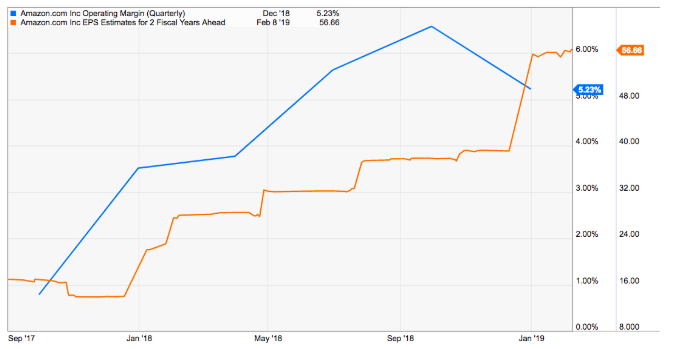

Amazon’s (NASDAQ: AMZN) margins have increased rapidly in the past few quarters, causing analysts’ earnings-per-share estimates for AMZN to rise. Over the last year, analysts following Amazon stock have increased their EPS estimates for two fiscal years into the future from less than $16 to $56. The company’s margins should rise further as the revenue share of its more profitable segments like its cloud business (AWS) and advertising increases.

Amazon (AMZN) stock Should Rebound as Analysts’ Estimates Rise

The percentage of revenue generated by the company’s businesses that it puts in its Other category has increased from 2.8% in the fourth quarter of 2017 to 4.7% last quarter. (Most Other revenue is derived from the company’s ad business.) In Q4, AWS accounted for 10.3% of the company’s revenue, up from 8.4% in Q4 of 2017. At the same time, concerns about the slowdown of AMZN’s revenue growth affecting sentiment towards Amazon stock are exaggerated, as the company can use several options to rapidly increase its top line.

Increases in Analysts’ EPS Estimates

Fig: Increases in the forward EPS estimates for AMZN

We can see in the above chart that analysts’ EPS estimates for AMZN have been increasing every quarter. The main reason for that is the growth of its margins throughout 2018.

Analysts’ consensus EPS estimates have risen a great deal, increasing from less than $16 to $56 in less than a year. This 250% jump has brought down the forward price-earnings multiple of Amazon stock, despite its rally in 2018. Amazon stock is currently trading at less than 30 times the consensus EPS estimate for two fiscal years from now.

That multiple is not pricey for a company which can use its growth levers to expand its top line as well as its bottom line. In 2019, analysts’ estimates can rise further as the company’s more profitable segments generate a higher percentage of its revenue.

Fig: The year-over-year growth of Amazon’s Other segment from Q3 of 2017 to Q4 of 2018

In Q4 of 2017, the revenue generated by the company’s Other segment, which is dominated by Amazon’s ad business, accounted for 2.8% of the company’s overall revenue. Last quarter, Other’s share of overall revenue jumped to 4.7%.

AMZN does not report the margins of this segment, but online advertising usually carries significant margins, as shown by the financial reports of Alphabet (NASDAQ: GOOG,NASDAQ:GOOGL) and Facebook (NASDAQ: FB). And as you can see from the chart above, the year-over-year growth rate of the Other segment has been close to 100% for the past four quarters.

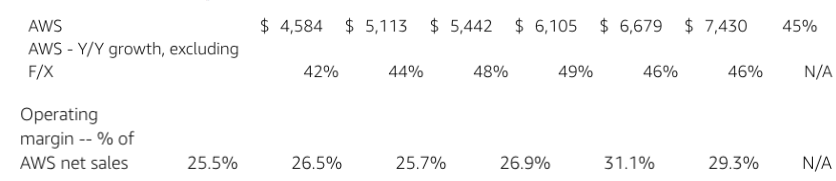

AWS Segment

Fg: The YoY growth of Amazon’s AWS segment

The growth of Amazon’s AWS unit has been quite strong for the past few quarters. This segment’s operating margin has also improved in recent quarters. In Q4 of 2017, the unit’s operating margin was 26.5% while last quarter it was 29.3%. AMZN has been able to defend its turf in the cloud segment despite the presence of goliath competitors like Microsoft (NASDAQ: MSFT), Google and IBM (NYSE: IBM).

It will be important to see if Alibaba (NYSE: BABA) is able to mount a strong challenge to Amazon’s cloud business. Last quarter, Alibaba ‘s cloud business grew 84%, and its margins improved. If Alibaba decides to ramp up its investments in this segment, Amazon’s pricing power could decrease, pulling down its margins and growth rate and hurting Amazon stock.

The Outlook of Amazon’s Margins

Together, the AWS and Other segments contribute 15% of Amazon’s total revenue. If these two segments grow at an annual rate of 60% for the next two years and its core retail segment grows 15%, the revenue share of these profitable businesses will exceed 24% in FY21. Moreover, the overall operating margins of AMZN will increase substantially due to the faster growth of these segments, providing Amazon stock with an important tailwind.

Fig: The slowdown of online store sales

The biggest contributor to Amazon’s top line is its e-commerce sales. However, in the past few quarters, the growth rate of this segment has slowed down. It is possible that management is intentionally trying to limit the growth of this segment due to its lower margins and its very high shipping costs. If the company is aiming to slow the growth of its online sales, then the unit’s pricing power and margins will probably increase because AMZN won’t feel as much urgency to stimulate its growth through aggressive discounts.

Revenue Growth

Slower revenue growth is the biggest problem facing AMZN stock. For the past two decades, the entire bullish case on Amazon stock was based on the company’s revenue growth. The company’s net-sales guidance for the current quarter is between $56 billion and $60 billion or growth of 10% -18%, compared to the first quarter of 2018.

At the low point of its guidance, Amazon’s revenue would rise 10%, which is quite low. But the company has a number of growth levers which can be used to fuel its growth in upcoming quarters. One of the best options for Amazon is to look to acquire another brick-and-mortar-retail company. By obtaining more physical stores, AMZN will improve its delivery services and build greater loyalty to its subscription services.

Amazon has a strong grip on the smart-speaker business, which it should be able to expand to other smart-home devices. The total addressable market of this segment is very high. Over the next few quarters, AMZN is likely to launch more smart-home devices to improve its foothold in that market.

Amazon has also entered the pharmacy-delivery market through the acquisition of Pill Pack in August 2018. The company is seeking licenses in different states. Amazon can leverage its extensive delivery platform to build a strong presence in that business.

Over the long term, AMZN has a number of options that it can use to increase its revenue growth and margins. Those improvements, in turn, should boost its EPS growth and Amazon stock in the next few quarters.

The Bottom Line on Amazon Stock

Although Amazon’s revenue growth may moderate, the long-term outlook of Amazon stock is still very strong. The company can make another big acquisition or expand its nascent businesses and services. I strongly recommend buying AMZN stock.

As of this writing, Rohit Chhatwal held no positions in the aforementioned securities.