The most recent quarterly report from Amazon (NASDAQ:AMZN) came and went with relatively modest fanfare. Although Amazon stock fell on the earnings shortfall, net income was still up year-over-year, and revenue topped expectations.

It was likely, given the market’s condition at the time, AMZN shares were destined to fall following earnings no matter what the ecommerce giant dished out.

It’s entirely possible though that a handful of important nuances of Amazon’s quarterly filing were missed thanks to the marketwide meltdown that materialized right around the same time. Since July 25, when Amazon delivered its second-quarter numbers, the S&P 500 is down more than 5%, and teasing investors with even more downside.

Three details that matter stand out among the other matters that may have been obscured by the noise.

Cash Flow

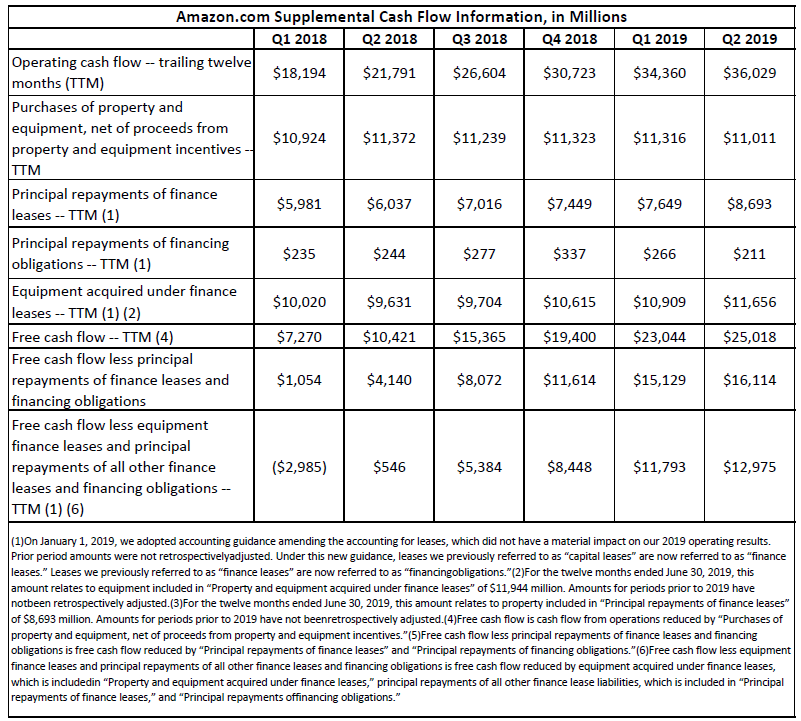

It’s been a contentious point for some time now. That is, Amazon categorizes the costs associated with the equipment that powers Amazon Web Services and at least some of its real estate as equipment finance leases. Normally, such spending would be booked as a capital expense.

It’s neither illegal nor immoral. GAAP standards were constructed that didn’t have rented access to a third party’s cloud in mind. It’s also arguable that the servers, storage and computing hardware needed to make AWS work are more meaningfully booked as lease obligations since they have a relatively short shelf life.

It was a problem nonetheless though, as accounting for these costs allowed the touted cash flow statements to suggest the company was actually paying all of its bills, which it wasn’t until the second quarter of 2018. That’s when cash flow, even after making payments on purchases added to the balance sheet as lease and financing liabilities. That free cash flow on a trailing-twelve-month basis reached a new record of nearly $13 billion last quarter.

Click to Enlarge

Amazon, in short, really is turning a profit.

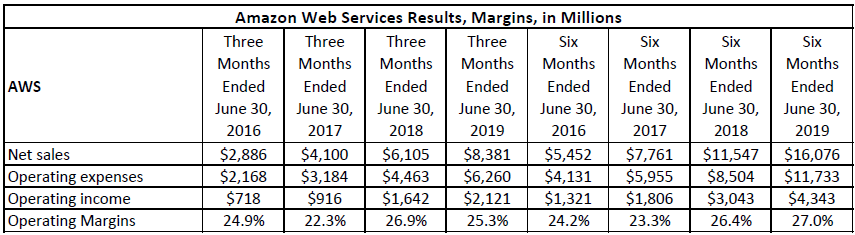

AWS Margins

Although Amazon Web Services, or AWS, has turned an operating profit for years. But, in that the competition between it, Microsoft (NASDAQ:MSFT) and Alphabet

(NASDAQ:GOOG,NASDAQ:GOOGL) mainstay Google have been part of an ever-growing competition. One would expect the race to eventually turn into a margin-gouging price war.

It hasn’t. In fact, margins are slightly improving. Over the past two quarters, Amazon Web Services’ operating margins have rolled in at 27.0%, and last quarter’s margin rate of 25.3% is still above the comparable figures from 2016 and 2017.

Click to Enlarge

There may still come a time when AWS profitability is challenged, but that time’s not here yet.

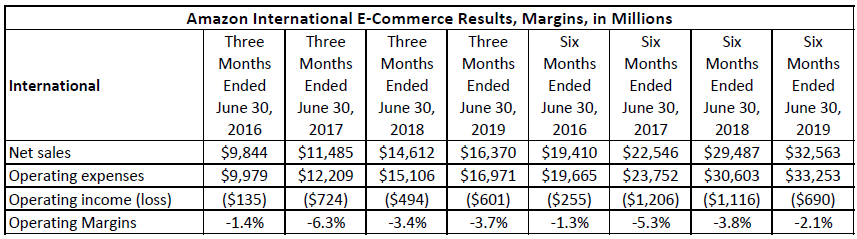

International Growth May Be in Trouble

Earlier this week, RBC Capital analyst Mark Mahaney commented that Turkey, Australia, Mexico, Brazil, and India “offer Amazon a very large, underpenetrated market opportunity,” adding that “We believe that investors may underappreciate the potential of these markets.”

His point was well taken by fans and followers of Amazon stock too. Though its North American business still has room to grow, it’s closer to a peak than not. The rest of the world, meanwhile, has not been fully exposed to the Amazon machine.

There’s something of a price to be paid for growing overseas though. That is, although its ecommerce business in North America is profitable and growing the bottom line as it expands, the company’s international arm remains in the red.

Click to Enlarge

Amazon stock owners have seen the occasional step towards viability, via a smaller year-over-year loss for its international division. The first quarter of this year was one such quarter. It didn’t persist though. The second quarter’s international operation saw its loss expand again despite revenue growth.

Growth of India’s ecommerce site Flipkart, owned by Walmart (NYSE:WMT), may have something to do with that … at least for India’s piece of that opportunity.

Looking Ahead for Amazon Stock

Of course, none of these nuances matters right now, here in the midst of what’s been a fairly indiscriminate selloff. AMZN stock is down 12% from its early July high, and sheer fear is threatening to drive it lower.

With the exception of its international business though, Amazon is doing well. Most importantly, it’s legitimately cash-flow-positive.

If and when any concerns about a global economic slowdown abate (though there’s no guarantee that will happen anytime soon), Amazon will emerge as the winner it’s for the most part been treated like. In the meantime though, AMZN stock isn’t for the faint of heart.

As of this writing, James Brumley held a long position in Alphabet. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.