When Apple Inc. (NASDAQ:AAPL) posted its prior quarter’s results in early May, it was a mixed message. Though revenue of $61.1 billion was record-breaking, sales of the (relatively) new iPhone X were … shall we say less than thrilling? All told, 52.2 million units of the high-priced smartphone were snatched up, but that was only 3% better than year-ago levels. That’s hardly the screaming “upgrade cycle” many pros and owners of AAPL stock were chattering about headed into the report.

There was a proverbial silver lining surrounding the rain clouds, though. That is, Apple’s “service” revenue — an increasingly important effort to sell digital content — saw a 31% year-over-year improvement. All told, the company generated $9.2 billion worth of sales via its music, app and video ventures.

It’s a relationship that raises more questions than it answers. Chief among them is the question of whether or not the company’s Services arm will be able to offset the impending peak of smartphone-mania. A visualization might be able to help provide an answer to the question.

A Lot of Ground to Make Up

If we’re being honest, Apple had to, or has to, know there was an effective limit on how much one could charge for a mobile phone — regardless of its capabilities. And the company had to know there was a functional limit to how many high-end phones could be sold in any given quarter. Ditto for AAPL stock owners.

We may not be there yet, but if we’re not, we’re certainly closer to that point than not.

Translation: In that it’s safe to assume the iPad and Macintosh computers aren’t going to suddenly become bread-winners, if they haven’t done so yet, Apple’s next big growth engine has to be Services like music and video.

And the effort on that front has been solid, to be sure. It’s a business that didn’t meaningfully exist on its own just a few quarters ago. But when the company turned up the heat on the iTunes store a few quarters back to turn it into a profit center in and of itself, it was a clear — even if obscured — sign of what’s to come.

If that division is going to make a difference though, it’s going to have to move a lot faster than it’s moving now.

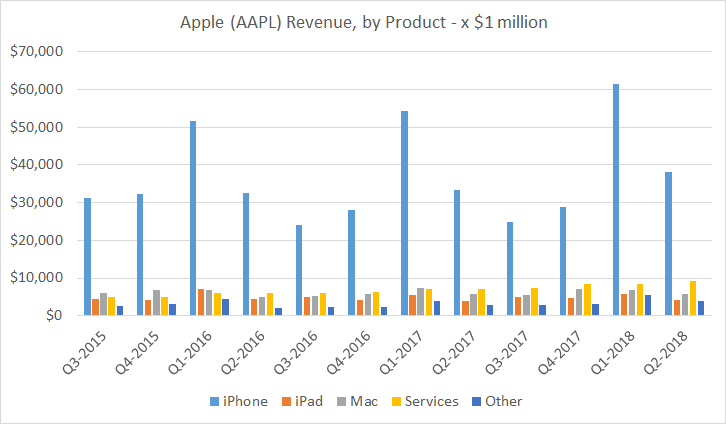

The graphic below tells the tale.

Click to Enlarge

From that perspective, the over-reliance on a product that may finally be losing its luster becomes clear: Even as good as its Services arm has become, it still only accounts for about 15% of the company’s top line. The iPhone, meanwhile, still accounts for more than 60% of Apple’s sales.

Competition for AAPL

Those who know the Apple Services story very, very well may recognize that its Services division is not only growing, but that its growth is accelerating. That’s good. That rise, however, may have more to do with a rising tide than Apple’s efforts in particular; consumers are increasingly accustomed to the subscription economy.

That’s the long way of saying you may not want to count on that growth pace lasting for much longer, as competition creeps in.

Don’t believe Apple can be toppled? Think again. Good competition is already gelling, even before Apple’s digital division has a chance to get going in earnest. YouTube Music is (finally) getting rave reviews after years of misfires from parent company Google, which is part of the ever-growing Alphabet Inc (NASDAQ:GOOGL

)(NASDAQ:GOOG). Meanwhile, in early April Amazon.com, Inc. (NASDAQ:AMZN) announced that the number of music subscribers it serviced had doubled in just six months.

Video? Netflix, Inc. (NASDAQ:NFLX) is still the king of the hill there, but YouTube Red is also (again, finally) starting to turn heads. Amazon still lags there, but there’s still enough interesting content between Amazon and Netflix to drive consumers to look past Apple’s video selection.

That leaves apps. On that front, Apple is still the king if only because the company sells so many iOS devices. It’s not clear, however, if apps alone will be enough to carry the weight of the pressure that’s about to be put on Apple’s services arm for the point in time when “peak iPhone” becomes a reality.

Bottom Line for AAPL Stock

Or, maybe Tim Cook has a trick up his sleeve, like the unveiling of a true “skinny” cable TV platform. It seems a bit late for that though. Indeed, it’s getting a bit late in the game for Apple to not be talking about, or doing, something besides more and more tweaks of existing products. Being first into a market may be more important than being the best.

None of this is to suggest Apple is doomed or that AAPL stock should be dumped at your earliest convenience. Apple on its worst day is still better than most other companies on their best days. It is to say, however, that the long dependence on the iPhone is quickly becoming a problem, and the company doesn’t have much in the lineup to use for an encore.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.