The struggles continue for International Business Machines (NYSE:IBM). The tech dinosaur just keeps dogging its way along and its stock price has greatly lagged that of its peers. Down 10% since reporting earnings on Tuesday after the close, IBM stock is now down 15% on the year.

While shares are up 43% over the past ten years, consider that that includes a rally out of the depths of the Great Recession. The truth is, Big Blue continues to lag many of its large cap peers. The PowerShares QQQ ETF Trust (NASDAQ:QQQ) is up almost 450% over the past decade, highlighting the underperformance.

IBM has let Microsoft (NASDAQ:MSFT), Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG), Amazon (NASDAQ:AMZN), Salesforce (NASDAQ:CRM

) and others beat it to the punch when it comes to the cloud and cloud services. As a result, these companies (and many smaller ones) have enjoyed massive gains over the last few years while IBM stock has struggled mightily.

Granted IBM has made strides in artificial intelligence and commercial cloud applications. But had it made a series of strategic acquisitions rather than dump billions upon billions of dollars into its buyback plan, investors would be much more forgiving to the name now.

Valuing IBM Stock

In the company’s fiscal third quarter, IBM beat earnings estimates of $3.42 per share by two cents, but missed on revenue expectations. Sales of $18.76 billion came up $330 million short of expectations and declined 2% year-over-year (YoY).

IBM missing revenue estimates is nothing new, but it highlights that, despite how robust the technology industry remains, IBM simply refuses to take part. I have nothing against the current management team, but maybe it’s time for a C-suite shakeup.

Forecasts call for revenue growth of just 1% for fiscal 2018. Given that sales declined YoY for 22 straight quarters; yeah, 22 straight. That’s more than five years! An eventual rebound was bound to happen. The fact that expectations only call for a 1% bump is borderline pathetic, but the fact that estimates call for a 50 basis point decline in fiscal 2019 should induce even more nausea.

I hate to sound like such a jerk, but what exactly are investors supposed to get excited about at this point? It’s not sales growth and given that IBM is only expected to grow earnings 1% this year and 1.5% next year, the bottom line isn’t very enticing either. That’s good for about 9.5 times current earnings and honestly I can’t make the case for a higher valuation.

A frightening realization? IBM had revenue of $92.7 billion in 2014. In 2017, that shrank to just $79.1 billion, a decline of almost 15%. Operating income has been more than decimated, falling about 40% during the same period. There’s no growth, no strength, nothing. Comparatively, Alphabet had sales of $66 billion in 2014, two-thirds of IBM’s total. In 2017, that sum had nearly doubled to $110.9 billion.

Trading IBM Stock

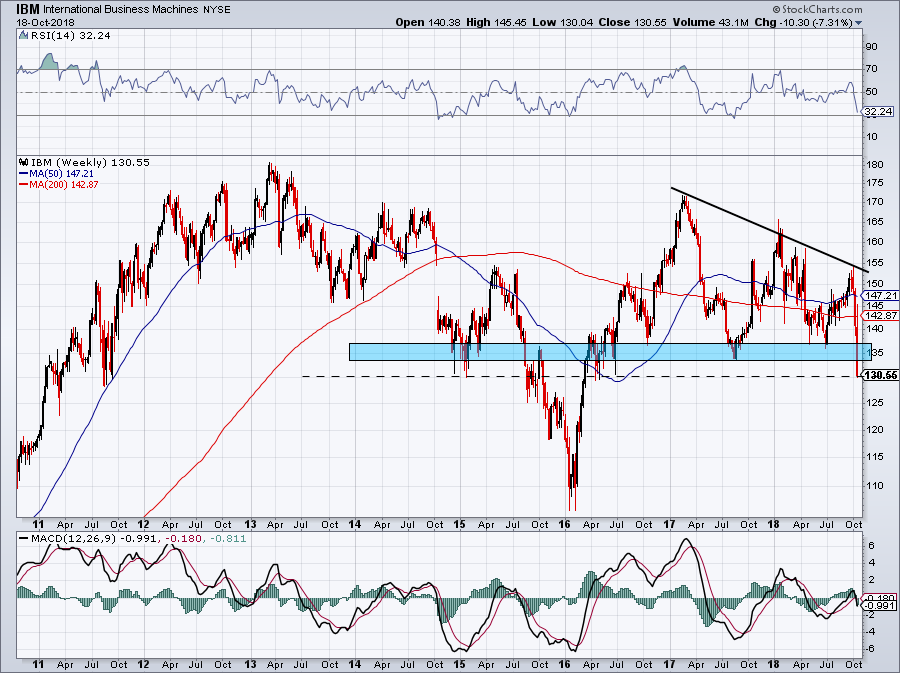

Click to Enlarge

The problem that IBM has? Even good growth in its smaller segments can’t move the needle much, as moving this legacy giant is like turning around an aircraft carrier. For all the flaws on its income statement, its balance sheet is actually pretty strong.

It’s my view that IBM would highly benefit from some M&A activity and new leadership. Think Microsoft when Satya Nadella took over for Steve Ballmer.

Anyway, how do we trade this dog?

Below this $135 support range and IBM stock is not looking good. I don’t have a problem with buying stock into support, but support needs to hold in order to make it a long candidate. That is not the case and now teetering on $130, I’m certainly not rushing in to buy the name. Below $130 and more downside becomes possible.

If IBM gets back over $135, maybe bottom-fishing it is worthwhile, perhaps on a rebound back to downtrend resistance. The issue is, if IBM is going to get there, it’s going to need a market-wide rebound to do it. The large cap names above will surely outperform IBM over that stretch.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell was long GOOGL and CRM.