Twilio Inc (NYSE:TWLO) has been rallying lately in expectation of a strong quarterly report. But this time around, the Street got things very wrong.

In after-hours trading, TWLO stock is off a grueling 30% to $23.93. That’s just above the 52-week low of $23.66 and well under the high of $70.96. Yes, playing the initial public offering game can be extremely volatile.

Now, the first quarter was not bad. The company posted earnings per share that beat the Street by 2 cents a share and revenues came to $87.4 million, compared to the consensus estimated of $83.60.

Instead, the reason for the plunge in TWLO stock is the guidance. For the current quarter, the company forecasts a loss of 10 cents to 11 cents and revenues ranging from $85.5 million to $87.5 million. The Street estimate, on the other hand, was for an 8 cent loss and revenues of $87.8 million.

The full-year outlook was also a bit light. TWLO is expecting a loss of 27 cents to 30 cents on revenues of $356 million to $362 million for the year. Yet the consensus was for a loss of 16 cents on revenues of $370 million.

Granted, such divergences may seem kind of minor. But then again, TWLO stock sported a frothy price-to-sale ratio of 11X ahead of the earnings. So even a slight change can make a big difference in the valuation for TWLO.

OK, so here are some of the other highlights of the quarter:

- The number of active customer accounts hit 40,696, up from 28,648 on a year-over-year basis.

- TWLO announced the extension of a strategic relationship with Amazon.com, Inc.’s (NASDAQ:AMZN) cloud services.

- The company released Programmable chat, which allows for real-time chat for the web, mobile and desktop.

- There was also the introduction of Programmable Fax.

- TWLO has launched the beta for Notify, which allows for managing notifications in apps like Facebook Inc’s (NASDAQ:FB) Messenger.

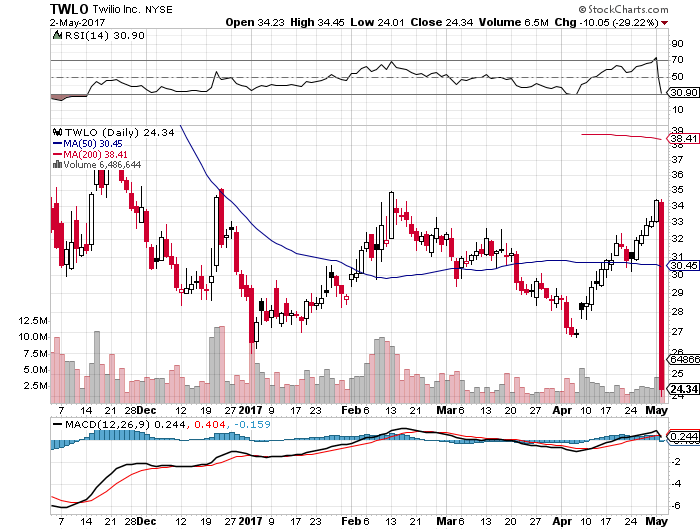

Click to Enlarge If Tuesday’s post-market losses stand, TWLO stock will be in deep technical danger.

The company should open around the $24 mark, smashing well below its 50-day moving average around $30.50, putting it near all-time lows at $23.66.

Now I’ve been bearish on TWLO stock for some time. One reason is the intense competitive environment. Some of the rivals include Cisco Systems, Inc. (NASDAQ:CSCO

), Vonage Holdings Corp. (NYSE:VG), CallFire, Nexmo and Bandwidth.com.Yet, Amazon may be the most lethal threat.

After all, the company has been building its own communications platform, with a focus on call center operations. While it was primarily for AMZN’s own ecommerce business, the company now thinks it could be leveraged into a separate offering, called Connect.

In light of this, Global Equities Research analyst Trip Chowdhry recently noted: “Pretty much TWLO is toast.”

But there is another nagging issue with TWLO stock — that is, the customer concentration. Note that last year about 30% of revenues came from 10 customers. Of these, FB’s WhatsAPP accounted for 9% and Uber represented over 10%.

Well, in the press release for Q1, Twilio CEO Jeff Lawson had this to say:

“While we are seeing some changes in the relationship with our largest customer, our momentum across the business continues to be strong, with a 42% year over year growth in Active Customer Accounts and a 62% year over year growth in Base Revenue during the quarter.”

Perhaps he is referring to Uber? If so, this should not be too much of a surprise. There’s no secret that Uber is an aggressive negotiator.

And, with the company trying to get to profitability as well as make itself a more attractive IPO candidate, there is probably more pressure to get better terms from vendors — especially when there are a myriad of alternatives on the market.

Tom Taulli runs the InvestorPlace blog IPO Playbook as well as OptionExercise.com, which provides interactive tools & services for employee stock options of pre/post IPO companies. Follow him on Twitter at @ttaulli. As of this writing, he did not hold a position in any of the aforementioned securities.