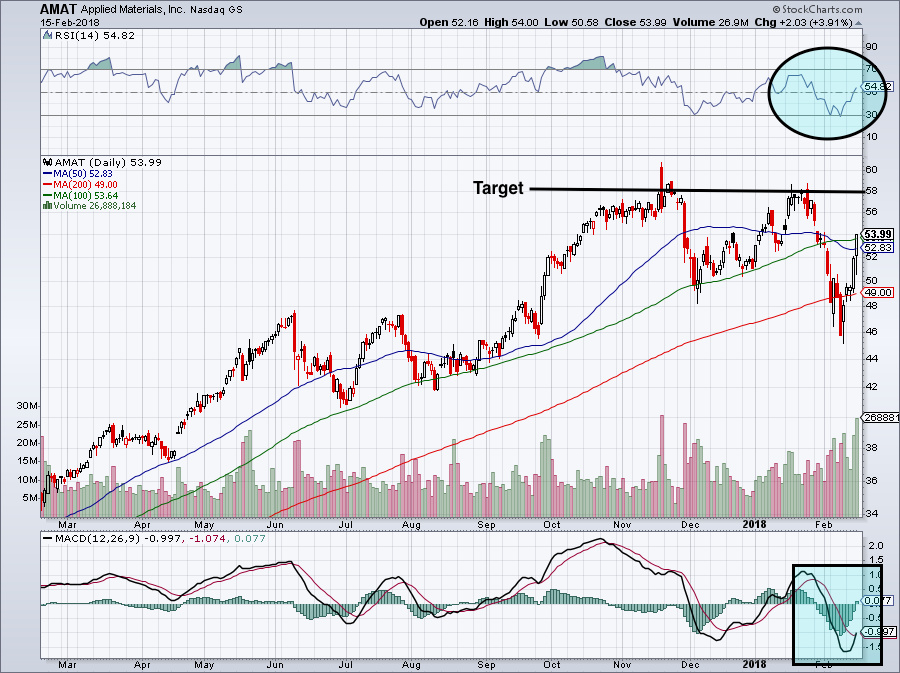

On Wednesday after the close, Applied Materials, Inc. (NASDAQ:AMAT) reported earnings. Despite a plethora of good news, AMAT stock actually sold off in early Thursday trading. That selloff also came despite the broader market powering higher. Ultimately though, investors saw the quarter for what it was — very good — and bought the stock. Shares ended higher by almost 4%, closing at $53.99.

So, where does that leave us now on Applied Materials stock?

It’s hard to see where there was disappointment. Fiscal first-quarter earnings per share of $1.06 came in 8 cents per share ahead of expectations. Revenue grew 28% year over year and operating cash flow surged 85% to $1.47 billion.

But guidance was the key.

Management expects second-quarter sales of $4.35 billion to $4.55 billion, easily ahead of estimates calling for $4.22 billion. Earnings guidance of $1.10 to $1.18 per share came in ahead analysts’ forecast of $1.01. Management’s midpoint guidance calls for 26% and 44% growth, respectively.

Seriously, these are great results! Oh, and did I mention the company doubled its dividend and raised its buyback plan, which had just $2.8 billion left, to $6 billion? Need I remind you, this is only a $55 billion company.

Valuing AMAT Stock

Management’s expectations for next quarter are obviously pretty good. But what about the rest of the year? Three months ago, analysts were looking for 2018 earnings per share of just $3.67. Now, though, they’re forecasting $4.40. Despite this 20% increase, AMAT stock is actually down over 5% from where it was trading 90 days ago.

As it stands, current estimates call for 35% earnings growth this year. This goes alongside forecasts for 20.4% revenue growth. Growth for 2019 now calls for mid-single-digit growth for both sales and earnings. But those estimates have increased as well. If analysts were significantly short for next quarter, it’s possible their estimates for 2019 aren’t accurate either.

When it comes to valuation, what are we paying for this 35% earnings and 20% sales grower? Just 12.2 times 2018 earnings.

The low valuation doesn’t make a lot of sense. Applied Materials supplies equipment for companies like Micron Technology, Inc. (NASDAQ:MU), which also trades at a ridiculously low valuation. In fact, I recently covered MU stock, concluding that it’s a buy. Shares trade at about 4 times earnings, while management provided much better-than-expected guidance last quarter and then revised it even higher earlier this month. MU stock is a no brainer.

Lam Research Corporation (NASDAQ:LRCX) is in a similar boat.

So why, then, do LRCX, MU, AMAT stock and others in the space trade with such low valuations despite their lofty cash flows and robust growth? Because investors are worried about the boom-bust possibility of the business. Right now it’s booming. But, at some point, it could bust and that will crush these stocks.

Trading Applied Materials Stock

The thing is, though, the management of these companies haven’t signaled an end to the current environment. NAND and DRAM may have lost some of their pricing power thanks to increases in supply, but demand remains incredibly strong, thanks to the proliferation of consumer technology products, the Internet of Things, servers and other memory-hungry applications.

Cisco Systems, Inc. (NASDAQ:CSCO) also reported earnings on Wednesday after the close. Here’s what management had to say: “We continue to be negatively impacted by the higher memory pricing we have discussed over the past several calls, which we expect to continue in the near term.”

Given these low valuations and positive outlook, it’s hard not to be a buyer of these stocks.

Click to Enlarge

In the case of AMAT stock, I see little reason why it can’t run to $58. That would represent a rally of roughly 7% from current levels. Truth be told, it’s hard to see why AMAT stock can’t retest its recent high just over $60, which would represent a return of more than 12%.

Further, I think MU and LRCX have a chance to do the same.

If the overall market continues to rebound and AMAT stock continues to churn out strong growth, it’s hard to imagine it not retesting these levels. And while 7% and 12% returns are respectful, they could be just the beginning. For instance, Stifel analysts upped their price target to $71 from $66 following AMAT’s earnings report, representing more than 30% upside.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a position in MU stock.