Bank of America (NYSE:BAC), JPMorgan (NYSE:JPM) Goldman Sachs (NYSE:GS) and others are on the move Friday. The rally comes after many in the banking sector were given the green light to raise their dividend payouts and increase their buybacks. Among them was BAC stock.

On June 21st, all 18 banks passed the Fed’s stress test. On the 27th, the Fed approved numerous capital return increases from various banks.

For Bank of America stock specifically, the company can buyback up to $30.9 billion worth of stock. Management also plan to raise the quarterly dividend by 20% to 18 cents per share. At 72 cents per share annually, that will boost BAC stock’s dividend yield to roughly 2.5%. That’s up from the current 2.13% payout it sports now.

On the buyback front, $30.9 billion represents more than 11.5% of the bank’s current market cap. It’s also a huge increase from the $20.6 billion buyback that was approved last year. In fact, it’s 50% larger this year, showing just how strong of a balance sheet CEO Brian Moynihan & Co. have built since the financial crisis.

Who Else Is Boosting Returns?

JPMorgan was already attractive before it boosted its results. But after the Fed’s approval, it gets even better. JPM will raise its quarterly dividend 12.5% to 90 cents a share from 80 cents a share. Shares will yield 3.3% at current prices, while the bank can repurchase up to $29.4 billion worth of stock. That’s up big from last year’s $20.7 billion buyback approval. Although the dividend bump seems modest, keep in mind, JPM raised its dividend by 40% in 2018, while having the largest capital return plan in 2017 and 2018.

Citigroup (NYSE:

C) plans to bump its quarterly dividend to 51 cents per share from 45 cents per share, a 13% increase. The stock would yield about 3% based on Thursday’s closing price, although shares will rally in response. Citigroup can also repurchase up to $17.1 billion in stock. That’s a bit more than 10% of its $160 billion market cap.

Goldman Sachs can buy up to $7 billion worth of stock and plans a big increase in its dividend. The bank is raising its quarterly payout from 85 cents per share to $1.25 per share. The 47% bump to the dividend brings Goldman’s yield to a level that’s more in line with some of its banking peers. Shares will now yield about 2.5%, up big from its prior yield of 1.7%.

Most banks’ capital return plan — although not all, like Credit Suisse (NYSE:CS) — were approved by the Fed. That suggests healthy balance sheets and strong financials. While it’s not clear when a recession will hit, investors should feel more comfortable this time around than they did a decade ago. At least when it comes to the strength of the banking system.

Trading BAC Stock

Click to Enlarge

So where does all of this leave BAC stock?

Bank of America stock lags both Citigroup and JPMorgan in dividend yield and is now in-line with Goldman Sachs. However, while GS trades at just 8.5 times this year’s earnings, estimates call for a year-over-year decline in both revenue and earnings. BAC estimates call for growth in both categories and trades at roughly 10 times earnings.

So BAC trumps GS in some views, but what about JPM and C? Earnings and revenue estimates for BAC stock lag JPMorgan and Citigroup in 2019. Only in 2020 does BAC edge either of them in either category (with growth expectations of 10.2% earnings growth to JPMorgan’s 6.2% growth).

According to the data — growth, valuation and yield — Citigroup seems like the best all around pick. But that does not make BAC stock a bad bank to own.

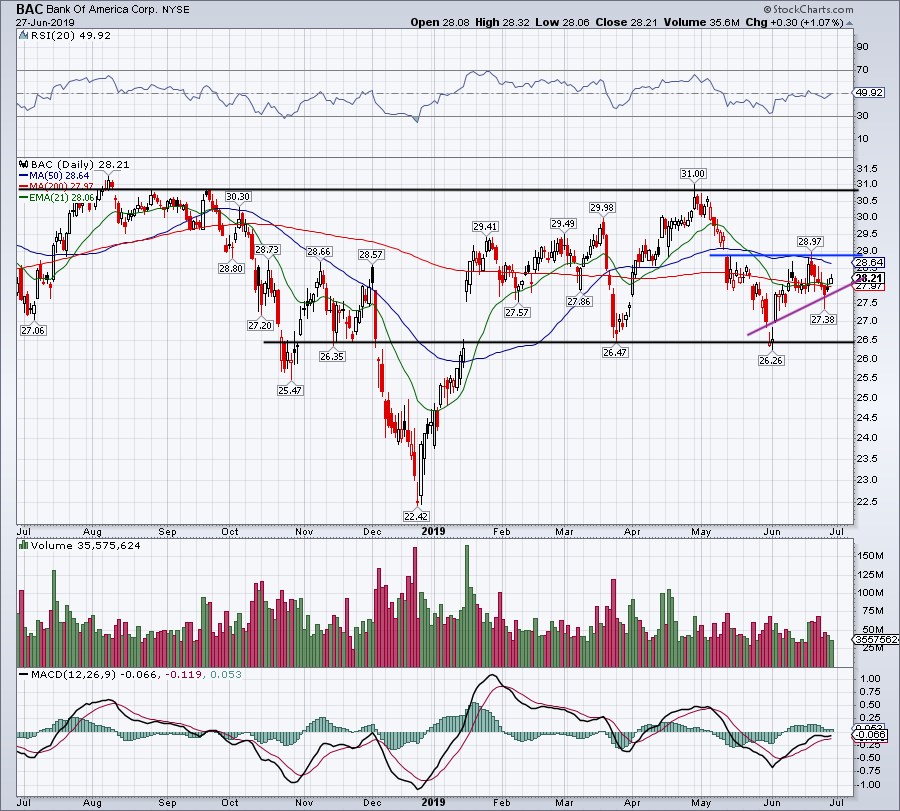

On the stock charts, BAC has been mostly range-bound between $26.50 support and $30.50 resistance. Over the 20-day and 200-day moving averages is good, as Bank of America stock trends higher (purple line). I want to see if this news can break BAC stock out over $29 and over the 50-day.

If it can, a run to range resistance is possible. Below $27.75 and a retest of range support could be in the cards.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.