The past three years have been tough for investors in Teva Pharmaceutical Industries (NYSE:TEVA). The share have gone from their 2015 peak near $72 to a current price below $16, slipping out of a rebound effort that took shape in 2018. TEVA stock has peeled back from last year’s high near $26, after bottoming near $11 in late-2017.

Nothing seems to excite investors for very long.

Nothing seems to excite investors for very long.

Analysts — some analysts anyway — are starting to take notice of subtle changes, putting several upgrades in place during the first quarter of this year.

Most of those calls are still cautious ones, with the most recent one from BMO Capital Markets being no exception to that norm. The analysts at Bank of Montreal (NYSE:BMO) see evidence of a turnaround taking shape, but remain concerned that Teva’s generics business and pipeline aren’t quite as robust as the firm would like.

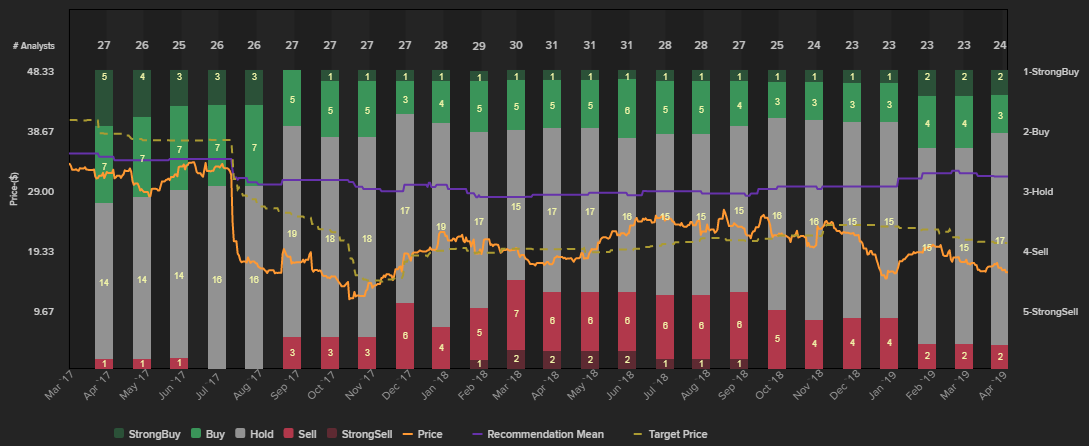

In taking a closer look at the analyst community’s changing consensus, though, it’s possible these professionals are quietly pointing toward more potential than most investors currently see in Teva stock.

Disguised Bullishness

BMO analyst Gary Nachman doesn’t believe recent launches of Huntington’s disease treatment Austedo and migraine treatment Ajovy will “be enough to put the overall company on a solid growth trajectory,” adding concern about the limited “visibility on the generic pipeline, where we believe TEVA is behind its peers.”

Still, there’s enough potential in Teva Pharmaceuticals stock for BMO to initiate coverage on it, rating it a Market Perform … a call that leaves the door wide open to updated ratings in either direction.

Nachman had a valid point, too, about the company’s generics pipeline. From what can be gleaned about it, it’s not necessarily scintillating.

That’s not exactly news though, to investors or to the company, or to other analysts for that matter. That’s been a lingering problem at Teva to most professional and amateur observers.

It may also be the groundwork for upgrades driven by the very pipeline BMO is concerned about.

Even if unintentionally, most other analysts are doing the same. As of the latest look, the pros collectively rate TEVA stock at only a little better than a “Hold” but simultaneously sport a consensus price target of $20.50. That’s 30% better than the stock’s current price.

Click to Enlarge

The superficial mismatch isn’t stunningly unusual; most stocks are priced below their consensus targets regardless of the collective buy/sell opinion on those names.

This particular disparity, however, is also mismatched with the “read between the lines” rhetoric. Teva stock has been upgraded three times so far this year, with two new-coverage initiations at Hold that may be precursors to expected upgrades.

If those upgrades are going to materialize, though, they’re going to do so thanks to only a handful of names in the company’s drug portfolio and pipeline.

Identifying Growth Drivers

While its bench of drugs is deep, Teva’s flagship product is multiple sclerosis drug Copaxone.

In its prime, Copaxone had no peers. It’s past its prime though, largely thanks to generic alternatives that have hit the market just in the past couple of years. Mylan (NASDAQ:MYL) got the nod from the FDA in late 2017; Novartis

(NYSE:NVS) is in the MS treatment race with its own version of Copaxone as well.

Those rival drugs have taken a measurable toll. In 2016, Teva sold $4.2 billion worth of Copaxone, but that volume was almost halved to a little less than $2.4 billion last year.

The bulk of the adverse impact of the generic multiple sclerosis treatment, however, is likely in the rearview mirror. Going forward, Teva shouldn’t be fighting as much of a headwind on at least that one front.

In the meantime, Ajovy and Austedo may be bigger growth drivers than BMO’s Nachman is currently be letting on.

Migraine drug Ajovy taps into a relatively underserved market. While Eli Lilly (NYSE:LLY) and Amgen (NASDAQ:AMGN)/Novartis are also in the same market with Emgality and Aimovig, respectively, analysts at Israel’s IBI anticipates peak sales of between $1.6 billion and $2.4 billion for Teva’s Ajovy. Meanwhile, RBC Capital Markets analyst Randall Stanicky forecasts peak sales of $1.3 billion for Austedo.

That level of success, along with the rest of the company’s portfolio and pipeline, should restore solid growth even as the benefit of Copaxone shrinks.

Also keep an eye on subsidiary Anda, which saw sales growth of 26% last quarter, reaching $363 million.

The upshot for owners of Teva stock is that it’s crystal clear where growth needs to come from. It won’t be difficult to see what’s working, and what’s not, given the relatively small portfolio and pipeline.

Bottom Line on Teva Stock

Again, without saying as much, most Teva stock analysts may be quietly expecting a respectable turnaround, but are thus far unwilling to say as much without more tangible proof it’s taking shape.

Analysts’ careers don’t just depend on quality analysis, but on being ‘right’ even if that standard is unspoken. These professionals may be cautiously leading investors to a marketwide conclusion that the forward-looking P/E of 6.0 for Teva stock is simply too cheap to pass up, given the potential — even if not the assured promise — of a turnaround.

Undoubtedly though, the rhetoric about slowing Copaxone’s deterioration and the growth of Austedo and Ajovy will help shape investors’ and analysts’ opinion. Investors would be wise to focus on those three drugs as a barometer of how the market feels about Teva stock.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.