The past three months haven’t been particularly easy ones for Hexo (NYSE:HEXO) newcomers. HEXO stock is down 40% from its late-April high, and knocking on the door of new six-month lows. Things could get worse before they get better.

Click to Enlarge

And yet, the great irony in the weakness (that’s not entirely unique to Hexo Corp stock) is, it’s one of the better-managed and better-priced marijuana plays. From a risk-vs-reward perspective, in fact, it may be one of the best. Namely, its price/sales ratio is one of the lowest in the industry, and the company’s on a trajectory towards actual profitability.

Too many investors still don’t see how its different sort of business model is a better, more palatable approach. There’s the crux of the opportunity.

Hexo Corp Stock Guilty by Association

Intellectually honest investors won’t even try to skirt the issue. When Constellation Brands (NYSE:STZ) first got the cannabis craze going in earnest back in October of 2017 with a relatively modest 10% stake in Canopy Growth (NYSE:CGC), traders were looking to plug into hype-induced strength.

A year later, recreational cannabis was to be legalized in Canada, which made for plenty of rally-driving noise. The United States’ legalization efforts only fanned the flames.

The milestone came and went largely as expected. Most of these companies have been able to report tens of millions of dollars’ worth of revenue with their first couple of quarterly filings; the lack of profits wasn’t an initial concern.

The euphoric hype came and went rather quickly though, once traders began to realize the heavy and somewhat indiscriminate spending in the name of growth and market share may never be fully justified by plausible results.

Along with the aforementioned Canopy Growth, shares of the legal marijuana’s most familiar names like Tilray (NASDAQ:TLRY), Aurora Cannabis (NYSE:ACB) and Cronos Group (NASDAQ:CRON) have all been fighting a seemingly losing battle since March.

Hexo stock has fared no better.

The market may have proverbially thrown the baby out with the bathwater, however, in treating Hexo like the rest of the names in the cannabis business. Though it’s not yet made a highly convincing case for true viability, it’s closer than most.

The key has been its more reserved, methodical approach to its expansion.

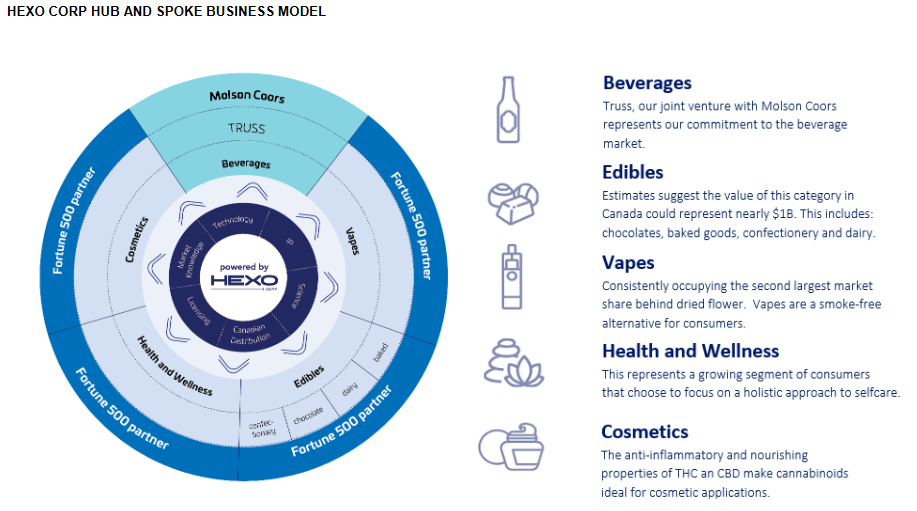

Hexo’s Hub and Spoke

It’s been mentioned often, but here’s a detailed look at Hexo’s so-called “hub and spoke

.”

In short, Hexo is a hub, or center of the wheel, and its different product categories likes beverages, edibles and vapes are spokes.

It’s what’s found at the end of those spokes, on the outer edge of the wheel, that differentiates Hexo stock from investments in other marijuana stocks. Though other cannabis names are willing to work with higher-profile names to develop a branded product, Hexo is being built from the ground up with the specific aim of partnering with a bigger brand on all of its product fronts. Bigger brands with deeper pockets can market these joint ventures more effectively.

Click to Enlarge

The first of those partners is Molson Coors Brewing (NYSE:TAP). The beer giant confirmed in August of last year it would develop a cannabis beverage line with Hexo, fortune 500-level partners are slow to move, though. The spots at the end of Hexo’s other spokes have yet to fully fill up with other partners, and the Molson Coors/Hexo partnership ( called Truss) has only indicated it will launch a beverage later this year.

That’s longer than most hype-chasing cannabis investors might like to wait.

Additional delays are serving as roadblocks on other fronts, underscoring investor frustration. Canada’s regulatory body announced last month that cannabis edibles wouldn’t be allowed to be sold in Canada until December, and even then on an initially-limited basis, pushing back a previous target launch date of October.

Looking Ahead for HEXO Stock

The regulatory headwind, however, may ultimately work in favor of Hexo rather than against it, buying it time to continue finding the right partners while its cannabis rivals continue to spend their way deeper into debt.

That’s certainly the way the analyst community has handicapped Hexo stock. These professionals specifically don’t expect the company to drive massive, high-margin growth until fiscal Q3 of 2020. That’s three quarters away, and well into 2020, after Health Canada should at least permits most of the would-be cannabis products on store shelves.

The timing matters. Expectations of most other marijuana stocks are uncomfortably high for this year, in terms of investors’ sentiment, as well as for analysts’ numerical outlooks.

The bar isn’t set quite as high for Hexo though. Indeed, the bar appears to be set at strangely low levels. With the current HEXO stock price at $4.70, Hexo shares are trading at a respectable (for the cannabis business anyway) forward-looking P/E of just above 50.

The unique hub and spoke business model, though arguably limits upside, also limits the potential downside, even if it takes longer to develop fruit-bearing products. Most important though, the partnering approach is an inexpensive way to carve out a piece of the cannabis market other names in the business are spending a fortune on just a chance to win. The projected swing to a profit isn’t merely wishful thinking.

Bottom Line on Hexo Stock

It’s admittedly difficult to ferret out the cannabis industry’s winners and losers. Though each outfit is starting to take different paths as they choose their areas of expertise, they largely remain more alike than different. Investors, in the meantime, continue to treat them all the same. They’re still rising and falling as a herd.

For investors that can look more than just a few days down the road though, Hexo stock is an option that’s deliberately, and wisely, taking a slower but safer road to profitability. That decision, ironically enough, means it may reach that destination sooner than most of its peers and rivals do.

Investors just have to be willing to hang on for the next three quarters and digest whatever volatility the stock is going to dish out. Waiting on the sidelines wouldn’t be a bad strategy either.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.