On Tuesday, Boeing (NYSE:BA) released its fourth-quarter commercial planes delivery results, which showed a 14% increase year-over-year. Sparking a 3.8% gain as a result adds to the plane-maker’s bounce, with shares now up 17% from its Christmas Eve lows. Shares look set to rise further on an upgrade from Morgan Stanley to “overweight” today.

What do we make of the stock at this point?

From a fundamental perspective, BA stock remains a healthy pick. Sales and earnings continue to drift higher, as Boeing chews through a backlog that extends years into the future. Demand for airplanes and commercial jets remains robust, as demand for air travel continues its steady ascent. That creates strong free cash flow, allowing BA stock to return plenty of capital to investors.

All that said, the stock price has not been acting that healthy and after rallying around $50 per share over the last few weeks, it may be time for a breather.

Trading BA Stock

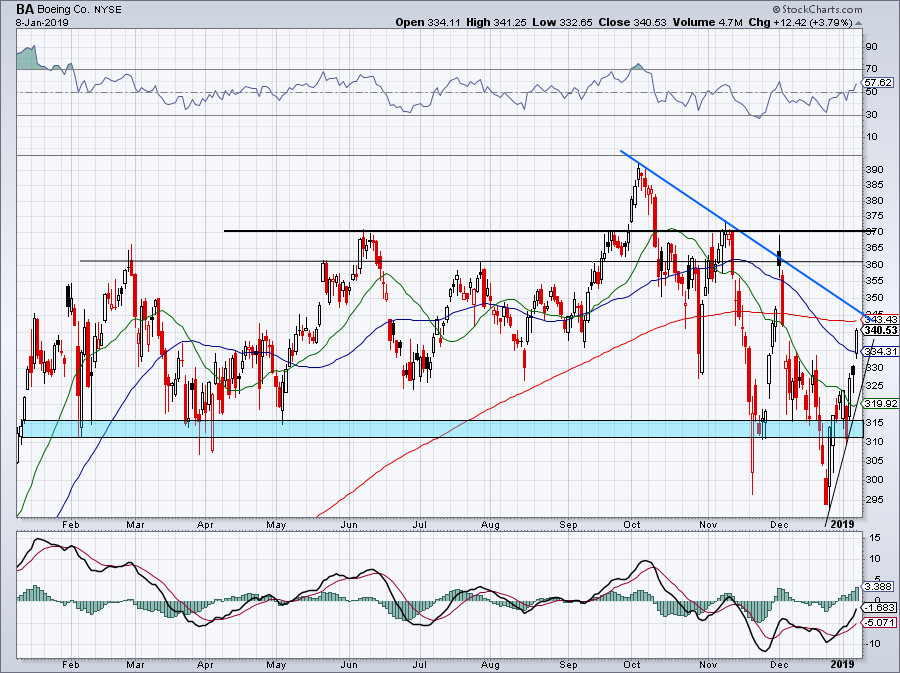

Click to Enlarge

The $310 to $315 level has been big-time support over the last 12 months. Even in November, BA shares gapped way below this area — opening near $300 and falling to $296 — before rallying back above it in a single session. However, even this level wasn’t enough to prop up BA stock when December came rolling around.

After bottoming in December, Boeing stock was quick to reclaim the $310 to $315 area before quickly leaping back above its 21-day and 50-day moving averages. Now what?

Shares are not yet overbought according to the RSI reading at the top of the chart. However, that doesn’t mean a pullback is off the table. The 200-day currently rests at $343, with downtrend resistance (blue line) just above it. At least on BA stock’s first attempt, I would expect this area to act as resistance.

If it doesn’t, BA stock could have room to rally up to $360 or $370 per share.

On a pullback, look to see where support materializes. When a stock goes basically straight up over a two-week stretch, finding levels of support becomes difficult. Will it retrace 50% of the move? Will the 50-day — just 1.7% away — hold up? How about the 21-day?

The simple fact is, we don’t know. But in an environment like this, it’s prudent to stay defensive when we’re trading because volatility still remains elevated. After a big run, it’s reasonable to look for resistance and be patient when it comes to finding support. Let price be the tell.

Valuing Boeing Stock

I love the consistency investors get with Boeing. The company is a cash-flow machine, and that is one of the most important metrics I look for when I’m searching for investments. Traders might see turbulence in Boeing’s chart, but investors see the cash flow. When the two groups can marry their theses together, that’s when we have the chance for outperformance.

Analysts expect a steady flight when it comes to sales, with revenue forecasts calling for 6.8% growth this year and 7% in 2019. Earnings growth is forecast to come in at 47% this year and 20% next year. The five-year forecast calls for about 22% annual growth.

Currently, BA stock price trades at about 20 times this year’s earnings. That’s really not a bad price given Boeing’s mid-to-high-single-digit sales growth and above-20% earnings growth.

Throw in its big buyback and 2.6% dividend yield, and BA stock looks even more attractive.

When BA stock hit $295 per share, its dividend yield was about 3%. For unflappable investors, that proved to be a timely buy. I have long liked BA down near $310, but now we wait to see what kind of price we can get.

While BA is impacted by China, the company doesn’t operate in a cyclical, consumer-based manner. However, improving trade talks can help Boeing going forward.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.