I have to give credit where credit is due. Early in April, our own Will Ashworth made the case for why shares of Comcast (NASDAQ:CMCSA) were worth $45 a piece, just as the share price cleared $40. Immediately, Comcast stock took off, almost as if Ashworth was directly pushing sentiment higher.

More impressively, the CMCSA stock price closed slightly above the specified target a few weeks back. At the time when my InvestorPlace colleague made his call, the media giant just weeks away from the release its first quarter 2019 earnings results.

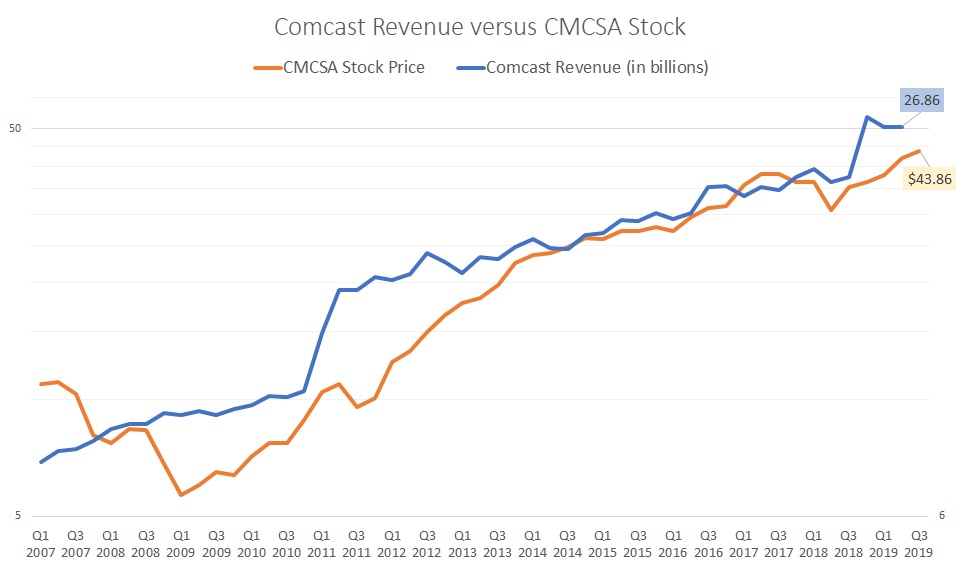

And Q1 was a pretty solid report for the company. Against an earnings-per-share target of 68 cents, Comcast delivered 76 cents. In terms of high-speed internet customers, it brought in 375,000 net additions. That was up significantly from the 353,000 expected net adds. Despite a revenue miss — $26.86 billion versus a consensus target of $27.2 billion — Comcast stock responded positively following the report.

It was more of the same in Q2. Consensus for per-share profitability was 75 cents. Actuals came in three pennies higher. Furthermore, Comcast beat again on internet-customer expectations, bringing in 209,000 net adds compared to an expected 208,000. But just like in Q1, revenue of $26.86 billion missed the consensus target of $27.06 billion.

That said, the key difference was the magnitude. On EPS and internet-subscription targets, the Q2 beats were notably smaller in scale than in Q1. I don’t think investors should take this necessarily as a negative on Comcast stock. However, it could suggest that much of the bullishness is now factored in.

But is there still room for the CMCSA stock price to move higher? Here are my thoughts:

Low-Hanging Fruit in Comcast Stock is Gone

Thanks to hindsight, we can see that the best time to have jumped aboard Comcast was at the beginning of this year. And when Ashworth presciently forecast the future CMCSA stock price, that was probably the last stop to profitability.

With Comcast stock now close to $45, I have mixed feelings on the matter. If you have a long-term outlook, this might not be a bad play. Currently, shares have a dividend yield of 1.9%. Moreover, management is making aggressive moves toward the streaming space.

And like rival Disney (NYSE:DIS), Comcast offers diverse revenue channels. Along with its cable networks and broadcast television, CMCSA stock provides exposure to filmed entertainment and theme parks. For the latter, consumers have demonstrated a willingness to open their wallets despite rising ticket prices.

But my biggest concern now is that these are known factors. For Comcast stock to move substantially higher, we need to have some fresh catalysts.

However, I just didn’t get a boost of confidence from the Q2 results. Here, Comcast did what they usually do: produce solid results. Over the last several years, the company has steadily grown their revenue channels.

Click to Enlarge

But CMCSA stock has also moved higher along with those rising sales. In other words, there’s no mismatch between the fundamentals and the technicals. If you’re buying shares now, you’re doing so based on the same information everyone else has.

Personally, I’m not particularly interested in Comcast stock. For one, its theme park and resort business pales in comparison

to Disney’s offerings. As well, I believe that Disney has the more lucrative film franchises. Not only do they have Star Wars, but they also own much of the ultra-popular Marvel Comics universe.

That’s a tough hurdle for any organization to overcome.

Streaming Saturation Detracts from CMCSA Stock

Of course, another obstacle for Comcast stock has been the cord-cutting phenomenon. With names like Netflix (NASDAQ:NFLX) and Roku (NASDAQ:ROKU) providing alternatives to traditional media, cable providers risk irrelevancy.

Comcast has responded in perhaps the only way possible: create a streaming platform of its own. That’s wonderful but we now have a saturation of options. Amazon (NASDAQ:AMZN) has Prime Video. Apple (NASDAQ:AAPL) and AT&T (NYSE:T) will dive into the arena soon.

At that point, only the best content will provide distinction among the mass of streaming options. And again, I’m not convinced that Comcast has the best entertainment brands. Therefore, I’m going to sit this one out.

As of this writing, Josh Enomoto is long T stock.