On Friday, General Electric Company (NYSE:GE) declared a 12 cent per share quarterly dividend. Some investors are torn on this payout though. Long-time holders likely think back to last year, when GE stock was paying out twice that amount. Some though are breathing a sigh of relief that it wasn’t cut again.

GE’s Dividend

In November, General Electric cut its annual dividend from 96 cents per share to just 48 cents per share. Amid balance sheet strains and crimping cash flows, management made some tough decisions. While the yield was over 4% at that point, GE stock has already fallen to the point where its yield now stands at 3.5%.

Now though, many are beginning to question whether GE’s first dividend cut was enough. CEO John Flannery didn’t help matters by not really saying if the dividend was safe for 2019. Flannery said the dividend is a function of cash flow which, although recovering, is still under pressure.

Furthermore, as the company sells assets to pay down debt, those cash flows disappear, making its dividend even harder to fund.

At least, that’s the takeaway from multiple analysts. Even the more optimistic analysts don’t inspire much confidence, though.

UBS analyst Steven Winoker has a neutral rating and $16 price target on the stock and says General Electric will cover its payout this year and next, albeit just barely.

Valuing General Electric

One of the most bearish analysts on GE has been Stephen Tusa of JPMorgan. Tusa has been spot on calling the decline in General Electric stock, so investors should listen to him. At the very least they would be wise to acknowledge what he has to say.

Just last week, Tusa raised a very important point on GE: its leverage. Tusa argues that General Electric needs to raise $30 billion in cash just to get to 2.5x times leverage. It would need to raise a whopping $40 billion just for GE’s leverage to be on par with its peers.

Remember that General Electric has a market cap of just $120 billion. Also worth noting is that Tusa has an $11 price target on the stock, implying about 20% downside from current levels and far below its current 52-week low of $12.73.

Analysts expect earnings to decline 10% this year to 94 cents per share. In 2019, current estimates call for GE to earn the same amount it did in 2017, a non-GAAP sum of $1.05 per share. Sales are forecast to decline slightly this year before climbing 1.3% in 2019.

So we have essentially no earning or revenue growth for two years, concerns on leverage and credit ratings, and worries over the dividend.

At almost 15 times this year’s earnings, why buy GE over the likes of Honeywell International Inc. (NYSE:HON), 3M Co (NYSE:MMM) or United Technologies Corporation (NYSE:UTX)?

These stocks yield 2%, 2.6% and 2.2% and trade at 19, 19.5 and 17.7 times this year’s earnings, respectively. Lower yields and higher valuations, yes, but much better growth and stronger balance sheets.

They deserved a look on their latest decline, all three of them.

Trading GE Stock

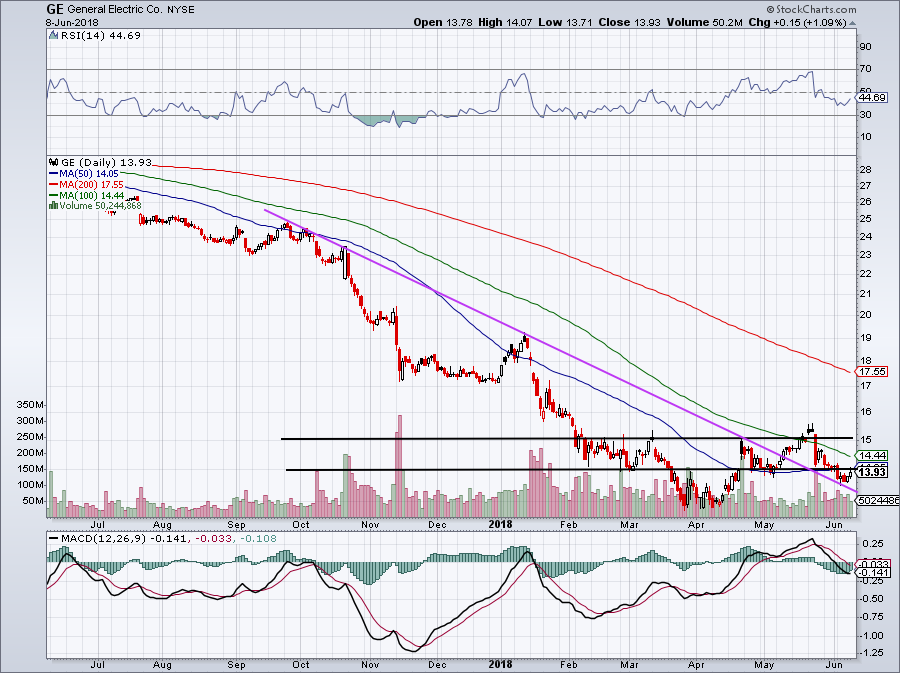

Click to Enlarge

Obviously GE’s fundamental story isn’t riveting, but we already knew that. Do the charts tell a different story though? Unlike Blue Apron Holdings Inc (NYSE:APRN), not really. GE’s balance sheet is under pressure.

In May, GE stock was looking incredibly constructive. It broke out over nasty downtrend resistance (in purple), saw $14 hold as support, broke above $15 and temporarily climbed over its 100-day moving average.

Just weeks later though and $15 has failed as support, as has $14, the 100-day moving average and the 50-day moving average. Can you see why bulls have been discouraged?

The only positive I’m seeing here is that GE stock is finding some support on the backside of its prior resistance trend-line (in purple). However, if it can’t get back above $14, more downside is likely on the table. Remember, like Tesla Inc (NASDAQ:TSLA), investors don’t have to be long or short. Sitting on your hands is an option too.

With GE, we don’t have to own it. And if other industrials like HON, MMM, and UTX don’t look attractive, we don’t have to own them, either.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.