The economy has been in slow-but-sure recovery over the past several years, but is finally starting to hit the gas. The U.S. is leading the way and now the economy is doing the best it has in years. You’d think that would mean good things for Wynn Resorts (NYSE:WYNN), Wynn stock and other casino names.

In fact, the strong economy is doing wonders for many businesses, particularly in the entertainment industry. Further, Vegas is doing well on the back of the U.S. economy while Macau is doing well on the back of an improving global economy and a seemingly always strong Chinese economy.

So why then are Wynn, Las Vegas Sands (NYSE:LVS), MGM Resorts (NYSE:MGM) and others similar stocks down?

The answer isn’t entirely clear.

At the start of the month, Macau gaming revenue growth came in at 17% year-over-year. While it saw a strong bump thanks the month lapping a big typhoon in August 2017, the results came in ahead of the +15% consensus expectations and bring the year-to-date tally to +17.5%.

Wynn Resorts specifically had some other issues at play, including Steve Wynn being removed as the CEO earlier this year. But by and large, the company continues to do well.

Valuing Wynn Stock

Last quarter didn’t go very smoothly for Wynn Resorts. Earnings of $1.53 per share came up way short of the $1.97 per share that analysts were looking for. While revenue grew almost 10% year-over-year, the $1.61 billion in sales came up $110 million short of consensus expectations.

That was a little more than a month ago and shares are still reeling. Wynn is off about 16% since then. After speaking with a few bulls, they are having trouble fathoming the latest beatdown. How could a stock with solid growth and a reasonable valuation be down so much?

Speaking of those metrics, consensus expectations call for 38% earnings growth this year and almost 20% next year. That goes alongside 7% and 12% sales growth in 2018 and 2019, respectively.

With the stock trading at 17.7 times this year’s earnings, Wynn stock isn’t the cheapest name in the world. But it’s a pretty reasonable valuation for a stock that had earnings of $5.46 a share in 2017 and is expected to generate $9 per share in earnings in 2019.

Adding to it, Wynn Resorts pays out an annual dividend of $3.00 per share

, good for a 2.35% yield.

Double-digit earnings growth? Check. High-single-digit to double-digit revenue growth? Check. Solid valuation and yield? Check. So why then is Wynn stock not a screaming buy? Because it’s akin to catching a falling knife.

Trading Wynn Stock

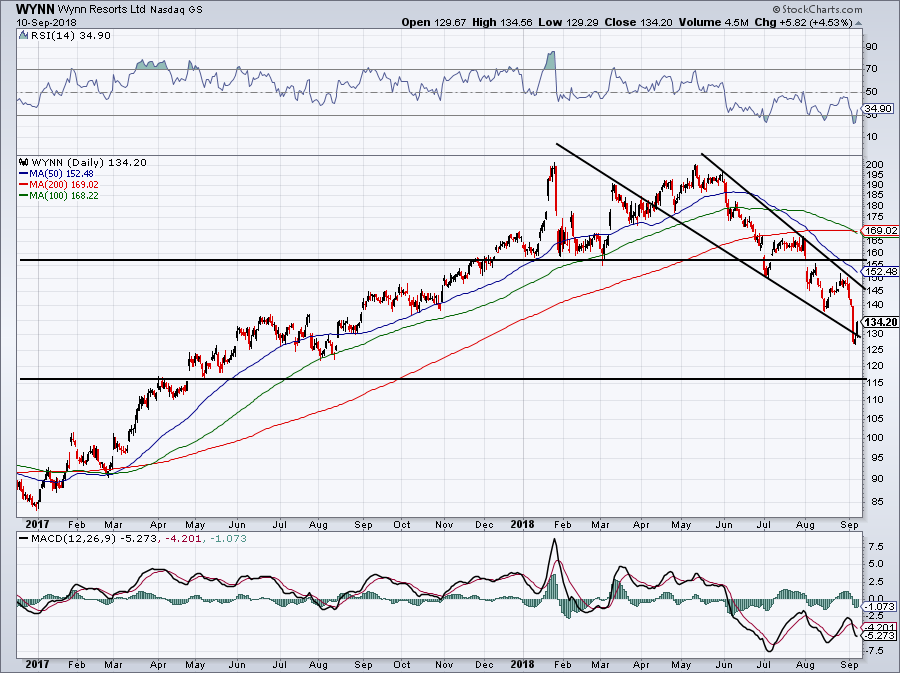

Click to Enlarge

Whether looking at the long-term or short-term charts, the story is the same: Wynn stock is trapped in a downward channel and investors should feel lucky that it is. I wouldn’t typically say that, except on Friday shares broke below the channel, dropping it into no man’s land.

No man’s land is never a good place to be when you’re looking to buy stocks. While the fundamentals check out and long-term investors will probably do fine nibbling a little Wynn right here, I prefer to marry fundamentals with technicals. Right now though, that technical picture isn’t too pretty.

This looks like a Picasso painting Steve Wynn accidentally ruined.

Now that the stock is back in the downward channel, Wynn has two tasks at hand. The first is to stay in that channel and not break below it. The second is to rally into resistance, currently near $145 and push through it. Once Wynn breaks out over the channel, then the bulls can start to plead their case.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.