In an effort to clear regulatory scrutiny, T-Mobile (NASDAQ:TMUS) and Sprint (NYSE:S) may offload Boost Mobile. Rumors began to circulate that Amazon (NASDAQ:AMZN) may be interested in the business, which sent shares of AT&T (NYSE:T) and Verizon (NYSE:VZ) tumbling. Is this an overreaction for AT&T stock and Verizon?

In my view, it’s an overreaction. First, we don’t even know that Amazon will step up and buy Boost Mobile. That’s why JPMorgan analysts said the dip in AT&T and Verizon were buying opportunities last week. Second, let’s say Amazon does enter the wireless race. There are plenty of reasons not to, but in theory, the ecommerce juggernaut could. In that event, while AT&T and Verizon will again suffer more temporary stock losses, consider that it would take a long time for them to start feeling the impact, assuming they do at all.

In short, these worries don’t make sense. Just like it doesn’t make sense to sell AT&T because

President Trump says to boycott the company as it is now the parent company of CNN.

With that in mind, let’s look at why AT&T stock is a solid holding for investors’ portfolios.

Valuing AT&T Stock

The key concern for AT&T is its debt load. Following the company’s acquisition of Time Warner, we saw long-term debt shoot from $127 billion (an already high figure) to $170 billion. I won’t defend the company’s acquisition of DirecTV, as investors continue to worry about cord-cutting trends leaving an exodus of subscribers.

However, the Time Warner deal is working, as it’s helped to boost free cash flow (FCF) significantly. While it upped the debt load in a big way, the added profitability, revenue growth and cash flow were worth it. As management pays down debt and sheds some non-core assets, it will hopefully prove to investors over time that AT&T is a dependable and stable addition to one’s portfolio.

At it stands, analysts expect 7.4% revenue growth this year and 0.4% growth in 2020. They also expect 1.7% earnings growth this year and next. Short of this year’s revenue estimates, that’s not very impressive, right? Right.

But at 8.7 times this year’s earnings, AT&T is not exactly expensive. Plus, it’s pretty clear this isn’t a revenue growth story. It’s an income play.

AT&T Dividend

Last quarter, AT&T missed revenue expectations and reported in-line earnings per share results. However, cash flow was the focus for me.

Operating cash flow jumped 24% to $11.1 billion. When accounting for CapEx, FCF came in at $5.9 billion, up 107% year-over-year (YoY) from $2.83 billion. More important, though, consider the implications of what that FCF means. First, the company paid $3.71 billion in dividends for the quarter. So FCF less the dividend leaves about $2.15 billion in cash flow. That amount can go directly to paying down debt should management choose to do so.

Further, the FCF dividend ratio (or the percentage of FCF that’s paid out in the form of a dividend) went from 108.5% in Q1 2018 to just 63.3% in Q1 2019. That’s a significant reduction and pads the safety in AT&T’s 6.6% dividend yield. Not that we needed any more confidence in this payout. AT&T has not only paid, but has raised its dividend for 35 straight years.

From the press release:

“Our first-quarter results show that we’re delivering on what we promised,” said Randall Stephenson, AT&T chairman and CEO. “We’re on plan to meet our de-leveraging goals with strong free cash flow and asset sales.”

Trading T Stock

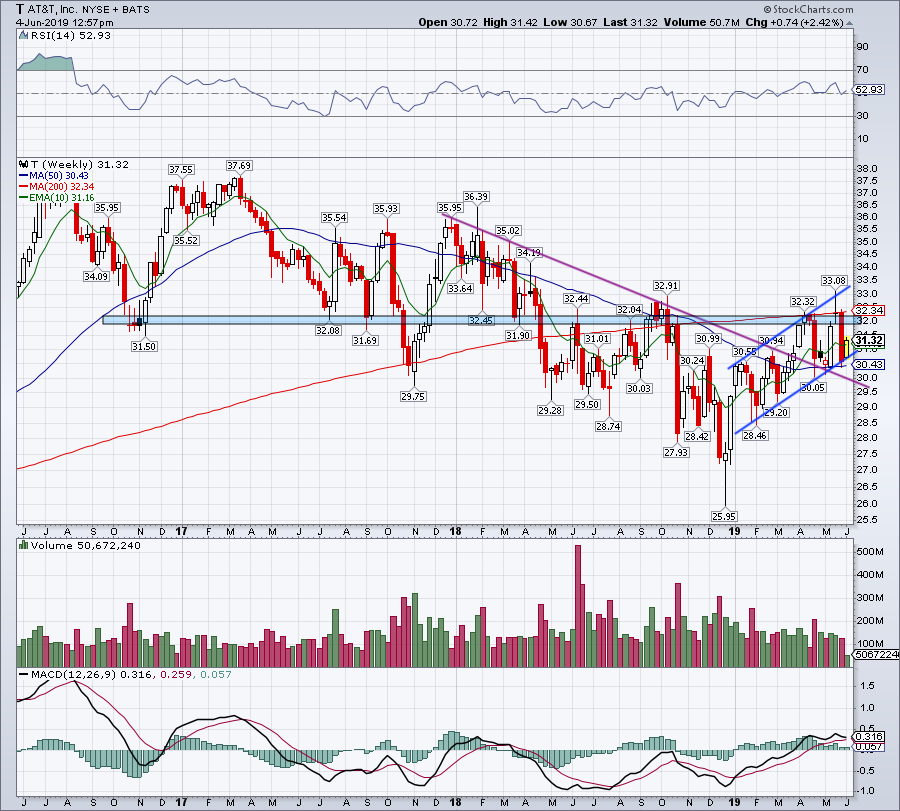

Click to Enlarge

AT&T stock is slowly but surely repairing the technical damage. The 200-week moving average has been working against the stock since April 2018. Twice in the last two months, this moving average has contained the rally in AT&T. If it eventually gives way, we can see a more dramatic change in the tide.

Until then, AT&T stock is going in the right direction. It broke over downtrend resistance (purple line) and is in the midst of a bullish channel (blue lines). The 50-week moving average has turned from resistance in Q1 to support in Q2.

The $32-ish level remains significant and so far, continues to act as resistance. If AT&T stock can keep its uptrend (channel support) in play, it increases the odds it will push through $32 and the 200-week moving average.

Remember, we’re mostly here for that 6.6% yield, but a decent return wouldn’t be frowned upon either. On the downside, look to see that the post-earnings lows near $30 hold. On a weekly basis, the $30.40 level needs to hold.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long T and AMZN.