Once it’s clear Amazon(NASDAQ:AMZN) is coming for a company’s business, what follows is rarely good… for the target. It’s usually great for Amazon stock holders. But now, AMZN has its sights set on a much larger business than usual, and Facebook’s (NASDAQ:FB) digital-ad dominance could be in danger.

Amazon is rapidly growing its advertising segment, which should become a major headwind for FB stock in the next few quarters. In the recent quarter, Amazon’s Other segment revenue — which mostly consists of advertising revenue — increased to $2.5 billion. Even after adjusting this for some accounting changes, the segment showed 56% growth on a year-over-year basis. This is on the back of a similar growth rate in the year-ago quarter.

At the same time, Facebook is facing a wide range of issues including concerns on data privacy and hiring a PR firm to defame critics. There is no quick solution for most of the challenges facing Facebook stock. So even if FB can recover its reputation, during this time it is likely that more ad dollars will shift toward Amazon’s “cleaner” platform — and profits will shift to Amazon stock

Amazon Stocks’s Next Profit Engine

In the past, Amazon has relied on the growth of AWS to deliver free cash flow, which it then invested in other segments. However, AMZN is now showing that the advertising segment can become an equally big driver for future profits. In a recent report, Piper Jaffray’s Michael Olson mentioned that by 2021 Amazon’s advertising segment can have an operating income of $16 billion compared to $15 billion for AWS. This shows the importance of advertising for Amazon.

According to eMarketer, Amazon’s market share in digital advertisement will rise from 4.1% in 2018 to 7.0% by 2020. The share of Facebook and Alphabet’s (NASDAQ:GOOGL) Google would fall from 57.7% to 55.9% in these two years. But I believe the growth numbers forecast for Amazon might be pessimistic. We’ve already seen that Amazon can leverage its platform and cash flow to massively grow a segment in a short time. Why would digital ads be an exception?

While looking at Amazon’s advertising potential, we should also look at Prime Video. Amazon is already bidding for all the 22 regional sports TV networks which would be sold by Disney (NYSE:DIS) as it acquires Twenty-First Century Fox

(NASDAQ:FOX,NASDAQ:FOXA). Amazon Prime has membership of over 100 million. The company is pouring huge sums into the growth of Prime Video. Although, Prime Video has not yet shown success similar to Netflix (NASDAQ:NFLX) or HBO, it is certainly possible that over the next few quarters we see more award-winning content from this segment.

Amazon provides advertisers with a clean platform which does not have any of the issues currently facing Facebook. Customers on Amazon are already visiting the platform with an intent to buy. Hence, the chances of converting a click into final sales is higher on Amazon compared to Facebook.

Challenges Facing Facebook

Amazon is not only looking to get a bigger share of the pie, it can change the entire dynamics of the digital-ad world. Facebook is the most at risk due to the data privacy issues built into the platform. Analysts who are bullish on FB stock point to the fact that few users are actually leaving the platform. This might be true because of the low number of social media options not owned by Facebook.

But, at the end of the day, the most important group is the advertisers not the users.

If advertisers start feeling that Facebook is not suitable to the identity of their brand, it could lead to the rapid flight of advertisers to other options. There are also efforts to regulate Facebook’s platform to prevent meddling in elections. Some groups are also calling for investigation of Facebook. This will only increase in the next few quarters as the next Presidential election cycle starts in U.S. Regulators in other countries like India are also planning regulate Facebook and Whatsapp.

These challenges might not decrease the user base, but it will certainly put pressure on major advertisers to seek other options. Amazon offers the best alternative to Facebook in terms of scale, buying intent and converting ad into final sales.

Amazon is also expanding into a number of new segments which will increase the interaction of customers with its platform. Earlier this year, Amazon purchased PillPack for $1 billion. It is now experimenting with delivering drugs to Amazon employees. We’ll see the full rollout of this service in 2019.

As you can see from the chart above, Facebook’s valuation is not very high. FB stock has recently moved below 20 times its trailing P/E ratio. But after a turbulent year, it is unlikely that the market will have an appetite for a higher valuation multiple for Facebook’s stock.

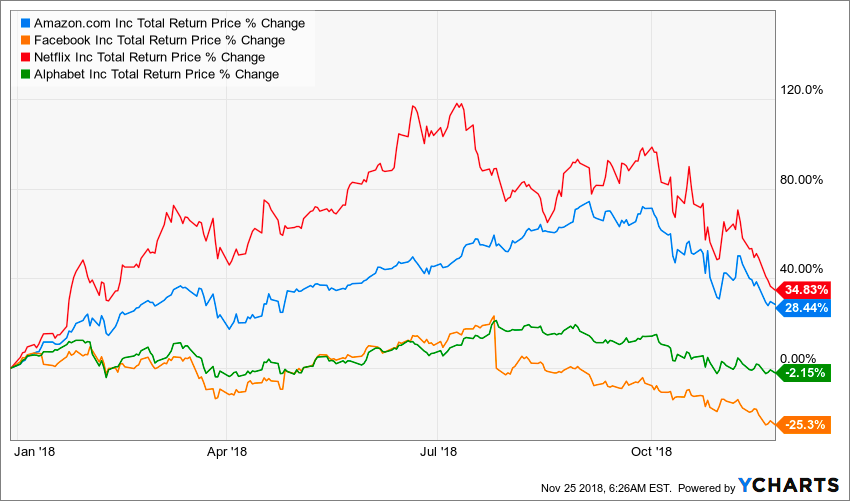

Facebook stock has also been the worst performing FANG stock in 2018. Things will get even worse in 2019 if advertisers make a big move toward Amazon. On the other hand, Amazon stock is still up by over 30% in 2018 despite suffering a correction post-earnings.

The Bottom Line for Amazon Stock

Amazon is making strong progress in building its ad platform. At the same time, Facebook is facing the threat of regulation and is suffering from massive negative PR in terms of how it has handled sensitive issues. This could lead to advertisers moving to Amazon’s platform, which offers a safer option for their brand and has better click to sales metric. This would be great for Amazon stock.

Facebook stock is cheap but its future trajectory depends a lot on how the current crisis is resolved. We could also see further headwinds for the stock in the next few quarters as further regulations are imposed on the company.

As of this writing, the author held no positions in the aforementioned securities.