badge is more trust-inducing than a government certification. According to demographics, that mentality will be the prevailing one in years to come.

PYPL Is Ahead of the Curve

My ultimate assessment is that PayPal stock is ahead of the curve. I can expand upon the fundamentals to further bolster my thesis. I can even talk technical momentum. PYPL stock, despite its choppiness, has on average bent its trend channel upwards. That alone might convince some investors to take the plunge. But I think this is a company in which you can ignore several components of the financial and technical arguments, and just focus on the winds of change.

If society was largely hungering for a return to an earthy, rudimentary lifestyle, I would be concerned for PayPal stock. If more people reversed Robert Kiyosaki‘s advice and declared that cash is definitely not trash, PYPL wouldn’t even register as a faint trading idea. But the reality is that paper currencies are increasingly out of favor with the younger generation. That more than any other argument is what drives PYPL stock.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.