What a difference a year makes! That’s the central talking point among oil companies; in particular, the so-called “supermajors” like Exxon Mobil Corporation (NYSE:XOM) and Chevron Corporation (NYSE:CVX). As Europe’s biggest oil firm, Royal Dutch Shell Plc (ADR) (NYSE:RDS.A, NYSE:RDS.B) certainly belongs on that list. Investor enthusiasm is back with a vengeance as the crude oil markets have finally found solid footing.

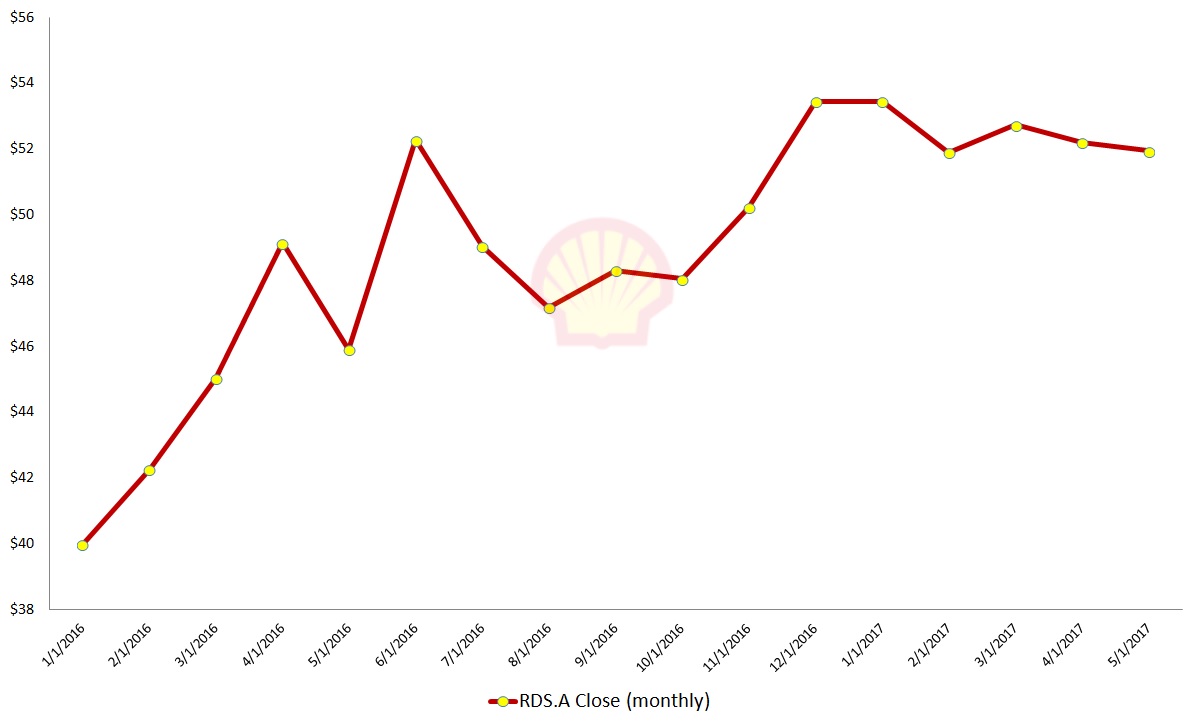

In May of last year, according to the International monetary Fund, the international benchmark Brent Crude Oil was priced around $47. Currently, a barrel of crude trades for over $51. However, the discrepancy was excessively severe in January of 2016, when Brent fell under $31. At that time, RDS stock and the rest of the industry was in full crisis mode. After all, the global oil index hadn’t been that weak since early 2004.

While the depressed energy markets devastated lesser-resourced competitors, the majors took it as a cue to solidify their financials. Royal Dutch Shell, along with its elite rivals, took a hard look at what was working, and what was not. Divesture was a common sight for RDS stock and the embattled oil industry.

But the sacrifices have paid off. Bloomberg reported that both Exxon Mobil and Chevron exceeded expectations for their first-quarter earnings results.

Better yet, Wall Street analysts are forecasting bigger and better results for the second quarter.

Inevitably, this means the pressure is on for Royal Dutch Shell. Both variants of RDS stock — RDS.A and RDS.B — were little moved by the news. Does the oil firm have what it takes to produce its own earnings surprise?

RDS Earnings Breakdown

For the first quarter of fiscal year 2017, RDS is forecasted to hit an earnings per share target of 74 cents. This is on the high end of the estimate range, which ranks from 36 cents at the bottom to 90 cents at the top. On the financials, this translates to a net income of $3.3 billion, a significant turnaround from the recent oil crisis.

In the year-ago level, Royal Dutch Shell was forecasted to hit a comparatively low 24 cents. The actual result came in substantially higher at 42 cents, for a positive surprise of 78%. Although enthusiasm is now surging for big oil stocks, RDS does have its work cut out for it.

In the past six quarters, Royal Dutch Shell recorded an evenly mixed performance — three beats, three misses. Ahead of Q1, RDS shareholders must feel like it’s a crapshoot. And optimism alone isn’t going to do much. Industry insiders were anticipating an earnings beat for ConocoPhillips (NYSE:COP), but it fell disappointingly short.

Nevertheless, RDS.A or RDS.B shareholders have reasons to be confident. First and most obviously, the threat of producing oil at uneconomical levels has subsided. Second, Royal Dutch Shell boosted its revenue picture, transitioning from paring losses to making solid gains. For example, the first half of 2016 featured quarter-over-quarter sales “growth” of -23%. In the second half, this figure improved to 1.2%.

The chances for RDS in Q1 are also buoyed by tighter financial controls. Out of necessity, Royal Dutch Shell execs slashed costs wherever they could. It will be tight for RDS.A and RDS.B, but they might have enough to get their earnings beat.

It’s All About the Price Tag

Click to Enlarge

On a year-to-date basis, Royal Dutch Shell is down 4.5%. That compares quite favorably to Exxon Mobil and Chevron, which are down 9% and 10.5%, respectively.

But in the end, it all comes down to the price of crude. We can talk ourselves silly about cost-cutting measures and other corporate initiatives. RDS and its big-oil buddies are integrated companies — they have an upstream business, as well as a downstream. If the underlying oil market doesn’t cooperate, no amount of internal engineering is going to do anything.

Fortunately, cooperation is exactly what Royal Dutch Shell is receiving. The lack of bearish momentum to push oil deeper into perdition suggests that much of the ugliness is baked in. The occasional choppy waves are to be expected, but the longer-term outlook is positive.

Overall, RDS.A and RDS.B should come out of earnings season better than when they entered. The oil markets are in the early stages of a long recovery. Royal Dutch Shell has also divested itself of underperforming projects, and is more financially robust. Finally, returning investor interest certainly doesn’t hurt.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.